The courtroom trial in the Federal Trade Commission’s (FTC’s) antitrust case against Qualcomm ended in January with a promise from the judge in the case, Judge Lucy Koh, to issue a ruling as quickly as possible — caveated by her acknowledgement that the case is complicated and the evidence voluminous. Well, things have only gotten more complicated since the end of the trial. Not only did Apple and Qualcomm reach a settlement in the antitrust case against Qualcomm that Apple filed just three days after the FTC brought its suit, but the abbreviated trial in that case saw the presentation by Qualcomm of some damning evidence that, if accurate, seriously calls into (further) question the merits of the FTC’s case.

Apple v. Qualcomm settles — and the DOJ takes notice

The Apple v. Qualcomm case, which was based on substantially the same arguments brought by the FTC in its case, ended abruptly last month after only a day and a half of trial — just enough time for the parties to make their opening statements — when Apple and Qualcomm reached an out-of-court settlement. The settlement includes a six-year global patent licensing deal, a multi-year chip supplier agreement, an end to all of the patent disputes around the world between the two companies, and a $4.5 billion settlement payment from Apple to Qualcomm.

That alone complicates the economic environment into which Judge Koh will issue her ruling. But the Apple v. Qualcomm trial also appears to have induced the Department of Justice Antitrust Division (DOJ) to weigh in on the FTC’s case with a Statement of Interest requesting Judge Koh to use caution in fashioning a remedy in the case should she side with the FTC, followed by a somewhat snarky Reply from the FTC arguing the DOJ’s filing was untimely (and, reading the not-so-hidden subtext, unwelcome).

But buried in the DOJ’s Statement is an important indication of why it filed its Statement when it did, just about a week after the end of the Apple v. Qualcomm case, and a pointer to a much larger issue that calls the FTC’s case against Qualcomm even further into question (I previously wrote about the lack of theoretical and evidentiary merit in the FTC’s case here).

Footnote 6 of the DOJ’s Statement reads:

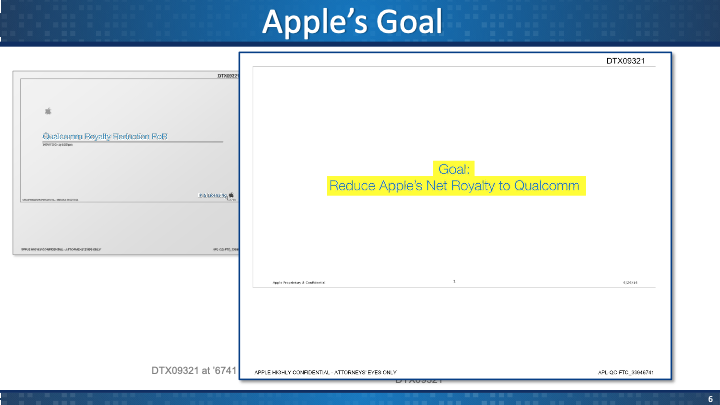

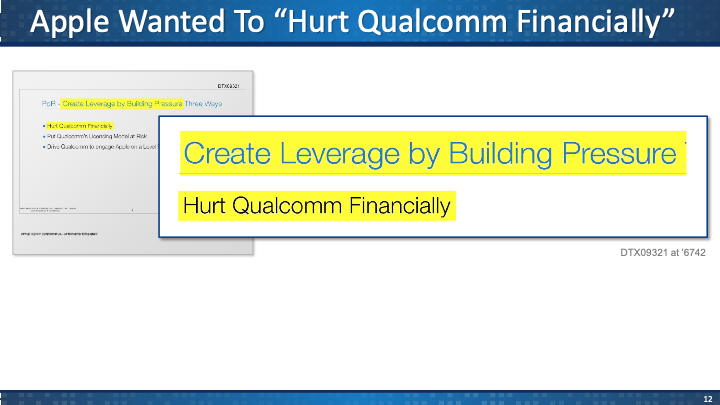

Internal Apple documents that recently became public describe how, in an effort to “[r]educe Apple’s net royalty to Qualcomm,” Apple planned to “[h]urt Qualcomm financially” and “[p]ut Qualcomm’s licensing model at risk,” including by filing lawsuits raising claims similar to the FTC’s claims in this case …. One commentator has observed that these documents “potentially reveal[] that Apple was engaging in a bad faith argument both in front of antitrust enforcers as well as the legal courts about the actual value and nature of Qualcomm’s patented innovation.” (Emphasis added).

Indeed, the slides presented by Qualcomm during that single day of trial in Apple v. Qualcomm are significant, not only for what they say about Apple’s conduct, but, more importantly, for what they say about the evidentiary basis for the FTC’s claims against the company.

