[TOTM: The following is part of a symposium by TOTM guests and authors on the 2020 Vertical Merger Guidelines. The entire series of posts is available here.

This post is authored by Eric Fruits (Chief Economist, International Center for Law & Economics and Professor of Economics, Portland State University).]

Vertical mergers are messy. They’re messy for the merging firms and they’re especially messy for regulators charged with advancing competition without advantaging competitors. Firms rarely undertake a vertical merger with an eye toward monopolizing a market. Nevertheless, competitors and competition authorities excel at conjuring up complex models that reveal potentially harmful consequences stemming from vertical mergers. In their post, Gregory J. Werden and Luke M. Froeb highlight the challenges in evaluating vertical mergers:

[V]ertical mergers produce anticompetitive effects only through indirect mechanisms with many moving parts, which makes the prediction of competitive effects from vertical mergers more complex and less certain.

There’s a recurring theme throughout this symposium: The current Vertical Merger Guidelines should be updated; the draft Guidelines are a good start, but they raise more questions than they answer. Other symposium posts have hit on the key ups and downs of the draft Guidelines.

In this post, I use the draft Guidelines’ examples to highlight how messy vertical mergers can be. The draft Guidelines’ examples are meant to clarify the government’s thinking on markets and mergers. In the end, however, they demonstrate the complexity in identifying relevant markets, related products, and the dynamic interaction of competition. I will focus on two examples provided in the draft Guidelines. Warning: you’re going to read a lot about oranges.

In the following example from the draft Guidelines, the relevant market is the wholesale supply of orange juice in region X and Company B’s supply of oranges is the related product:

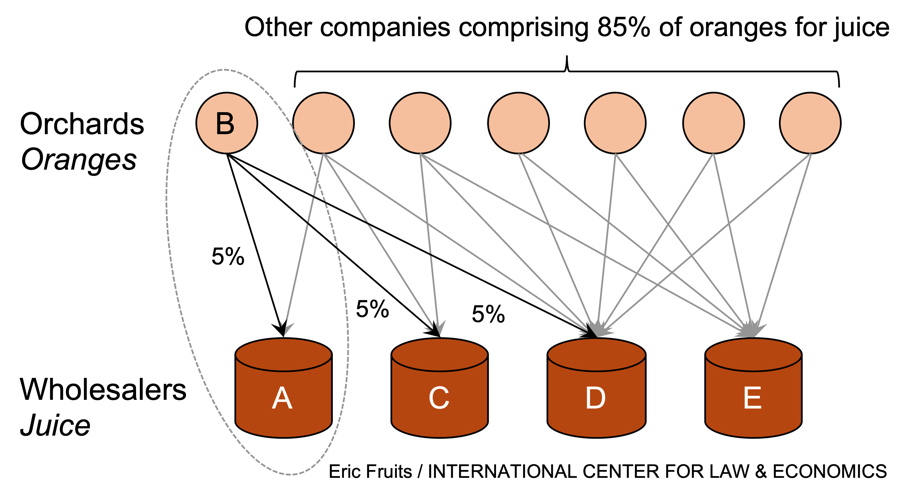

Example 2: Company A is a wholesale supplier of orange juice. It seeks to acquire Company B, an owner of orange orchards. The Agencies may consider whether the merger would lessen competition in the wholesale supply of orange juice in region X (the relevant market). The Agencies may identify Company B’s supply of oranges as the related product. Company B’s oranges are used in fifteen percent of the sales in the relevant market for wholesale supply of orange juice. The Agencies may consider the share of fifteen percent as one indicator of the competitive significance of the related product to participants in the relevant market.

The figure below illustrates one hypothetical structure. Company B supplies an equal amount of oranges to Company A and two other wholesalers, C and D, totalling 15 percent of orange juice sales in region X. Orchards owned by others account for the remaining 85 percent. For the sake of argument, assume all the wholesalers are the same size in which case Company B’s orchard would supply 20 percent of the oranges used by wholesalers A, C, and D.

Orange juice sold in a particular region is just one of many uses for oranges. The juice can be sold as fresh liquid, liquid from concentrate, or frozen concentrate. The fruit can be sold as fresh produce or it can be canned, frozen, or processed into marmalade. Many of these products can be sold outside of a particular region and can be sold outside of the United States. This is important in considering the next example from the draft Guidelines.

