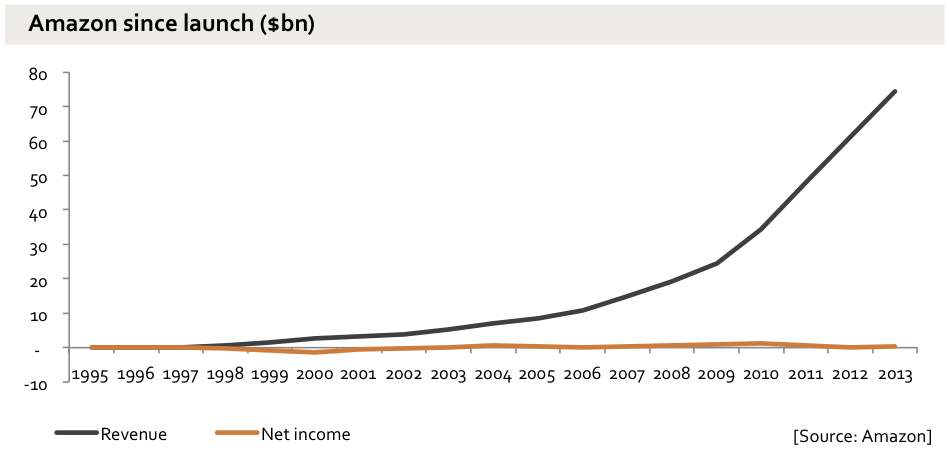

In 2014, Benedict Evans, a venture capitalist at Andreessen Horowitz, wrote “Why Amazon Has No Profits (And Why It Works),” a blog post in which he tried to explain Amazon’s business model. He began with a chart of Amazon’s revenue and net income that has now become (in)famous:

Source: Benedict Evans

A question inevitably followed in antitrust circles: How can a company that makes so little profit on so much revenue be worth so much money? It must be predatory pricing!

Predatory pricing is a rather rare anticompetitive practice because the “predator” runs the risk of bankrupting itself in the process of trying to drive rivals out of business with below-cost pricing. Furthermore, even if a predator successfully clears the field of competition, in developed markets with deep capital markets, keeping out new entrants is extremely unlikely.

Nonetheless, in those rare cases where plaintiffs can demonstrate that a firm actually has a viable scheme to drive competitors from the market with prices that are “too low” and has the ability to recoup its losses once it has cleared the market of those competitors, plaintiffs (including the DOJ) can prevail in court.

In other words, whoa if true.

Khan’s Predatory Pricing Accusation

In 2017, Lina Khan, then a law student at Yale, published “Amazon’s Antitrust Paradox” in a note for the Yale Law Journal and used Evans’ chart as supporting evidence that Amazon was guilty of predatory pricing. In the abstract she says, “Although Amazon has clocked staggering growth, it generates meager profits, choosing to price below-cost and expand widely instead.”

But if Amazon is selling below-cost, where does the money come from to finance those losses?

In her article, Khan hinted at two potential explanations: (1) Amazon is using profits from the cloud computing division (AWS) to cross-subsidize losses in the retail division or (2) Amazon is using money from investors to subsidize short-term losses:

Recently, Amazon has started reporting consistent profits, largely due to the success of Amazon Web Services, its cloud computing business. Its North America retail business runs on much thinner margins, and its international retail business still runs at a loss. But for the vast majority of its twenty years in business, losses—not profits—were the norm. Through 2013, Amazon had generated a positive net income in just over half of its financial reporting quarters. Even in quarters in which it did enter the black, its margins were razor-thin, despite astounding growth.

…

Just as striking as Amazon’s lack of interest in generating profit has been investors’ willingness to back the company. With the exception of a few quarters in 2014, Amazon’s shareholders have poured money in despite the company’s penchant for losses.

…

Revising predatory pricing doctrine to reflect the economics of platform markets, where firms can sink money for years given unlimited investor backing, would require abandoning the recoupment requirement in cases of below-cost pricing by dominant platforms.

