Jonathan B. Baker, Nancy L. Rose, Steven C. Salop, and Fiona Scott Morton don’t like vertical mergers:

Vertical mergers can harm competition, for example, through input foreclosure or customer foreclosure, or by the creation of two-level entry barriers. … Competitive harms from foreclosure can occur from the merged firm exercising its increased bargaining leverage to raise rivals’ costs or reduce rivals’ access to the market. Vertical mergers also can facilitate coordination by eliminating a disruptive or “maverick” competitor at one vertical level, or through information exchange. Vertical mergers also can eliminate potential competition between the merging parties. Regulated firms can use vertical integration to evade rate regulation. These competitive harms normally occur when at least one of the markets has an oligopoly structure. They can lead to higher prices, lower output, quality reductions, and reduced investment and innovation.

Baker et al. go so far as to argue that any vertical merger in which the downstream firm is subject to price regulation should face a presumption that the merger is anticompetitive.

George Stigler’s well-known article on vertical integration identifies several ways in which vertical integration increases welfare by subverting price controls:

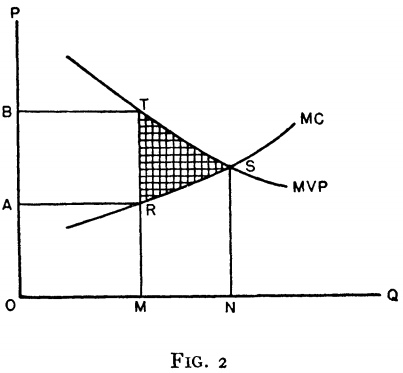

The most important of these other forces, I believe, is the failure of the price system (because of monopoly or public regulation) to clear markets at prices within the limits of the marginal cost of the product (to the buyer if he makes it) and its marginal-value product (to the seller if he further fabricates it). This phenomenon was strikingly illustrated by the spate of vertical mergers in the United States during and immediately after World War II, to circumvent public and private price control and allocations. A regulated price of OA was set (Fig. 2), at which an output of OM was produced. This quantity had a marginal value of OB to buyers, who were rationed on a nonprice basis. The gain to buyers and sellers combined from a free price of NS was the shaded area, RST, and vertical integration was the simple way of obtaining this gain. This was the rationale of the integration of radio manufacturers into cabinet manufacture, of steel firms into fabricated products, etc.

Stigler was on to something:

- In 1947, Emerson Radio acquired Plastimold, a maker of plastic radio cabinets. The president of Emerson at the time, Benjamin Abrams, stated “Plastimold is an outstanding producer of molded radio cabinets and gives Emerson an assured source of supply of one of the principal components in the production of radio sets.” [emphasis added]

- In the same year, the Congressional Record reported, “Admiral Corp. like other large radio manufacturers has reached out to take over a manufacturer of radio cabinets, the Chicago Cabinet Corp.”

- In 1948, the Federal Trade Commission ascribed wartime price controls and shortages as reasons for vertical mergers in the textiles industry as well as distillers’ acquisitions of wineries.

While there may have been some public policy rationale for price controls, it’s clear the controls resulted in shortages and a deadweight loss in many markets. As such, it’s likely that vertical integration to avoid the price controls improved consumer welfare (if only slightly, as in the figure above) and reduced the deadweight loss.

Rather than leading to monopolization, Stigler provides examples in which vertical integration was employed to circumvent monopolization by cartel quotas and/or price-fixing: “Almost every raw-material cartel has had trouble with customers who wish to integrate backward, in order to negate the cartel prices.”

In contrast to Stigler’s analysis, Salop and Daniel P. Culley begin from an implied assumption that where price regulation occurs, the controls are good for society. Thus, they argue avoidance of the price controls are harmful or against the public interest:

Example: The classic example is the pre-divestiture behavior of AT&T, which allegedly used its purchases of equipment at inflated prices from its wholly-owned subsidiary, Western Electric, to artificially increase its costs and so justify higher regulated prices.

This claim is supported by the court in U.S. v. AT&T [emphasis added]:

The Operating Companies have taken these actions, it is said, because the existence of rate of return regulation removed from them the burden of such additional expense, for the extra cost could simply be absorbed into the rate base or expenses, allowing extra profits from the higher prices to flow upstream to Western rather than to its non-Bell competition.

