[TOTM: The following is the third in a series of posts by TOTM guests and authors on the politicization of antitrust. The entire series of posts is available here.]

This post is authored by Geoffrey A. Manne, president and founder of the International Center for Law & Economics, and Alec Stapp, Research Fellow at the International Center for Law & Economics.

Source: The Economist

Is there a relationship between concentrated economic power and political power? Do big firms have success influencing politicians and regulators to a degree that smaller firms — or even coalitions of small firms — could only dream of? That seems to be the narrative that some activists, journalists, and scholars are pushing of late. And, to be fair, it makes some intuitive sense (before you look at the data). The biggest firms have the most resources — how could they not have an advantage in the political arena?

The argument that corporate power leads to political power faces at least four significant challenges, however. First, the little empirical research there is does not support the claim. Second, there is almost no relationship between market capitalization (a proxy for economic power) and lobbying expenditures (a, admittedly weak, proxy for political power). Third, the absolute level of spending on lobbying is surprisingly low in the US given the potential benefits from rent-seeking (this is known as the Tullock paradox). Lastly, the proposed remedy for this supposed problem is to make antitrust more political — an intervention that is likely to make the problem worse rather than better (assuming there is a problem to begin with).

The claims that political power follows economic power

The claim that large firms or industry concentration causes political power (and thus that under-enforcement of antitrust laws is a key threat to our democratic system of government) is often repeated, and accepted as a matter of faith. Take, for example, Robert Reich’s March 2019 Senate testimony on “Does America Have a Monopoly Problem?”:

These massive corporations also possess substantial political clout. That’s one reason they’re consolidating: They don’t just seek economic power; they also seek political power.

Antitrust laws were supposed to stop what’s been going on.

* * *

[S]uch large size and gigantic capitalization translate into political power. They allow vast sums to be spent on lobbying, political campaigns, and public persuasion. (emphasis added)

Similarly, in an article in August of 2019 for The Guardian, law professor Ganesh Sitaraman argued there is a tight relationship between economic power and political power:

[R]eformers recognized that concentrated economic power — in any form — was a threat to freedom and democracy. Concentrated economic power not only allowed for localized oppression, especially of workers in their daily lives, it also made it more likely that big corporations and wealthy people wouldn’t be subject to the rule of law or democratic controls. Reformers’ answer to the concentration of economic power was threefold: break up economic power, rein it in through regulation, and tax it.

It was the reformers of the Gilded Age and Progressive Era who invented America’s antitrust laws — from the Sherman Antitrust Act of 1890 to the Clayton Act and Federal Trade Commission Acts of the early 20th century. Whether it was Republican trust-buster Teddy Roosevelt or liberal supreme court justice Louis Brandeis, courageous leaders in this era understood that when companies grow too powerful they threatened not just the economy but democratic government as well. Break-ups were a way to prevent the agglomeration of economic power in the first place, and promote an economic democracy, not just a political democracy. (emphasis added)

Luigi Zingales made a similar argument in his 2017 paper “Towards a Political Theory of the Firm”:

[T]he interaction of concentrated corporate power and politics is a threat to the functioning of the free market economy and to the economic prosperity it can generate, and a threat to democracy as well. (emphasis added)

The assumption that economic power leads to political power is not a new one. Not only, as Zingales points out, have political thinkers since Adam Smith asserted versions of the same, but more modern social scientists have continued the claims with varying (but always indeterminate) degrees of quantification. Zingales quotes Adolf Berle and Gardiner Means’ 1932 book, The Modern Corporation and Private Property, for example:

The rise of the modern corporation has brought a concentration of economic power which can compete on equal terms with the modern state — economic power versus political power, each strong in its own field.

Russell Pittman (an economist at the DOJ Antitrust Division) argued in 1988 that rent-seeking activities would be undertaken only by firms in highly concentrated industries because:

if the industry in question is unconcentrated, then the firm may decide that the level of benefits accruing to the industry will be unaffected by its own level of contributions, so that the benefits may be enjoyed without incurrence of the costs. Such a calculation may be made by other firms in the industry, of course, with the result that a free-rider problem prevents firms individually from making political contributions, even if it is in their collective interest to do so.

For the most part the claims are virtually entirely theoretical and their support anecdotal. Reich, for example, supports his claim with two thin anecdotes from which he draws a firm (but, in fact, unsupported) conclusion:

To take one example, although the European Union filed fined [sic] Google a record $2.7 billion for forcing search engine users into its own shopping platforms, American antitrust authorities have not moved against the company.

