[TOTM: The following is part of a symposium by TOTM guests and authors on the 2020 Vertical Merger Guidelines. The entire series of posts is available here.

This post is authored by Geoffrey A. Manne (President & Founder, ICLE; Distinguished Fellow, Northwestern University Center on Law, Business, and Economics ); and Kristian Stout (Associate Director, ICLE).]

As many in the symposium have noted — and as was repeatedly noted during the FTC’s Hearings on Competition and Consumer Protection in the 21st Century — there is widespread dissatisfaction with the 1984 Non-Horizontal Merger Guidelines.

Although it is doubtless correct that the 1984 guidelines don’t reflect the latest economic knowledge, it is by no means clear that this has actually been a problem — or that a new set of guidelines wouldn’t create even greater problems. Indeed, as others have noted in this symposium, there is a great deal of ambiguity in the proposed guidelines that could lead either to uncertainty as to how the agencies will exercise their discretion, or, more troublingly, could lead courts to take seriously speculative theories of harm.

We can do little better in expressing our reservations that new guidelines are needed than did the current Chairman of the FTC, Joe Simons, writing on this very blog in a symposium on what became the 2010 Horizontal Merger Guidelines. In a post entitled, Revisions to the Merger Guidelines: Above All, Do No Harm, Simons writes:

My sense is that there is no need to revise the DOJ/FTC Horizontal Merger Guidelines, with one exception…. The current guidelines lay out the general framework quite well and any change in language relative to that framework are likely to create more confusion rather than less. Based on my own experience, the business community has had a good sense of how the agencies conduct merger analysis…. If, however, the current administration intends to materially change the way merger analysis is conducted at the agencies, then perhaps greater revision makes more sense. But even then, perhaps the best approach is to try out some of the contemplated changes (i.e. in actual investigations) and publicize them in speeches and the like before memorializing them in a document that is likely to have some substantial permanence to it.

Wise words. Unless, of course, “the current [FTC] intends to materially change the way [vertical] merger analysis is conducted.” But the draft guidelines don’t really appear to portend a substantial change, and in several ways they pretty accurately reflect agency practice.

What we want to draw attention to, however, is an implicit underpinning of the draft guidelines that we believe the agencies should clearly disavow (or at least explain more clearly the complexity surrounding): the extent and implications of the presumed functional equivalence of vertical integration by contract and by merger — the contract/merger equivalency assumption.

Vertical mergers and their discontents

The contract/merger equivalency assumption has been gaining traction with antitrust scholars, but it is perhaps most clearly represented in some of Steve Salop’s work. Salop generally believes that vertical merger enforcement should be heightened. Among his criticisms of current enforcement is his contention that efficiencies that can be realized by merger can often also be achieved by contract. As he discussed during his keynote presentation at last year’s FTC hearing on vertical mergers:

And, finally, the key policy issue is the issue is not about whether or not there are efficiencies; the issue is whether the efficiencies are merger-specific. As I pointed out before, Coase stressed that you can get vertical integration by contract. Very often, you can achieve the vertical efficiencies if they occur, but with contracts rather than having to merge.

And later, in the discussion following his talk:

If there is vertical integration by contract… it meant you could get all the efficiencies from vertical integration with a contract. You did not actually need the vertical integration.

Salop thus argues that because the existence of a “contract solution” to firm problems can often generate the same sorts of efficiencies as when firms opt to merge, enforcers and courts should generally adopt a presumption against vertical mergers relative to contracting:

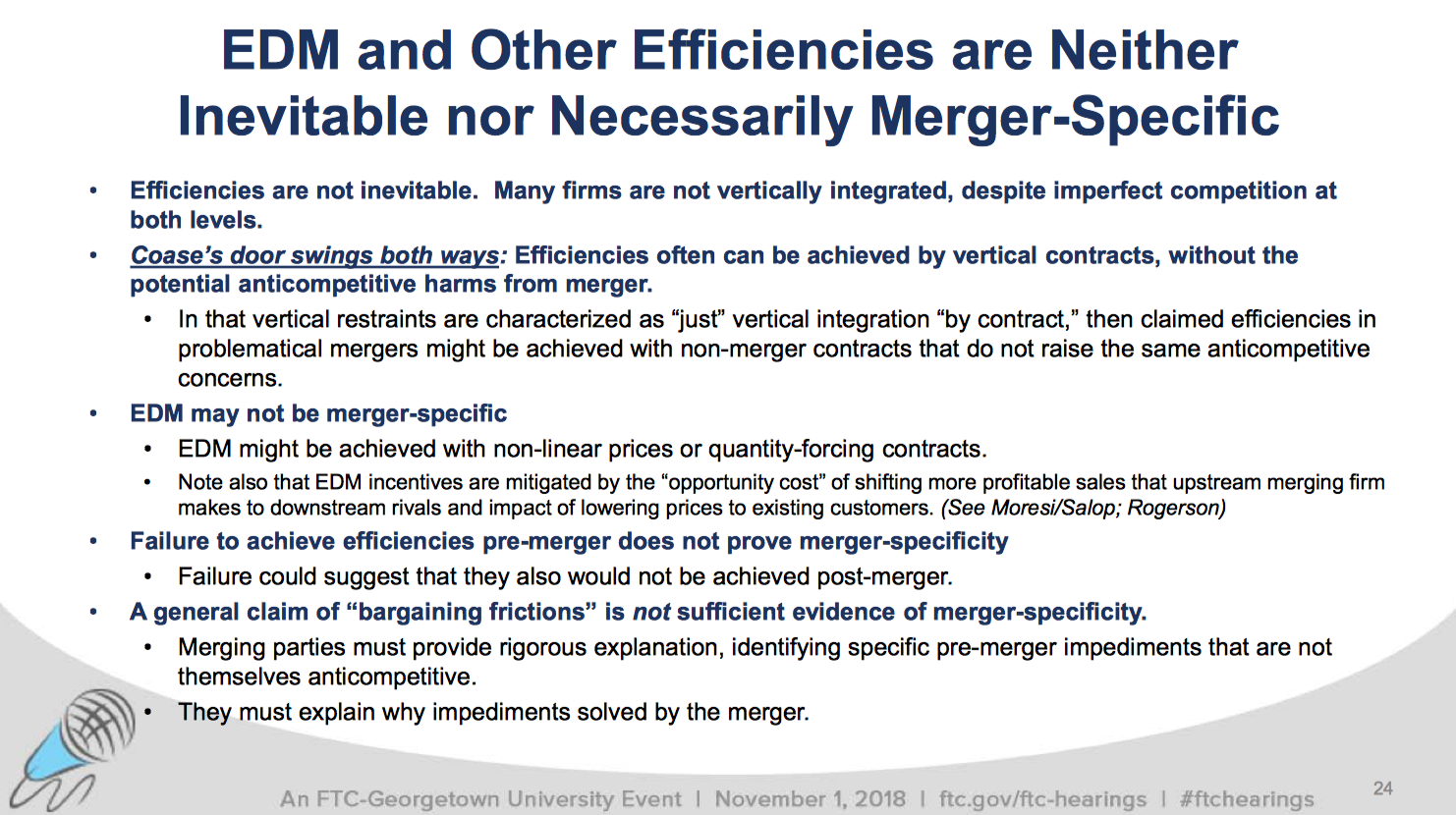

Coase’s door swings both ways: Efficiencies often can be achieved by vertical contracts, without the potential anticompetitive harms from merger.

In that vertical restraints are characterized as “just” vertical integration “by contract,” then claimed efficiencies in problematical mergers might be achieved with non-merger contracts that do not raise the same anticompetitive concerns. (emphasis in original)

(Salop isn’t alone in drawing such a conclusion, of course; Carl Shapiro, for example, has made a similar point (as have others)).

In our next post we explore the policy errors implicated by this contract/merger equivalency assumption. But here we want to consider whether it makes logical sense in the first place.

The logic of vertical integration is not commutative

It is true that, where contracts are observed, they are likely as (or more, actually) efficient than merger. But, by the same token, it is also true that where mergers are observed they are likely more efficient than contracts. Indeed, the entire reason for integration is efficiency relative to what could be done by contract — this is the essence of the so-called “make-or-buy” decision.

For example, a firm that decides to buy its own warehouse has determined that doing so is more efficient than renting warehouse space. Some of these efficiencies can be measured and quantified (e.g., carrying costs of ownership vs. the cost of rent), but many efficiencies cannot be easily measured or quantified (e.g., layout of the facility or site security). Under the contract/merger equivalency assumption, the benefits of owning a warehouse can be achieved “very often” by renting warehouse space. But the fact that many firms using warehouses own some space and rent some space indicates that the make-or-buy decision is often unique to each firm’s idiosyncratic situation. Moreover, the distinctions driving those differences will not always be readily apparent, and whether contracting or integrating is preferable in any given situation may not be inferred from the existence of one or the other elsewhere in the market — or even in the same firm!