The evidence presented by Qualcomm in its opening statement suggests some troubling conduct by Apple

Others have pointed to Qualcomm’s opening slides and the Apple internal documents they present to note Apple’s apparent bad conduct. As one commentator sums it up:

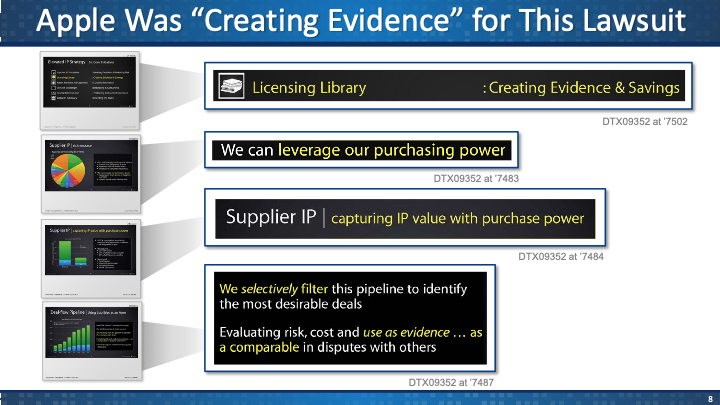

Although we really only managed to get a small glimpse of Qualcomm’s evidence demonstrating the extent of Apple’s coordinated strategy to manipulate the FRAND license rate, that glimpse was particularly enlightening. It demonstrated a decade-long coordinated effort within Apple to systematically engage in what can only fairly be described as manipulation (if not creation of evidence) and classic holdout.

Qualcomm showed during opening arguments that, dating back to at least 2009, Apple had been laying the foundation for challenging its longstanding relationship with Qualcomm. (Emphasis added).

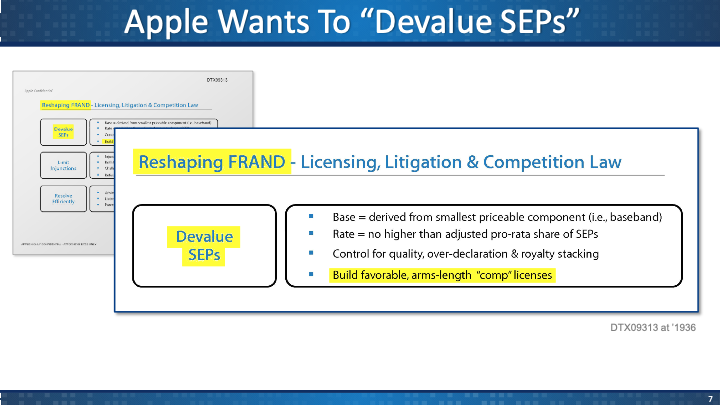

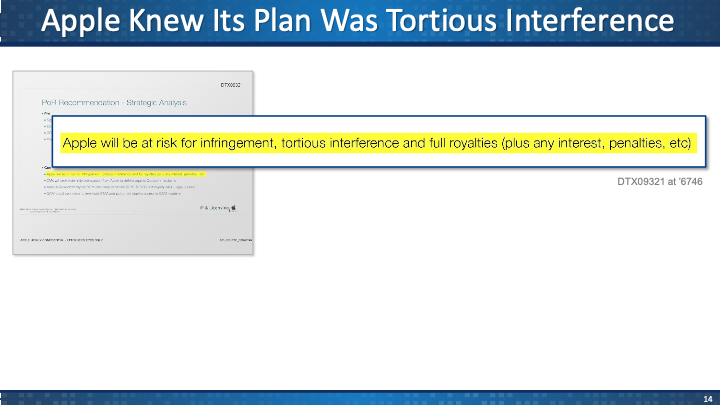

The internal Apple documents presented by Qualcomm to corroborate this claim appear quite damning. Of course, absent explanation and cross-examination, it’s impossible to know for certain what the documents mean. But on their face they suggest Apple knowingly undertook a deliberate scheme (and knowingly took upon itself significant legal risk in doing so) to devalue comparable patent portfolios to Qualcomm’s:

The apparent purpose of this scheme was to devalue comparable patent licensing agreements where Apple had the power to do so (through litigation or the threat of litigation) in order to then use those agreements to argue that Qualcomm’s royalty rates were above the allowable, FRAND level, and to undermine the royalties Qualcomm would be awarded in courts adjudicating its FRAND disputes with the company. As one commentator put it:

Apple embarked upon a coordinated scheme to challenge weaker patents in order to beat down licensing prices. Once the challenges to those weaker patents were successful, and the licensing rates paid to those with weaker patent portfolios were minimized, Apple would use the lower prices paid for weaker patent portfolios as proof that Qualcomm was charging a super-competitive licensing price; a licensing price that violated Qualcomm’s FRAND obligations. (Emphasis added).

