The once-mighty Blockbuster video chain is now down to a single store, in Bend, Oregon. It appears to be the only video rental store in Bend, aside from those offering “adult” features. Does that make Blockbuster a monopoly?

It seems almost silly to ask if the last firm in a dying industry is a monopolist. But, it’s just as silly to ask if the first firm in an emerging industry is a monopolist. They’re silly questions because they focus on the monopoly itself, rather than the alternative—what if the firm, and therefore the industry—did not exist at all.

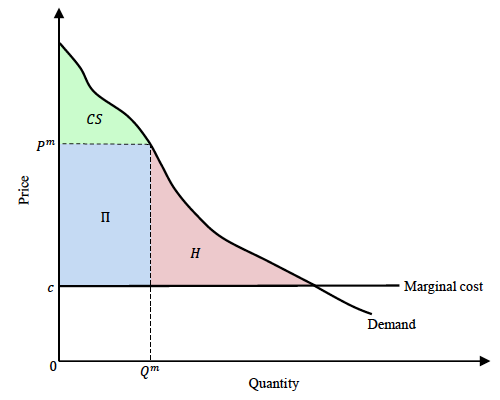

A recent post on CEPR’s Vox blog points out something very obvious, but often forgotten: “The deadweight loss from a monopolist’s not producing at all can be much greater than from charging too high a price.”

The figure below is from the post, by Michael Kremer, Christopher Snyder, and Albert Chen. With monopoly pricing (and no price discrimination), consumer surplus is given by CS, profit is given by ?, and a deadweight loss given by H.

The authors point out if fixed costs (or entry costs) are so high that the firm does not enter the market, the deadweight loss is equal to CS + H.

Too often, competition authorities fall for the Nirvana Fallacy, a tendency to compare messy, real-world economic circumstances today to idealized potential alternatives and to justify policies on the basis of the discrepancy between the real world and some alternative perfect (or near-perfect) world.

In 2005, Blockbuster dropped its bid to acquire competing Hollywood Entertainment Corporation, the then-second-largest video rental chain. Blockbuster said it expected the Federal Trade Commission would reject the deal on antitrust grounds. The merged companies would have made up more than 50 percent of the home video rental market.

Five years later Blockbuster, Hollywood, and third-place Movie Gallery had all filed for bankruptcy.

Blockbuster’s then-CEO, John Antioco, has been ridiculed for passing up an opportunity to buy Netflix for $50 million in 2005. But, Blockbuster knew its retail world was changing and had thought a consolidation might help it survive that change.

But, just as Antioco can be chided for undervaluing Netflix, so should the FTC. The regulators were so focused on Blockbuster-Hollywood market share that they undervalued the competitive pressure Netflix and other services were bringing. With hindsight, it seems obvious that the Blockbuster’s post-merger market share would not have conveyed any significant power over price. What’s not known is whether the merger would have put off the bankruptcy of the three largest video rental retailers.

Also, what’s not known is the extent to which consumers are better or worse off with the exit of Blockbuster, Hollywood, and Movie Gallery.

Nevertheless, the video rental business highlights a key point in an earlier TOTM post: A great deal of competition comes from the flanks, rather than head-on. Head-on competition from rental kiosks, such as Redbox, nibbled at the sales and margins of Blockbuster, Hollywood, and Movie Gallery. But, the real killer of the bricks-and-mortar stores came from a wide range of streaming services.

The lesson for regulators is that competition is nearly always and everywhere present, even if it’s standing on the sidelines.