There is no reason to presume in any given situation that the outcome from contracting would be the same as from merging, even where both are notionally feasible. The two are, quite simply, different bargaining environments, each with a different risk and cost allocation; accounting treatment; effect on employees, customers, and investors; tax consequence, etc. Even if the parties accomplished nominally “identical” outcomes, they would not, in fact, be identical.

Meanwhile, what if the reason for failure to contract, or the reason to prefer merger, has nothing to do with efficiency? What if there were no anticompetitive aim but there were a tax advantage? What if one of the parties just wanted a larger firm in order to satisfy the CEO’s ego? That these are not cognizable efficiencies under antitrust law is clear. But the adoption of a presumption of equivalence between contract and merger would — ironically — entail their incorporation into antitrust law just the same — by virtue of their effective prohibition under antitrust law.

In other words, if the assumption is that contract and merger are equally efficient unless proven otherwise, but the law adopts a suspicion (or, even worse, a presumption) that vertical mergers are anticompetitive which can be rebutted only with highly burdensome evidence of net efficiency gain, this effectively deputizes antitrust law to enforce a preconceived notion of “merger appropriateness” that does not necessarily turn on efficiencies. There may (or may not) be sensible policy reasons for adopting such a stance, but they aren’t antitrust reasons.

More fundamentally, however, while there are surely some situations in which contractual restraints might be able to achieve similar organizational and efficiency gains as a merger, the practical realities of achieving not just greater efficiency, but a whole host of non-efficiency-related, yet nonetheless valid, goals, are rarely equivalent between the two.

It may be that the parties don’t know what they don’t know to such an extent that a contract would be too costly because it would be too incomplete, for example. But incomplete contracts and ambiguous control and ownership rights aren’t (as much of) an issue on an ongoing basis after a merger.

As noted, there is no basis for assuming that the structure of a merger and a contract would be identical. In the same way, there is no basis for assuming that the knowledge transfer that would result from a merger would be the same as that which would result from a contract — and in ways that the parties could even specify or reliably calculate in advance. Knowing that the prospect for knowledge “synergies” would be higher with a merger than a contract might be sufficient to induce the merger outcome. But asked to provide evidence that the parties could not engage in the same conduct via contract, the parties would be unable to do so. The consequence, then, would be the loss of potential gains from closer integration.

At the same time, the cavalier assumption that parties would be able — legally — to enter into an analogous contract in lieu of a merger is problematic, given that it would likely be precisely the form of contract (foreclosing downstream or upstream access) that is alleged to create problems with the merger in the first place.

At the FTC hearings last year, Francine LaFontaine highlighted this exact concern:

I want to reemphasize that there are also rules against vertical restraints in antitrust laws, and so to say that the firms could achieve the mergers outcome by using vertical restraints is kind of putting them in a circular motion where we are telling them you cannot merge because you could do it by contract, and then we say, but these contract terms are not acceptable.

Indeed, legal risk is one of the reasons why a merger might be preferable to a contract, and because the relevant markets here are oligopoly markets, the possibility of impermissible vertical restraints between large firms with significant market share is quite real.

More important, the assumptions underlying the contention that contracts and mergers are functionally equivalent legal devices fails to appreciate the importance of varied institutional environments. Consider that one reason some takeovers are hostile is because incumbent managers don’t want to merge, and often believe that they are running a company as well as it can be run — that a change of corporate control would not improve efficiency. The same presumptions may also underlie refusals to contract and, even more likely, may explain why, to the other firm, a contract would be ineffective.

But, while there is no way to contract without bilateral agreement, there is a corporate control mechanism to force a takeover. In this institutional environment a merger may be easier to realize than a contract (and that applies even to a consensual merger, of course, given the hostile outside option). In this case, again, the assumption that contract should be the relevant baseline and the preferred mechanism for coordination is misplaced — even if other firms in the industry are successfully accomplishing the same thing via contract, and even if a contract would be more “efficient” in the abstract.

Conclusion

Properly understood, the choice of whether to contract or merge derives from a host of complicated factors, many of which are difficult to observe and/or quantify. The contract/merger equivalency assumption — and the species of “least-restrictive alternative” reasoning that would demand onerous efficiency arguments to permit a merger when a contract was notionally possible — too readily glosses over these complications and unjustifiably embraces a relative hostility to vertical mergers at odds with both theory and evidence.

Rather, as has long been broadly recognized, there can be no legally relevant presumption drawn against a company when it chooses one method of vertical integration over another in the general case. The agencies should clarify in the draft guidelines that the mere possibility of integration via contract or the inability of merging parties to rigorously describe and quantify efficiencies does not condemn a proposed merger.