Even so, the pass-through of higher costs seems only a minor concern to the court relative to the “three hats” worn by AT&T and its subsidiaries in the (1) setting of standards, (2) counseling of operating companies in their equipment purchases, and (3) production of equipment for sale to the operating companies [emphasis added]:

The government’s evidence has depicted defendants as sole arbiters of what equipment is suitable for use in the Bell System a role that carries with it a power of subjective judgment that can be and has been used to advance the sale of Western Electric’s products at the expense of the general trade. First, AT&T, in conjunction with Bell Labs and Western Electric, sets the technical standards under which the telephone network operates and the compatibility specifications which equipment must meet. Second, Western Electric and Bell Labs … serve as counselors to the Operating Companies in their procurement decisions, ostensibly helping them to purchase equipment that meets network standards. Third, Western also produces equipment for sale to the Operating Companies in competition with general trade manufacturers.

The upshot of this “wearing of three hats” is, according to the government’s evidence, a rather obviously anticompetitive situation. By setting technical or compatibility standards and by either not communicating these standards to the general trade or changing them in mid-stream, AT&T has the capacity to remove, and has in fact removed, general trade products from serious consideration by the Operating Companies on “network integrity” grounds. By either refusing to evaluate general trade products for the Operating Companies or producing biased or speculative evaluations, AT&T has been able to influence the Operating Companies, which lack independent means to evaluate general trade products, to buy Western. And the in-house production and sale of Western equipment provides AT&T with a powerful incentive to exercise its “approval” power to discriminate against Western’s competitors.

It’s important to keep in mind that rate of return regulation was not thrust upon AT&T, it was a quid pro quo in which state and federal regulators acted to eliminate AT&T/Bell competitors in exchange for price regulation. In a floor speech to Congress in 1921, Rep. William J. Graham declared:

It is believed to be better policy to have one telephone system in a community that serves all the people, even though it may be at an advanced rate, property regulated by State boards or commissions, than it is to have two competing telephone systems.

For purposes of Salop and Culley’s integration-to-evade-price-regulation example, it’s important to keep in mind that AT&T acquired Western Electric in 1882, or about two decades before telephone pricing regulation was contemplated and eight years before the Sherman Antitrust Act. While AT&T may have used vertical integration to take advantage of rate-of-return price regulation, it’s simply not true that AT&T acquired Western Electric to evade price controls.

Salop and Culley provide a more recent example:

Example: Potential evasion of regulation concerns were raised in the FTC’s analysis in 2008 of the Fresenius/Daiichi Sankyo exclusive sub-license for a Daiichi Sankyo pharmaceutical used in Fresenius’ dialysis clinics, which potentially could allow evasion of Medicare pricing regulations.

As with the AT&T example, this example is not about evasion of price controls. Rather it raises concerns about taking advantage of Medicare’s pricing formula.

At the time of the deal, Medicare reimbursed dialysis clinics based on a drug manufacturer’s Average Sales Price (“ASP”) plus six percent, where ASP was calculated by averaging the prices paid by all customers, including any discounts or rebates.

The FTC argued by setting an artificially high transfer price of the drug to Fresenius, the ASP would increase, thereby increasing the Medicare reimbursement to all clinics providing the same drug (which not only would increase the costs to Medicare but also would increase income to all clinics providing the drug). Although the FTC claims this would be anticompetitive, the agency does not describe in what ways competition would be harmed.

The FTC introduces an interesting wrinkle in noting that a few years after the deal would have been completed, “substantial changes to the Medicare program relating to dialysis services … would eliminate the regulations that give rise to the concerns created by the proposed transaction.” Specifically, payment for dialysis services would shift from fee-for-service to capitation.

This wrinkle highlights a serious problem with a presumption that any purported evasion of price controls is an antitrust violation. Namely, if the controls go away, so does the antitrust violation.

Conversely–as Salop and Culley seem to argue with their AT&T example–a vertical merger could be retroactively declared anticompetitive if price controls are imposed after the merger is completed (even decades later and even if the price regulations were never anticipated at the time of the merger).

It’s one thing to argue that avoiding price regulation runs counter to public interest, but it’s another thing to argue that avoiding price regulation is anticompetitive. Indeed, as Stigler argues, if the price controls stifle competition, then avoidance of the controls may enhance competition. Placing such mergers under heightened scrutiny, such as an anticompetitive presumption, is a solution in search of a problem.