Antitrust populists have a long list of complaints about competition policy, including: laws aren’t broad enough or tough enough, enforcers are lax, and judges tend to favor defendants over plaintiffs or government agencies. The populist push got a bump with the New York Times coverage of Lina Khan’s “Amazon’s Antitrust Paradox” in which she advocated breaking up Amazon and applying public utility regulation to platforms. Khan’s ideas were picked up by Sen. Elizabeth Warren, who has a plan for similar public utility regulation and promised to unwind earlier acquisitions by Amazon (Whole Foods and Zappos), Facebook (WhatsApp and Instagram), and Google (Waze, Nest, and DoubleClick).

Khan, Warren, and the other Break Up Big Tech populists don’t clearly articulate how consumers, suppliers — or anyone for that matter — would be better off with their mandated spinoffs. The Khan/Warren plan, however, requires a unique alignment of many factors: Warren must win the White House, Democrats must control both houses of Congress, and judges must substantially shift their thinking. It’s like turning a supertanker on a dime in the middle of a storm. Instead of publishing manifestos and engaging in antitrust hashtag hipsterism, maybe — just maybe — the populists can do something.

The populists seem to have three main grievances:

- Small firms cannot enter the market or cannot thrive once they enter;

- Suppliers, including workers, are getting squeezed; and

- Speculation that someday firms will wake up, realize they have a monopoly, and begin charging noncompetitive prices to consumers.

Each of these grievances can be, and has been, already addressed by antitrust and competition litigation. And, in many cases these grievances were addressed in private antitrust litigation. For example:

- Leegin v. PSKS, private antitrust litigation alleging anticompetitive vertical price restraints ;

- Weyerhaeuser v. Ross-Simmons, private antitrust litigation alleging predatory bidding of inputs;

- Apple v. Pepper, private antitrust litigation that chipped away at Illinois Brick’s indirect purchaser doctrine; and

- The European Commission’s Google Search investigation was prompted by complaints filed by a private party, Foundem.

In the US, private actions are available for a wide range of alleged anticompetitive conduct, including coordinated conduct (e.g., price-fixing), single-firm conduct (e.g., predatory pricing), and mergers that would substantially lessen competition.

If the antitrust populists are so confident that concentration is rising and firms are behaving anticompetitively and consumers/suppliers/workers are being harmed, then why don’t they organize an antitrust lawsuit against the worst of the worst violators? If anticompetitive activity is so obvious and so pervasive, finding compelling cases should be easy.

For example, earlier this year, Shaoul Sussman, a law student at Fordham University, published “Prime Predator: Amazon and the Rationale of Below Average Variable Cost Pricing Strategies Among Negative-Cash Flow Firms” in the Journal of Antitrust Enforcement. Why not put Sussman’s theory to the test by building an antitrust case around it? The discovery process would unleash a treasure trove of cost data and probably more than a few “hot docs.”

Khan argues:

While predatory pricing technically remains illegal, it is extremely difficult to win predatory pricing claims because courts now require proof that the alleged predator would be able to raise prices and recoup its losses.

However, in her criticism of the court in the Apple e-books litigation, she lays out a clear rationale for courts to revise their thinking on predatory pricing [emphasis added]:

Judge Cote, who presided over the district court trial, refrained from affirming the government’s conclusion. Still, the government’s argument illustrates the dominant framework that courts and enforcers use to analyze predation—and how it falls short. Specifically, the government erred by analyzing the profitability of Amazon’s e-book business in the aggregate and by characterizing the conduct as “loss leading” rather than potentially predatory pricing. These missteps suggest a failure to appreciate two critical aspects of Amazon’s practices: (1) how steep discounting by a firm on a platform-based product creates a higher risk that the firm will generate monopoly power than discounting on non-platform goods and (2) the multiple ways Amazon could recoup losses in ways other than raising the price of the same e-books that it discounted.