That alone is a startling revelation, if accurate, and one that would seem to undermine claims that patent holdout isn’t a real problem. It also would undermine Apple’s claims that it is a “willing licensee,” engaging with SEP licensors in good faith. (Indeed, this has been called into question before, and one Federal Circuit judge has noted in dissent that “[t]he record in this case shows evidence that Apple may have been a hold out.”). If the implications drawn from the Apple documents shown in Qualcomm’s opening statement are accurate, there is good reason to doubt that Apple has been acting in good faith.

Even more troubling is what it means for the strength of the FTC’s case

But the evidence offered in Qualcomm’s opening argument point to another, more troubling implication, as well. We know that Apple has been coordinating with the FTC and was likely an important impetus for the FTC’s decision to bring an action in the first place. It seems reasonable to assume that Apple used these “manipulated” agreements to help make its case.

But what is most troubling is the extent to which it appears to have worked.

The FTC’s action against Qualcomm rested in substantial part on arguments that Qualcomm’s rates were too high (even though the FTC constructed its case without coming right out and saying this, at least until trial). In its opening statement the FTC said:

Qualcomm’s practices, including no license, no chips, skewed negotiations towards the outcomes that favor Qualcomm and lead to higher royalties. Qualcomm is committed to license its standard essential patents on fair, reasonable, and non-discriminatory terms. But even before doing market comparison, we know that the license rates charged by Qualcomm are too high and above FRAND because Qualcomm uses its chip power to require a license.

* * *

Mr. Michael Lasinski [the FTC’s patent valuation expert] compared the royalty rates received by Qualcomm to … the range of FRAND rates that ordinarily would form the boundaries of a negotiation … Mr. Lasinski’s expert opinion … is that Qualcomm’s royalty rates are far above any indicators of fair and reasonable rates. (Emphasis added).

The key question is what constitutes the “range of FRAND rates that ordinarily would form the boundaries of a negotiation”?

Because they were discussed under seal, we don’t know the precise agreements that the FTC’s expert, Mr. Lasinski, used for his analysis. But we do know something about them: His analysis entailed a study of only eight licensing agreements; in six of them, the licensee was either Apple or Samsung; and in all of them the licensor was either Interdigital, Nokia, or Ericsson. We also know that Mr. Lasinski’s valuation study did not include any Qualcomm licenses, and that the eight agreements he looked at were all executed after the district court’s decision in Microsoft vs. Motorola in 2013.

A curiously small number of agreements

Right off the bat there is a curiosity in the FTC’s valuation analysis. Even though there are hundreds of SEP license agreements involving the relevant standards, the FTC’s analysis relied on only eight, three-quarters of which involved licensing by only two companies: Apple and Samsung.

Indeed, even since 2013 (a date to which we will return) there have been scads of licenses (see, e.g., here, here, and here). Not only Apple and Samsung make CDMA and LTE devices; there are — quite literally — hundreds of other manufacturers out there, all of them licensing essentially the same technology — including global giants like LG, Huawei, HTC, Oppo, Lenovo, and Xiaomi. Why were none of their licenses included in the analysis?

At the same time, while Interdigital, Nokia, and Ericsson are among the largest holders of CDMA and LTE SEPs, several dozen companies have declared such patents, including Motorola (Alphabet), NEC, Huawei, Samsung, ZTE, NTT DOCOMO, etc. Again — why were none of their licenses included in the analysis?

All else equal, more data yields better results. This is particularly true where the data are complex license agreements which are often embedded in larger, even-more-complex commercial agreements and which incorporate widely varying patent portfolios, patent implementers, and terms.

Yet the FTC relied on just eight agreements in its comparability study, covering a tiny fraction of the industry’s licensors and licensees, and, notably, including primarily licenses taken by the two companies (Samsung and Apple) that have most aggressively litigated their way to lower royalty rates.

A curiously crabbed selection of licensors

And it is not just that the selected licensees represent a weirdly small and biased sample; it is also not necessarily even a particularly comparable sample.