Why not?… We can’t be sure why the FTC chose not to pursue Google. After all, section 5 of the Federal Trade Commission Act of 1914 gives the Commission broad authority to prevent unfair acts or practices. One distinct possibility concerns Google’s political power. It has one of the biggest lobbying powerhouses in Washington, and the firm gives generously to Democrats as well as Republicans.

A clearer example of an abuse of power was revealed last November when the New York Times reported that Facebook executives withheld evidence of Russian activity on their platform far longer than previously disclosed.

Even more disturbing, Facebook employed a political opposition research firm to discredit critics. How long will it be before Facebook uses its own data and platform against critics? Or before potential critics are silenced even by the possibility? As the Times’s investigation made clear, economic power cannot be separated from political power. (emphasis added)

The conclusion — that “economic power cannot be separated from political power” — simply does not follow from the alleged evidence.

The relationship between economic power and political power is extremely weak

Few of these assertions of the relationship between economic and political power are backed by empirical evidence. Pittman’s 1988 paper is empirical (as is his previous 1977 paper looking at the relationship between industry concentration and contributions to Nixon’s re-election campaign), but it is also in direct contradiction to several other empirical studies (Zardkoohi (1985); Munger (1988); Esty and Caves (1983)) that find no correlation between concentration and political influence; Pittman’s 1988 paper is indeed a response to those papers, in part.

In fact, as one study (Grier, Muger & Roberts (1991)) summarizes the evidence:

[O]f ten empirical investigations by six different authors/teams…, relatively few of the studies find a positive, significant relation between contributions/level of political activity and concentration, though a variety of measures of both are used….

There is little to recommend most of these studies as conclusive one way or the other on the question of interest. Each one suffers from a sample selection or estimation problem that renders its results suspect. (emphasis added)

And, as they point out, there is good reason to question the underlying theory of a direct correlation between concentration and political influence:

[L]egislation or regulation favorable to an industry is from the perspective of a given firm a public good, and therefore subject to Olson’s collective action problem. Concentrated industries should suffer less from this difficulty, since their sparse numbers make bargaining cheaper…. [But at the same time,] concentration itself may affect demand, suggesting that the predicted correlation between concentration and political activity may be ambiguous, or even negative.

* * *

The only conclusion that seems possible is that the question of the correct relation between the structure of an industry and its observed level of political activity cannot be resolved theoretically. While it may be true that firms in a concentrated industry can more cheaply solve the collective action problem that inheres in political action, they are also less likely to need to do so than their more competitive brethren…. As is so often the case, the interesting question is empirical: who is right? (emphasis added)

The results of Grier, Muger & Roberts (1991)’s own empirical study are ambiguous at best (and relate only to political participation, not success, and thus not actual political power):

[A]re concentrated industries more or less likely to be politically active? Numerous previous studies have addressed this topic, but their methods are not comparable and their results are flatly contradictory.

On the side of predicting a positive correlation between concentration and political activity is the theory that Olson’s “free rider” problem has more bite the larger the number of participants and the smaller their respective individual benefits. Opposing this view is the claim that it precisely because such industries are concentrated that they have less need for government intervention. They can act on their own to gamer the benefits of cartelization that less concentrated industries can secure only through political activity.

Our results indicate that both sides are right, over some range of concentration. The relation between political activity and concentration is a polynomial of degree 2, rising and then falling, achieving a peak at a four-firm concentration ratio slightly below 0.5. (emphasis added)

Despite all of this, Zingales (like others) explicitly claims that there is a clear and direct relationship between economic power and political power:

In the last three decades in the United States, the power of corporations to shape the rules of the game has become stronger… [because] the size and market share of companies has increased, which reduces the competition across conflicting interests in the same sector and makes corporations more powerful vis-à-vis consumers’ interest.

