The Asamblea Legislativa de la República de Costa Rica (Costa Rica’s legislature) moved in 2020 to empower the Banco Central de Costa Rica (BCCR), the nation’s central bank, to impose price controls on fees charged by both payment-card issuers and acquirers.

I have written previously about the perverse effects these price controls can generate (here, here, and here), and was thus intrigued to see that the International Monetary Fund (IMF) included a related assessment of payment-card fees as part of a background paper on the Costa Rican economy.

In this post, I review the implementation of price controls on the merchant-discount rate (MDR) and interchange fees in Costa Rica, as well as their likely effects. I then review the IMF’s analysis and offer some constructive criticism.

BCCR’s MDR and Interchange-Fee Caps

Legislative Decree No. 9831 authorized the BCCR to regulate fees charged for “the processing of transactions that use payment devices and the operation of the card system.” The law’s stated objective was “to promote its efficiency and security, and guarantee the lowest possible cost for affiliates.” The BCCR was tasked with issuing regulations that would ensure the rule is “in the public interest” and that it guarantee that fees charged to “affiliates” (i.e., merchants) are “the lowest possible … following international best practices.”

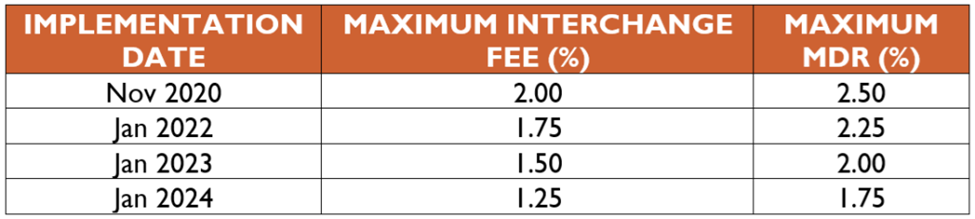

Starting in late November 2020, the BCCR set maximum interchange fees for domestic cards at 2.0% and maximum MDR at 2.5%. Over a four-year period, the BCCR has gradually ratcheted down both MDR and interchange-fee caps, as shown in Table 1.

TABLE 1: Interchange Fee and MDR Caps in Costa Rica, 2020-2024

The simultaneous caps on MDR and interchange fees limit revenue to both acquiring banks and issuing banks. This has likely reduced banks’ investments in improvements to the payment system, resulting in lower levels of system efficiency and speed, and possibly increased fraud, than would otherwise have been the case.

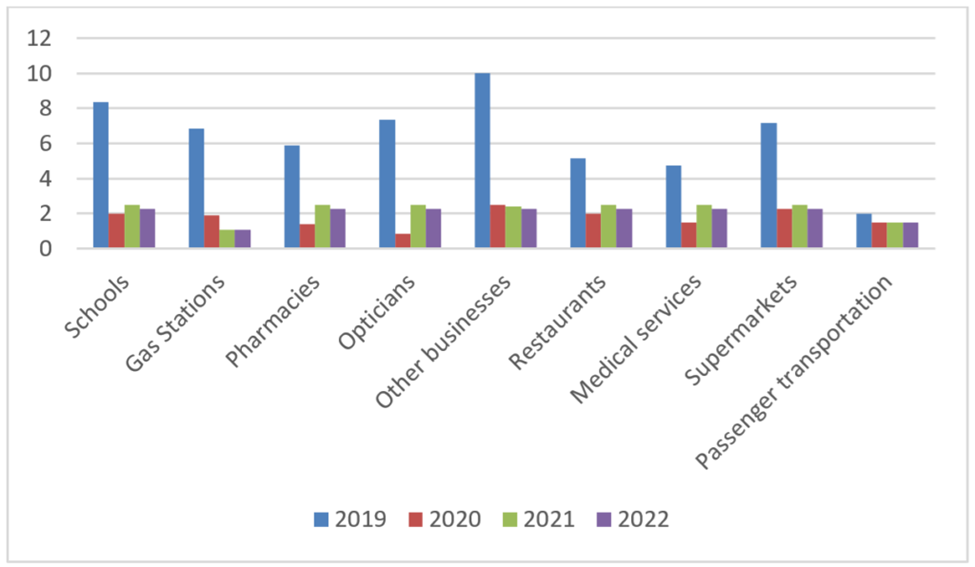

The caps may also have made it unprofitable for banks to service some merchants. Prior to the caps, the median MDR varied considerably by merchant type. One explanation for this is that riskier merchants were effectively charged a risk premium in the form of higher MDRs, because of the greater likelihood that they or their customers would engage in fraud and thereby impose liability on the acquirer and/or issuer. (This is hardly unique to Costa Rica – it is simply good risk management by acquirers.) After the caps, the median MDRs became much more closely bunched (see Figure 1).

If the previously larger differentials were a result of acquirers charging a risk premium, then in BCCR’s attempt to reduce merchant costs, it may inadvertently (but predictably) have prohibited some merchants from being able to accept payment cards. This is neither efficient, nor is it in the public interest.

FIGURE 1: Median MDR for Various Merchants in Costa Rica, 2019-2022 (%)

SOURCE: Author’s calculations based on BCCR data

An alternative hypothesis is that these high MDRs reflect a lack of competition among acquiring banks. In that case, the appropriate response would have been to seek to understand the root cause and remedy that directly. For example, if the lack of competition arose from regulations imposed by BCCR, it would be incumbent on BCCR to modify its regulations to reduce barriers to competition. In that case, capping the MDR would not address the underlying problem; indeed, it likely makes it worse, by inhibiting acquirers from being able to differentiate themselves on price or quality.

The IMF’s Analysis

Given the potential harms that price controls might do to Costa Rica’s economy, it is perhaps not surprising that the IMF should have taken an interest in the subject. But strangely, rather than review the price controls’ broader impact and warning against those potential harms, the IMF instead focused narrowly on the methodology BCCR used to set the price controls.