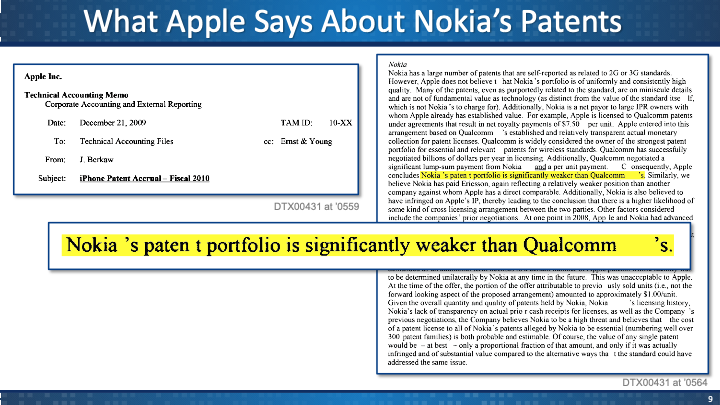

One thing we can be fairly confident of, given what we know of the agreements used, is that at least one of the license agreements involved Nokia licensing to Apple, and another involved InterDigital licensing to Apple. But these companies’ patent portfolios are not exactly comparable to Qualcomm’s. About Nokia’s patents, Apple said:

And about InterDigital’s:

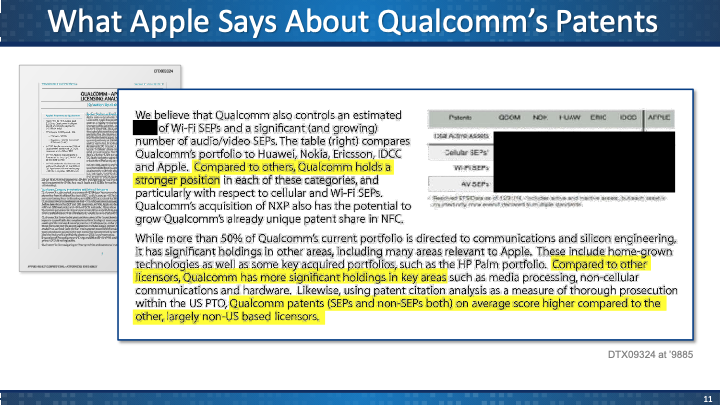

Meanwhile, Apple’s view of Qualcomm’s patent portfolio (despite its public comments to the contrary) was that it was considerably better than the others’:

The FTC’s choice of such a limited range of comparable license agreements is curious for another reason, as well: It includes no Qualcomm agreements. Qualcomm is certainly one of the biggest players in the cellular licensing space, and no doubt more than a few license agreements involve Qualcomm. While it might not make sense to include Qualcomm licenses that the FTC claims incorporate anticompetitive terms, that doesn’t describe the huge range of Qualcomm licenses with which the FTC has no quarrel. Among other things, Qualcomm licenses from before it began selling chips would not have been affected by its alleged “no license, no chips” scheme, nor would licenses granted to companies that didn’t also purchase Qualcomm chips. Furthermore, its licenses for technology reading on the WCDMA standard are not claimed to be anticompetitive by the FTC.

And yet none of these licenses were deemed “comparable” by the FTC’s expert, even though, on many dimensions — most notably, with respect to the underlying patent portfolio being valued — they would have been the most comparable (i.e., identical).

A curiously circumscribed timeframe

That the FTC’s expert should use the 2013 cut-off date is also questionable. According to Lasinski, he chose to use agreements after 2013 because it was in 2013 that the U.S. District Court for the Western District of Washington decided the Microsoft v. Motorola case. Among other things, the court in Microsoft v Motorola held that the proper value of a SEP is its “intrinsic” patent value, including its value to the standard, but not including the additional value it derives from being incorporated into a widely used standard.

According to the FTC’s expert,

prior to [Microsoft v. Motorola], people were trying to value … the standard and the license based on the value of the standard, not the value of the patents ….

Asked by Qualcomm’s counsel if his concern was that the “royalty rates derived in license agreements for cellular SEPs [before Microsoft v. Motorola] could very well have been above FRAND,” Mr. Lasinski concurred.

The problem with this approach is that it’s little better than arbitrary. The Motorola decision was an important one, to be sure, but the notion that sophisticated parties in a multi-billion dollar industry were systematically agreeing to improper terms until a single court in Washington suggested otherwise is absurd. To be sure, such agreements are negotiated in “the shadow of the law,” and judicial decisions like the one in Washington (later upheld by the Ninth Circuit) can affect the parties’ bargaining positions.

But even if it were true that the court’s decision had some effect on licensing rates, the decision would still have been only one of myriad factors determining parties’ relative bargaining power and their assessment of the proper valuation of SEPs. There is no basis to support the assertion that the Motorola decision marked a sea-change between “improper” and “proper” patent valuations. And, even if it did, it was certainly not alone in doing so, and the FTC’s expert offers no justification for determining that agreements reached before, say, the European Commission’s decision against Qualcomm in 2018 were “proper,” or that the Korea FTC’s decision against Qualcomm in 2009 didn’t have the same sort of corrective effect as the Motorola court’s decision in 2013.