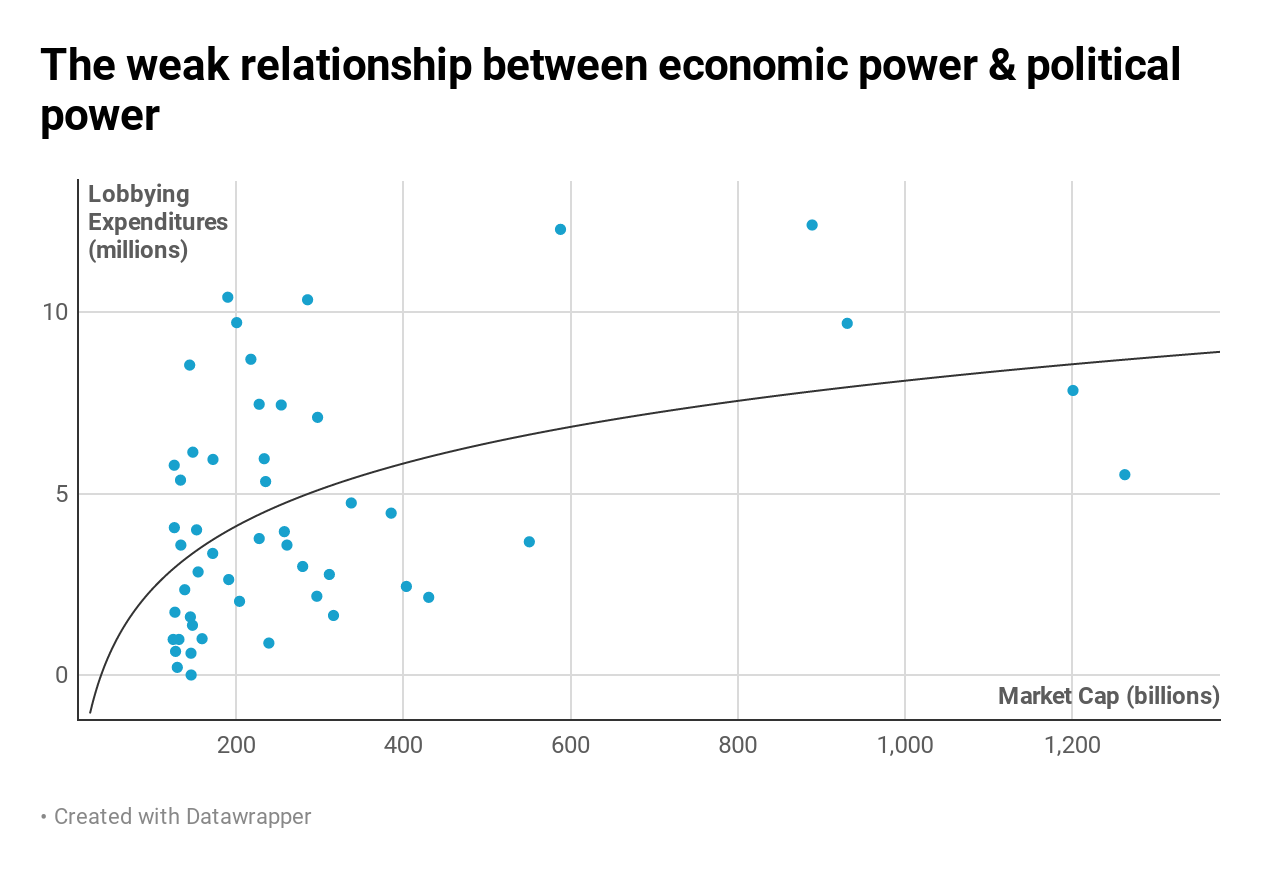

But a quick look at the empirical data continues to call this assertion into serious question. Indeed, if we look at the lobbying expenditures of the top 50 companies in the US by market capitalization, we see an extremely weak (at best) relationship between firm size and political power (as proxied by lobbying expenditures):

Of course, once again, this says little about the effectiveness of efforts to exercise political power, which could, in theory, correlate with market power but not expenditures. Yet the evidence on this suggests that, while concentration “increases both [political] activity and success…, [n]either firm size nor industry size has a robust influence on political activity or success.” (emphasis added). Of course there are enormous and well-known problems with measuring industry concentration, and it’s not clear that even this attribute is well-correlated with political activity or success (and, interestingly for the argument that profits are a big part of the story because firms in more concentrated industries from lax antitrust realize higher profits have more money to spend on political influence, even concentration in the Esty and Caves study is not correlated with political expenditures.)

Indeed, a couple of examples show the wide range of lobbying expenditures for a given firm size. Costco, which currently has a market cap of $130 billion, has spent only $210,000 on lobbying so far in 2019. By contrast, Amgen, which has a $144 billion market cap, has spent $8.54 million, or more than 40 times as much. As shown in the chart above, this variance is the norm.

However, discussing the relative differences between these companies is less important than pointing out the absolute levels of expenditure. Spending eight and a half million dollars per year would not be prohibitive for literally thousands of firms in the US. If access is this cheap, what’s going on here?

Why is there so little money in US politics?

The Tullock paradox asks why, if the return to rent-seeking is so high — which it plausibly is because the government spends trillions of dollars each year — is so little money spent on influencing policymakers?