Why not put Khan’s cross-subsidy theory to the test by building an antitrust case around it? Surely there’d be a document explaining how the firm expects to recoup its losses. Or, maybe not. Maybe by the firm’s accounting, it’s not losing money on the discounted products. Without evidence, it’s just speculation.

In fairness, one can argue that recent court decisions have made pursuing private antitrust litigation more difficult. For example, the Supreme Court’s decision in Twombly requires an antitrust plaintiff to show more than mere speculation based on circumstantial evidence in order to move forward to discovery. Decisions in matters such as Ashcroft v. Iqbal have made it more difficult for plaintiffs to maintain antitrust claims. Wal-Mart v. Dukes and Comcast Corp v Behrend subject antitrust class actions to more rigorous analysis. In Ohio v. Amex the court ruled antitrust plaintiffs can’t meet the burden of proof by showing only some effect on some part of a two-sided market.

At the same time Jeld-Wen indicates third party plaintiffs can be awarded damages and obtain divestitures, even after mergers clear. In Jeld-Wen, a competitor filed suit to challenge the consummated Jeld-Wen/Craftmaster merger four years after the DOJ approved the merger without conditions. The challenge was lengthy, but successful, and a district court ordered damages and the divestiture of one of the combined firm’s manufacturing facilities six years after the merger was closed.

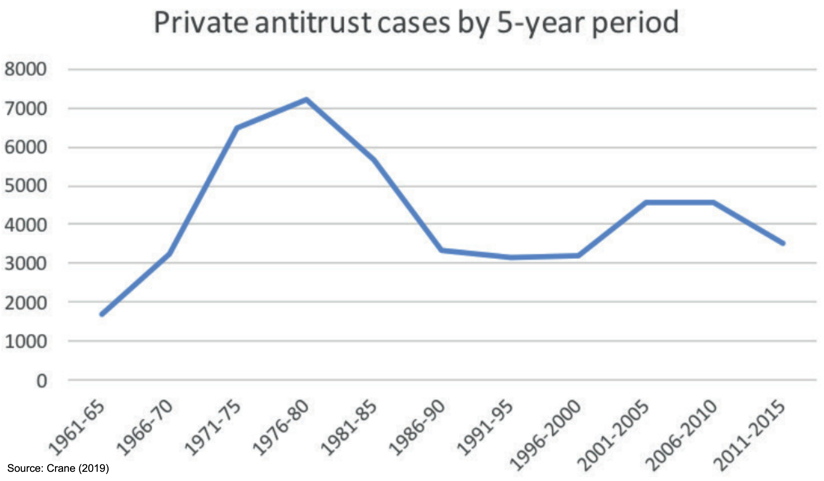

Despite the possible challenges of pursuing a private antitrust suit, Daniel Crane’s review of US federal court workload statistics concludes the incidence of private antitrust enforcement in the United States has been relatively stable since the mid-1980s — in the range of 600 to 900 new private antitrust filings a year. He also finds resolution by trial has been relatively stable at an average of less than 1 percent a year. Thus, it’s not clear that recent decisions have erected insurmountable barriers to antitrust plaintiffs.

In the US, third parties may fund private antitrust litigation and plaintiffs’ attorneys are allowed to work under a contingency fee arrangement, subject to court approval. A compelling case could be funded by deep-pocketed supporters of the populists’ agenda, big tech haters, or even investors. Perhaps the most well-known example is Peter Thiel’s bankrolling of Hulk Hogan’s takedown of Gawker. Before that, the savings and loan crisis led to a number of forced mergers which were later challenged in court, with the costs partially funded by the issuance of litigation tracking warrants.

The antitrust populist ranks are chock-a-block with economists, policy wonks, and go-getter attorneys. If they are so confident in their claims of rising concentration, bad behavior, and harm to consumers, suppliers, and workers, then they should put those ideas to the test with some slam dunk litigation. The fact that they haven’t suggests they may not have a case.