At the same time, a review of a wider range of agreements suggested that Qualcomm’s licensing royalties weren’t inflated

Meanwhile, one of Qualcomm’s experts in the FTC case, former DOJ Chief Economist Aviv Nevo, looked at whether the FTC’s theory of anticompetitive harm was borne out by the data by looking at Qualcomm’s royalty rates across time periods and standards, and using a much larger set of agreements. Although his remit was different than Mr. Lasinski’s, and although he analyzed only Qualcomm licenses, his analysis still sheds light on Mr. Lasinski’s conclusions:

[S]pecifically what I looked at was the predictions from the theory to see if they’re actually borne in the data….

[O]ne of the clear predictions from the theory is that during periods of alleged market power, the theory predicts that we should see higher royalty rates.

So that’s a very clear prediction that you can take to data. You can look at the alleged market power period, you can look at the royalty rates and the agreements that were signed during that period and compare to other periods to see whether we actually see a difference in the rates.

Dr. Nevo’s analysis, which looked at royalty rates in Qualcomm’s SEP license agreements for CDMA, WCDMA, and LTE ranging from 1990 to 2017, found no differences in rates between periods when Qualcomm was alleged to have market power and when it was not alleged to have market power (or could not have market power, on the FTC’s theory, because it did not sell corresponding chips).

The reason this is relevant is that Mr. Lasinski’s assessment implies that Qualcomm’s higher royalty rates weren’t attributable to its superior patent portfolio, leaving either anticompetitive conduct or non-anticompetitive, superior bargaining ability as the explanation. No one thinks Qualcomm has cornered the market on exceptional negotiators, so really the only proffered explanation for the results of Mr. Lasinski’s analysis is anticompetitive conduct. But this assumes that his analysis is actually reliable. Prof. Nevo’s analysis offers some reason to think that it is not.

All of the agreements studied by Mr. Lasinski were drawn from the period when Qualcomm is alleged to have employed anticompetitive conduct to elevate its royalty rates above FRAND. But when the actual royalties charged by Qualcomm during its alleged exercise of market power are compared to those charged when and where it did not have market power, the evidence shows it received identical rates. Mr Lasinki’s results, then, would imply that Qualcomm’s royalties were “too high” not only while it was allegedly acting anticompetitively, but also when it was not. That simple fact suggests on its face that Mr. Lasinski’s analysis may have been flawed, and that it systematically under-valued Qualcomm’s patents.

Connecting the dots and calling into question the strength of the FTC’s case

In its closing argument, the FTC pulled together the implications of its allegations of anticompetitive conduct by pointing to Mr. Lasinski’s testimony:

Now, looking at the effect of all of this conduct, Qualcomm’s own documents show that it earned many times the licensing revenue of other major licensors, like Ericsson.

* * *

Mr. Lasinski analyzed whether this enormous difference in royalties could be explained by the relative quality and size of Qualcomm’s portfolio, but that massive disparity was not explained.

Qualcomm’s royalties are disproportionate to those of other SEP licensors and many times higher than any plausible calculation of a FRAND rate.

* * *

The overwhelming direct evidence, some of which is cited here, shows that Qualcomm’s conduct led licensees to pay higher royalties than they would have in fair negotiations.

It is possible, of course, that Lasinki’s methodology was flawed; indeed, at trial Qualcomm argued exactly this in challenging his testimony. But it is also possible that, whether his methodology was flawed or not, his underlying data was flawed.

It is impossible from the publicly available evidence to definitively draw this conclusion, but the subsequent revelation that Apple may well have manipulated at least a significant share of the eight agreements that constituted Mr. Lasinski’s data certainly increases the plausibility of this conclusion: We now know, following Qualcomm’s opening statement in Apple v. Qualcomm, that that stilted set of comparable agreements studied by the FTC’s expert also happens to be tailor-made to be dominated by agreements that Apple may have manipulated to reflect lower-than-FRAND rates.

What is most concerning is that the FTC may have built up its case on such questionable evidence, either by intentionally cherry picking the evidence upon which it relied, or inadvertently because it rested on such a needlessly limited range of data, some of which may have been tainted.

Intentionally or not, the FTC appears to have performed its valuation analysis using a needlessly circumscribed range of comparable agreements and justified its decision to do so using questionable assumptions. This seriously calls into question the strength of the FTC’s case.