Considering the value of public policies at stake and the reputed influence of campaign contributors in policymaking, Gordon Tullock (1972) asked, why is there so little money in U.S. politics? In 1972, when Tullock raised this question, campaign spending was about $200 million. Assuming a reasonable rate of return, such an investment could have yielded at most $250-300 million over time, a sum dwarfed by the hundreds of billions of dollars worth of public expenditures and regulatory costs supposedly at stake.

A recent article by Scott Alexander updated the numbers for 2019 and compared the total to the $12 billion US almond industry:

[A]ll donations to all candidates, all lobbying, all think tanks, all advocacy organizations, the Washington Post, Vox, Mic, Mashable, Gawker, and Tumblr, combined, are still worth a little bit less than the almond industry.

Maybe it’s because spending money on donations, lobbying, think tanks, journalism and advocacy is ineffective on net (i.e., spending by one group is counterbalanced by spending by another group) and businesses know it?

In his paper on elections, Ansolabehere focuses on the corporate perspective. He argues that money neither makes a candidate much more likely to win, nor buys much influence with a candidate who does win. Corporations know this, which is why they don’t bother spending more. (emphasis added)

To his credit, Zingales acknowledges this issue:

To the extent that US corporations are exercising political influence, it seems that they are choosing less-visible but perhaps more effective ways. In fact, since Gordon Tullock’s (1972) famous article, it has been a puzzle in political science why there is so little money in politics (as discussed in this journal by Ansolabehere, de Figueiredo, and Snyder 2003).

So, what are these “less-visible but perhaps more effective” ways? Unfortunately, the evidence in support of this claim is anecdotal and unconvincing. As noted above, Reich offers only speculation and extremely weak anecdotal assertions. Meanwhile, Zingales tells the story of Robert (mistakenly identified in the paper as “Richard”) Rubin pushing through repeal of Glass-Steagall to benefit Citigroup, then getting hired for $15 million a year when he left the government. Assuming the implication is actually true, is that amount really beyond the reach of all but the largest companies? How many banks with an interest in the repeal of Glass-Steagall were really unlikely at the time to be able to credibly offer future compensation because they would be out of business? Very few, and no doubt some of the biggest and most powerful were arguably at greater risk of bankruptcy than some of the smaller banks.

Maybe only big companies have an interest in doing this kind of thing because they have more to lose? But in concentrated industries they also have more to lose by conferring the benefit on their competitors. And it’s hard to make the repeal or passage of a law, say, apply only to you and not everyone else in the industry. Maybe they collude? Perhaps, but is there any evidence of this? Zingales offers only pure speculation here, as well. For example, why was the US Google investigation dropped but not the EU one? Clearly because of White House visits, says Zingales. OK — but how much do these visits cost firms? If that’s the source of political power, it surely doesn’t require monopoly profits to obtain it. And it’s virtually impossible that direct relationships of this kind are beyond the reach of coalitions of smaller firms, or even small firms, full stop.

In any case, the political power explanation turns mostly on doling out favors in exchange for individuals’ payoffs — which just aren’t that expensive, and it’s doubtful that the size of a firm correlates with the quality of its one-on-one influence brokering, except to the extent that causation might run the other way — which would be an indictment not of size but of politics. Of course, in the Hobbesian world of political influence brokering, as in the Hobbesian world of pre-political society, size alone is not determinative so long as alliances can be made or outcomes turn on things other than size (e.g., weapons in the pre-Hobbesian world; family connections in the world of political influence).

The Noerr–Pennington doctrine is highly relevant here as well. In Noerr, the Court ruled that “no violation of the [Sherman] Act can be predicated upon mere attempts to influence the passage or enforcement of laws” and “[j]oint efforts to influence public officials do not violate the antitrust laws even though intended to eliminate competition.” This would seem to explain, among other things, the existence of trade associations and other entities used by coalitions of small (and large) firms to influence the policymaking process.

If what matters for influence peddling is ultimately individual relationships and lobbying power, why aren’t the biggest firms in the world the lobbying firms and consultant shops? Why is Rubin selling out for $15 million a year if the benefit to Citigroup is in the billions? And, if concentration is the culprit, why isn’t it plausibly also the solution? It isn’t only the state that keeps the power of big companies in check; it’s other big companies, too. What Henry G. Manne said in his testimony on the Industrial Reorganization Act of 1973 remains true today:

There is simply no correlation between the concentration ratio in an industry, or the size of its firms, and the effectiveness of the industry in the halls of Government.

In addition to the data presented earlier, this analysis would be incomplete if it did not mention the role of advocacy groups in influencing outcomes, the importance and size of large foundations, the role of unions, and the role of individual relationships.

Maybe voters matter more than money?