Example 3: In Example 2, the merged firm may be able to profitably stop supplying oranges (the related product) to rival orange juice suppliers (in the relevant market). The merged firm will lose the margin on the foregone sales of oranges but may benefit from increased sales of orange juice if foreclosed rivals would lose sales, and some of those sales were diverted to the merged firm. If the benefits outweighed the costs, the merged firm would find it profitable to foreclose. If the likely effect of the foreclosure were to substantially lessen competition in the orange juice market, the merger potentially raises significant competitive concerns and may warrant scrutiny.

This is the classic example of raising rivals’ costs. Under the standard formulation, the merged firm will produce oranges at the orchard’s marginal cost — in theory, the price it pays for oranges would be the same both pre- and post-merger. If orchard B does not sell its oranges to the non-integrated wholesalers C, D, and E, the other orchards will be able to charge a price greater than their marginal cost of production and greater than the pre-merger market price for oranges. The higher price of oranges used by non-integrated wholesalers will then be reflected in higher prices for orange juice sold by the wholesalers.

The merged firm’s juice prices will be higher post-merger because its unintegrated rivals’ juice prices will be higher, thus increasing the merged firm’s profits. The merged firm and unintegrated orchards would be the “winners;” unintegrated wholesalers and consumers would be the “losers.” Under a consumer welfare standard the result could be deemed anticompetitive. Under a total welfare standard, anything goes.

But, the classic example of raising rivals’ costs is based on some strong assumptions. It assumes that, pre-merger, all upstream firms price at marginal cost, which means there is no double marginalization. It assumes all the upstream firm’s products are perfectly identical. It assumes unintegrated firms don’t respond by integrating themselves. If one or more of these assumptions is not correct, more complex models — with additional (potentially unprovable) assumptions — must be employed. What begins as a seemingly straightforward theoretical example is now a battle of which expert’s models best fit the facts and best predicts the likely outcome.

In the draft Guidelines’ raising rivals’ costs example, it’s assumed the merged firm would refuse to sell oranges to rival downstream wholesalers. However, if rival orchards charge a sufficiently high price, the merged firm would profit from undercutting its rivals’ orange prices, while still charging a price greater than marginal cost. Thus, it’s not obvious that the merged firm has an incentive to cut off supply to downstream competitors. The extent of the pricing pressure on the merged firm to cheat on itself is an empirical matter that depends on how upstream and downstream firms react, or might react.

For example, using the figure above, if the merged firm stopped supplying oranges to rival wholesalers, then the merged firm’s orchard would supply 60 percent of the oranges used in the firm’s juice. Although wholesalers C and D would not get oranges from B’s orchards, they could obtain oranges from other orchards that are no longer supplying wholesaler A. In this case, the merged firm’s attempt at foreclosure would have no effect and there would be no harm to competition.

It’s possible the merged firm would divert some or all of its oranges to a “secondary” market, removing those oranges from the juice market. Rather than juicing oranges, the merged firm may decide to sell them as fresh produce; fresh citrus fruits account for 7 percent of Florida’s crop and 75% of California’s. This diversion would lead to a decline in the supply of oranges for juice and the price of this key input would rise.

But, as noted in the Guidelines’ example, this strategy would raise the merged firm’s costs along with its rivals. Moreover, rival orchards can respond to this strategy by diverting their own oranges from “secondary” markets to the juice market, in which case there may be no significant effect on the price of juice oranges. What begins as a seemingly straightforward theoretical example is now a complicated empirical matter. Or worse, it may just be a battle over which expert is the most convincing fortune teller.

Moreover, the merged firm may have legitimate business reasons for the merger and legitimate business reasons for reducing the supply of oranges to juice wholesalers. For example “citrus greening,” an incurable bacterial disease, has caused severe damage to Florida’s citrus industry, significantly reducing crop yields. A vertical merger could be one way to reduce supply risks. On the demand side, an increase in the demand for fresh oranges would guide firms to shift from juice and processed markets to the fresh market. What some would see as anticompetitive conduct, others would see as a natural and expected response to price signals.Because of the many alternative uses for oranges, it’s overly simplistic to declare that the supply of orange juice in a specific region is “the” relevant market. Orchards face a myriad of options in selling their products. Misshapen fruit can be juiced fresh or as frozen concentrate; smaller fruit can be canned or jellied. “Perfect” fruit can be sold as fresh produce, juice, canned, or jellied. Vertical integration with a juice wholesaler adds just one factor to the myriad factors affecting how and where an upstream supplier sells its products. Just as there is no single relevant market, in many cases there is no single related product — a fact that is especially relevant in vertical relationships. Unfortunately the draft Guidelines provide little guidance in these important areas.