The IMF analysis begins with a highly simplified description of four-party card payments. It then outlines Legislative Decree 9831 and notes that the highest MDR prior to the decree’s implementation was 12%, which it said reflected:

…in part a highly concentrated payment system in Costa Rica. For example, the top 3 companies accounted for 71 percent of the credit card transactions.

Meanwhile:

After the BCCR imposed maximum card payment fees following the implementation of the decree, the number of service providers and customers have both increased.

This is an interesting observation. One would think the IMF might have elaborated a bit more, because prima facie, it defies economic logic. Price controls tend to reduce supply. A cap on MDRs would reduce the profitability of acquiring, making it less attractive to enter and compete in the market for card acquisition. So, how exactly did the BCCR’s price caps have the opposite effect? The IMF does not attempt to offer an explanation.

Perhaps the IMF is confusing correlation with causation. The past few years have seen an explosion in fintech firms globally, including many offering acquiring and related services (e.g., gateways and combined gateway-acquirers such as Stripe). These fintechs tend to have lower costs, which is what allows them to challenge incumbents. A more logical conclusion would be that competition has increased despite the price controls.

Regression Analysis of BCCR Price Caps

After its naive and tendentious analysis of the competitive landscape for payments in Costa Rica, the IMF goes on to describe the process by which the BCCR set its price controls on MDR and interchange fees, using international comparisons. Here, the IMF enters the world of bathos, combining a sublime misunderstanding of the role of MDRs and interchange fees with a delusional view of the regulator’s role in setting prices.

The IMF initially offers its own international price comparison in the form of a multivariate-regression analysis, from which it infers price caps for Costa Rica’s issuers and acquirers:

Based on the regression analysis using the international data, the corresponding interchange fee for Costa Rica is estimated as 1.06 with a 95 percent confidence interval equal to [0.91, 1.20], compared to the BCCR’s point estimate of 1.25. The estimated MDR, at 1.94, is almost the same as the results obtained by BCCR at 1.91.

Nowhere does it explain why such a regression should be used to set such caps or, indeed, why such caps would generate economic benefits. That’s because it can’t. There is simply no logical basis for using a regression analysis to set MDRs, interchange fees, or any related price controls.

It is, however, noteworthy that the variable in the IMF’s regression that has the largest and most statistically significant coefficient for both interchange and MDR is “regulation.” This should not be surprising, as many governments around the world have used their monopoly power to regulate—i.e., to impose price controls on—payment-card fees.

The IMF goes on to state that “in many countries, a cost-based methodology is often used to determine the maximum commissions.” It continues:

Rather than being based on international comparisons, a cost-based methodology takes into account the specific market structure in the country by reflecting certain costs incurred by the providers of the acquiring and issuing service…

This is true as far as it goes. Unfortunately, the IMF leaves unstated that such cost-based methodologies are little better than international comparisons as a basis for setting price caps on payment-card fees. The fundamental problem with both is that interchange fees (and, hence, MDRs) cannot be determined objectively, because a core purpose of such fees is to balance two-sided markets (merchants on one side, consumers on the other). This means that they are always contingent and tentative.

In markets that are not subject to price controls, network operators set interchange fees in such a way as to maximize the value for all participants. This is a discovery process, wherein prices for different cards and different merchants are adjusted to account for changes in demand, fraud rates, and other factors. Meanwhile, acquirers set MDRs to accommodate the range of interchange fees and merchant-specific facts.

It is beguiling, then, that the IMF deigns to offer the following “advice” to Costa Rica:

Going forward, the BCCR should consider complementing the cross-country analysis with a cost-based methodology that can capture the characteristics of Costa Rica’s own payment system in determining the maximum commission fees.

The Distortionary Role of Bank Regulation

One possible cause of a lack of competition is state ownership of banks and distortionary regulation. The fact that the “digital payment” variable in the IMF’s international regression is strongly negatively correlated with interchange fees may be an indication that markets more open to digital payments are more competitive.

A 2022 technical note by the World Bank noted that: “Various distortions and regulatory asymmetries make the playing field uneven between public and private banks in Costa Rica,” which has the effect of impeding competition and undermining innovation.

When governments compete directly with the private sector—while subjecting private companies to opaque and distortionary licensing systems—few private companies will have the stomach or the funds to stand in line and wait their turn. By contrast, when governments stay out of the market and operate open, transparent, impartial, and efficient licensing systems governed by simple rules, market participants will champ at the bit to compete.

In its main report, the World Bank offered a rather more insightful assessment of how to address these competitive distortions than did the IMF:

Costa Rica’s state-led economic development model of the past created a sizeable state footprint in the financial sector, but also over many years competitive distortions and inefficiencies. To enhance financial intermediation efficiency and development it is recommended to:

- Level the playing field in financial services provision –irrespective of ownership. …

- Remov[e] competitive advantages enjoyed by Banco Popular …

- Transform SBD [a state-owned bank] into a regulated second-tier development finance institution. …

Conclusion

Given these concrete, practical observations published a year previously by its sister organization at 1850 I Street, it’s not clear why the IMF decided to focus on the issue of MDRs and interchange fees as part of its Article IV Review of Costa Rica. No explanation is given. But the analysis is, at once, both superficial and supercilious.

It is superficial because it fails to grasp even the most basic elements of how payment systems work, the role of two-sided markets, and the inherent variation in risks associated with different merchants and consumers.

It is supercilious because it purports to offer a deterministic mechanism by which to set MDRs and interchange fees—based either on comparisons of those prices set in other jurisdictions (many effectively themselves set by political mandates) or on some arbitrary set of cost metrics, or both.