Below-Cost Pricing Not Subsidized by Investors

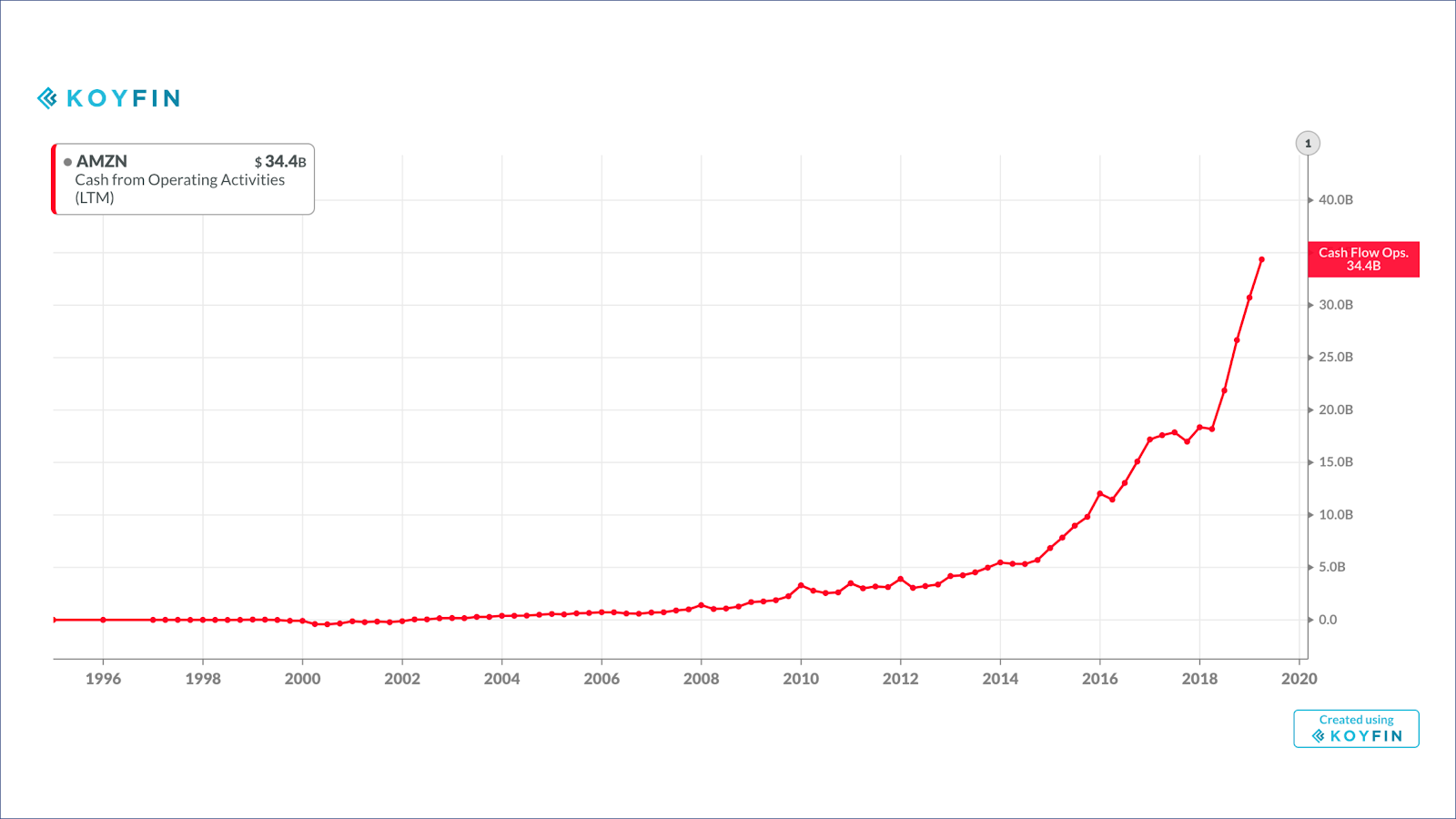

But neither explanation withstands scrutiny. First, the money is not from investors. Amazon has not raised equity financing since 2003. Nor is it debt financing: The company’s net debt position has been near-zero or negative for its entire history (excluding the Whole Foods acquisition):

Source: Benedict Evans

Amazon does not require new outside financing because it has had positive operating cash flow since 2002:

Notably for a piece of analysis attempting to explain Amazon’s business practices, the text of Khan’s 93-page law review article does not include the word “cash” even once.