The National Rifle Association spends very little on direct lobbying efforts (less than $10 million over the most recent two-year cycle). The organization’s total annual budget is around $400 million. In the grand scheme of things, these are not overwhelming resources. But the NRA is widely-regarded as one of the most powerful political groups in the country, particularly within the Republican Party. How could this be? In short, maybe it’s not Sturm Ruger, Remington Outdoor, and Smith & Wesson — the three largest gun manufacturers in the US — that influence gun regulations; maybe it’s the highly-motivated voters who like to buy guns.

The NRA has 5.5 million members, many of whom vote in primaries with gun rights as one of their top issues — if not the top issue. And with low turnout in primaries — only 8.7% of all registered voters participated in 2018 Republican primaries — a candidate seeking the Republican nomination all but has to secure an endorsement from the NRA. On this issue at least, the deciding factor is the intensity of voter preferences, not the magnitude of campaign donations from rent-seeking corporations.

The NRA is not the only counterexample to arguments like those from Zingales. Auto dealers are a constituency that is powerful not necessarily due to its raw size but through its dispersed nature. At the state level, almost every political district has an auto dealership (and the owners are some of the wealthiest and best-connected individuals in the area). It’s no surprise then that most states ban the direct sale of cars from manufacturers (i.e., you have to go through a dealer). This results in higher prices for consumers and lower output for manufacturers. But the auto dealership industry is not highly concentrated at the national level. The dealers don’t need to spend millions of dollars lobbying federal policymakers for special protections; they can do it on the local level — on a state-by-state basis — for much less money (and without merging into consolidated national chains).

Another, more recent, case highlights the factors besides money that may affect political decisions. President Trump has been highly critical of Jeff Bezos and the Washington Post (which Bezos owns) since the beginning of his administration because he views the newspaper as a political enemy. In October, Microsoft beat out Amazon for a $10 billion contract to provide cloud infrastructure for the Department of Defense (DoD). Now, Amazon is suing the government, claiming that Trump improperly influenced the competitive bidding process and cost the company a fair shot at the contract. This case is a good example of how money may not be determinative at the margin, and also how multiple “monopolies” may have conflicting incentives and we don’t know how they net out.

Politicizing antitrust will only make this problem worse

At the FTC’s “Hearings on Competition and Consumer Protection in the 21st Century,” Barry Lynn of the Open Markets Institute advocated using antitrust to counter the political power of economically powerful firms:

[T]he main practical goal of antimonopoly is to extend checks and balances into the political economy. The foremost goal is not and must never be efficiency. Markets are made, they do not exist in any platonic ether. The making of markets is a political and moral act.

In other words, the goal of breaking up economic power is not to increase economic benefits but to decrease political influence.

But as the author of one of the empirical analyses of the relationship between economic and political power notes the asserted “solution” to the unsupported “problem” of excess political influence by economically powerful firms — more and easier antitrust enforcement — may actually make the alleged problem worse:

Economic rents may be obtained through the process of market competition or be obtained by resorting to governmental protection. Rational firms choose the least costly alternative. Collusion to obtain governmental protection will be less costly, the higher the concentration, ceteris paribus. However, high concentration in itself is neither necessary nor sufficient to induce governmental protection.

The result that rent-seeking activity is triggered when firms are affected by government regulation has a clear implication: to reduce rent-seeking waste, governmental interference in the market place needs to be attenuated. Pittman’s suggested approach, however, is “to maintain a vigorous antitrust policy” (p. 181). In fact, a more strict antitrust policy may exacerbate rent-seeking. For example, the firms which will be affected by a vigorous application of antitrust laws would have incentive to seek moderation (or rents) from Congress or from the enforcement officials.

Rent-seeking by smaller firms could both be more prevalent, and, paradoxically, ultimately lead to increased concentration. And imbuing antitrust with an ill-defined set of vague political objectives (as many proponents of these arguments desire), would also make antitrust into a sort of “meta-legislation.” As a result, the return on influencing a handful of government appointments with authority over antitrust becomes huge — increasing the ability and the incentive to do so.

And if the underlying basis for antitrust enforcement is extended beyond economic welfare effects, how long can we expect to resist calls to restrain enforcement precisely to further those goals? With an expanded basis for increased enforcement, the effort and ability to get exemptions will be massively increased as the persuasiveness of the claimed justifications for those exemptions, which already encompass non-economic goals, will be greatly enhanced. We might find that we end up with even more concentration because the exceptions could subsume the rules. All of which of course highlights the fundamental, underlying irony of claims that we need to diminish the economic content of antitrust in order to reduce the political power of private firms: If you make antitrust more political, you’ll get less democratic, more politically determined, results.