Below-Cost Pricing Not Cross-Subsidized by AWS

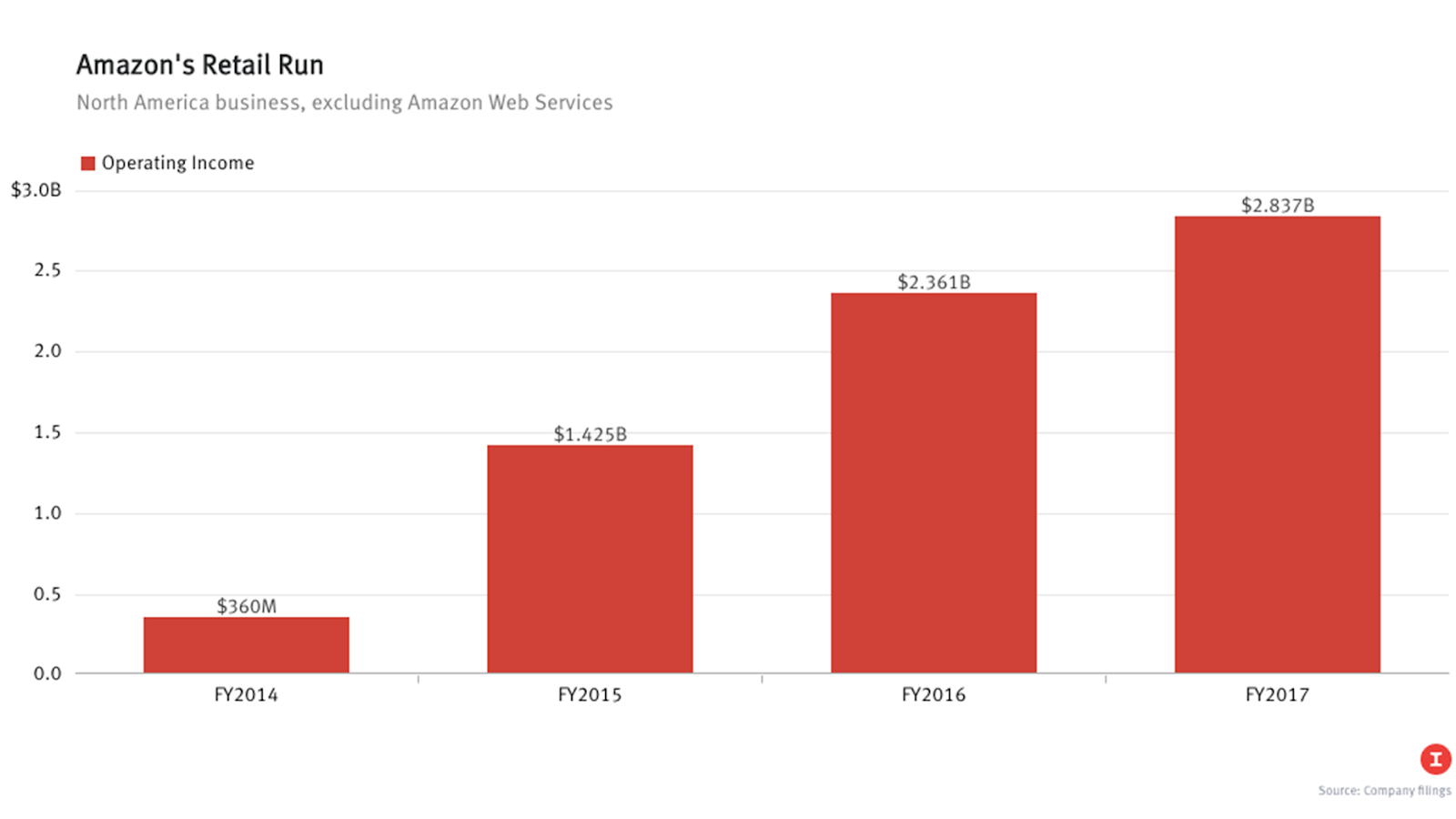

Source: The Information

As Priya Anand observed in a recent piece for The Information, since Amazon started breaking out AWS in its financials, operating income for the North America retail business has been significantly positive:

But [Khan] underplays its retail profits in the U.S., where the antitrust debate is focused. As the above chart shows, its North America operation has been profitable for years, and its operating income has been on the rise in recent quarters. While its North America retail operation has thinner margins than AWS, it still generated $2.84 billion in operating income last year, which isn’t exactly a rounding error compared to its $4.33 billion in AWS operating income.

Below-Cost Pricing in Retail Also Known as “Loss Leader” Pricing

Okay, so maybe Amazon isn’t using below-cost pricing in aggregate in its retail division. But it still could be using profits from some retail products to cross-subsidize below-cost pricing for other retail products (e.g., diapers), with the intention of driving competitors out of business to capture monopoly profits. This is essentially what Khan claims happened in the Diapers.com (Quidsi) case. But in the retail industry, diapers are explicitly cited as a loss leader that help retailers to develop a customer relationship with mothers in the hopes of selling them a higher volume of products over time. This is exactly what the founders of Diapers.com told Inc Magazine in a 2012 interview (emphasis added):

We saw brick-and-mortar stores, the Wal-Marts and Targets of the world, using these products to build relationships with mom and the end consumer, bringing them into the store and selling them everything else. So we thought that was an interesting model and maybe we could replicate that online. And so we started with selling the loss leader product to basically build a relationship with mom. And once they had the passion for the brand and they were shopping with us on a weekly or a monthly basis that they’d start to fall in love with that brand. We were losing money on every box of diapers that we sold. We weren’t able to buy direct from the manufacturers.

An anticompetitive scheme could be built into such bundling, but in many if not the overwhelming majority of these cases, consumers are the beneficiaries of lower prices and expanded output produced by these arrangements. It’s hard to definitively say whether any given firm that discounts its products is actually pricing below average variable cost (“AVC”) without far more granular accounting ledgers than are typically maintained. This is part of the reason why these cases can be so hard to prove.

A successful predatory pricing strategy also requires blocking market entry when the predator eventually raises prices. But the Diapers.com case is an explicit example of repeated entry that would defeat recoupment. In an article for the American Enterprise Institute, Jeffrey Eisenach shares the rest of the story following Amazon’s acquisition of Diapers.com:

Amazon’s conduct did not result in a diaper-retailing monopoly. Far from it. According to Khan, Amazon had about 43 percent of online sales in 2016 — compared with Walmart at 23 percent and Target with 18 percent — and since many people still buy diapers at the grocery store, real shares are far lower.

…

In the end, Quidsi proved to be a bad investment for Amazon: After spending $545 million to buy the firm and operating it as a stand-alone business for more than six years, it announced in April 2017 it was shutting down all of Quidsi’s operations, Diapers.com included. In the meantime, Quidsi’s founders poured the proceeds of the Amazon sale into a new online retailer — Jet.com — which was purchased by Walmart in 2016 for $3.3 billion. Jet.com cofounder Marc Lore now runs Walmart’s e-commerce operations and has said publicly that his goal is to surpass Amazon as the top online retailer.

Sussman’s Predatory Pricing Accusation

Earlier this year, Shaoul Sussman, a law student at Fordham University, published “Prime Predator: Amazon and the Rationale of Below Average Variable Cost Pricing Strategies Among Negative-Cash Flow Firms” in the Journal of Antitrust Enforcement. The article, which was written up by David Dayen for In These Times, presents a novel two-part argument for how Amazon might be profitably engaging in predatory pricing without raising prices:

- Amazon’s “True” Cash Flow Is Negative

Sussman argues that the company has been inflating its free cash flow numbers by excluding “capital leases.” According to Sussman, “If all of those expenses as detailed in its statements are accounted for, Amazon experienced a negative cash outflow of $1.461 billion in 2017.” Even though it’s not dispositive of predatory pricing on its own, Sussman believes that a negative free cash flow implies the company has been selling below-cost to gain market share.

2. Amazon Recoups Losses By Lowering AVC, Not By Raising Prices

Instead of raising prices to recoup losses from pricing below-cost, Sussman argues that Amazon flies under the antitrust radar by keeping consumer prices low and progressively decreasing AVC, ostensibly through using its monopsony power to offload costs on suppliers and partners (although this point is not fully explored in his piece).

But Sussman’s argument contains errors in both legal reasoning as well as its underlying empirical assumptions.

Below-cost pricing?

While there are many different ways to calculate the “cost” of a product or service, generally speaking, “below-cost pricing” means the price is less than marginal cost or AVC. Typically, courts tend to rely on AVC when dealing with predatory pricing cases. And as Herbert Hovenkamp has noted, proving that a price falls below the AVC is exceedingly difficult, particularly when dealing with firms in dynamic markets that sell a number of differentiated but complementary goods or services. Amazon, the focus of Sussman’s article, is a useful example here.

When products are complements, or can otherwise be bundled, firms may also be able to offer discounts that are unprofitable when selling single items. In business this is known as the “razor and blades model” (i.e., sell the razor handle below-cost one time and recoup losses on future sales of blades — although it’s not clear if this ever actually happens). Printer manufacturers are also an oft-cited example here, where printers are often sold below AVC in the expectation that the profits will be realized on the ongoing sale of ink. Amazon’s Kindle functions similarly: Amazon sells the Kindle around its AVC, ostensibly on the belief that it will realize a profit on selling e-books in the Kindle store.

Yet, even ignoring this common and broadly inoffensive practice, Sussman’s argument is odd. In essence, he claims that Amazon is concealing some of its costs in the form of capital leases in an effort to conceal its below-AVC pricing while it works to simultaneously lower its real AVC below the prices it charges consumers. At the end of this process, once its real AVC is actually sufficiently below consumers prices, it will (so the argument goes) be in the position of a monopolist reaping monopoly profits.

The problem with this argument should be immediately apparent. For the moment, let’s ignore the classic recoupment problem where new entrants will be drawn into the market to win some of those monopoly prices based on the new AVC that is possible. The real problem with his logic is that Sussman basically suggests that if Amazon sharply lowers AVC — that is it makes production massively more efficient — and then does not drop prices, they are a “predator.” But by pricing below its AVC in the first place, consumers in essence were given a loan by Amazon — they were able to enjoy what Sussman believes are radically low prices while Amazon works to actually make those prices possible through creating production efficiencies. It seems rather strange to punish a firm for loaning consumers a large measure of wealth. Its doubly odd when you then re-factor the recoupment problem back in: as soon as other firms figure out that a lower AVC is possible, they will enter the market and bid away any monopoly profits from Amazon.

Sussman’s Technical Analysis Is Flawed

While there are issues with Sussman’s general theory of harm, there are also some specific problems with his technical analysis of Amazon’s financial statements.

Capital Leases Are a Fixed Cost

First, capital leases should be not be included in cost calculations for a predatory pricing case because they are fixed — not variable — costs. Again, “below-cost” claims in predatory pricing cases generally use AVC (and sometimes marginal cost) as relevant cost measures.

Capital Leases Are Mostly for Server Farms

Second, the usual story is that Amazon uses its wildly-profitable Amazon Web Services (AWS) division to subsidize predatory pricing in its retail division. But Amazon’s “capital leases” — Sussman’s hidden costs in the free cash flow calculations — are mostly for AWS capital expenditures (i.e., server farms).

According to the most recent annual report: “Property and equipment acquired under capital leases was $5.7 billion, $9.6 billion, and $10.6 billion in 2016, 2017, and 2018, with the increase reflecting investments in support of continued business growth primarily due to investments in technology infrastructure for AWS, which investments we expect to continue over time.”

In other words, any adjustments to the free cash flow numbers for capital leases would make Amazon Web Services appear less profitable, and would not have a large effect on the accounting for Amazon’s retail operation (the only division thus far accused of predatory pricing).

Look at Operating Cash Flow Instead of Free Cash Flow

Again, while cash flow measures cannot prove or disprove the existence of predatory pricing, a positive cash flow measure should make us more skeptical of such accusations. In the retail sector, operating cash flow is the appropriate metric to consider. As shown above, Amazon has had positive (and increasing) operating cash flow since 2002.

Your Theory of Harm Is Also Known as “Investment”

Third, in general, Sussman’s novel predatory pricing theory is indistinguishable from pro-competitive behavior in an industry with high fixed costs. From the abstract (emphasis added):

[N]egative cash flow firm[s] … can achieve greater market share through predatory pricing strategies that involve long-term below average variable cost prices … By charging prices in the present reflecting future lower costs based on prospective technological and scale efficiencies, these firms are able to rationalize their predatory pricing practices to investors and shareholders.

“’Charging prices in the present reflecting future lower costs based on prospective technological and scale efficiencies” is literally what it means to invest in capex and R&D.

Sussman’s paper presents a clever attempt to work around the doctrinal limitations on predatory pricing. But, if courts seriously adopt an approach like this, they will be putting in place a legal apparatus that quite explicitly focuses on discouraging investment. This is one of the last things we should want antitrust law to be doing.