Wall Street Journal commentator, Greg Ip, reviews Thomas Philippon’s forthcoming book, The Great Reversal: How America Gave Up On Free Markets. Ip describes a “growing mountain” of research on industry concentration in the U.S. and reports that Philippon concludes competition has declined over time, harming U.S. consumers.

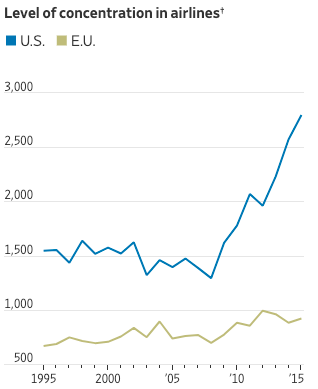

In one example, Philippon points to air travel. He notes that concentration in the U.S. has increased rapidly—spiking since the Great Recession—while concentration in the EU has increased modestly. At the same time, Ip reports “U.S. airlines are now far more profitable than their European counterparts.” (Although it’s debatable whether a five percentage point difference in net profit margin is “far more profitable”).

On first impression, the figures fit nicely with the populist antitrust narrative: As concentration in the U.S. grew, so did profit margins. Closer inspection raises some questions, however.

For example, the U.S. airline industry had a negative net profit margin in each of the years prior to the spike in concentration. While negative profits may be good for consumers, it would be a stretch to argue that long-run losses are good for competition as a whole. At some point one or more of the money losing firms is going to pull the ripcord. Which raises the issue of causation.

Just looking at the figures from the WSJ article, one could argue that rather than concentration driving profit margins, instead profit margins are driving concentration. Indeed, textbook IO economics would indicate that in the face of losses, firms will exit until economic profit equals zero. Paraphrasing Alfred Marshall, “Which blade of the scissors is doing the cutting?”

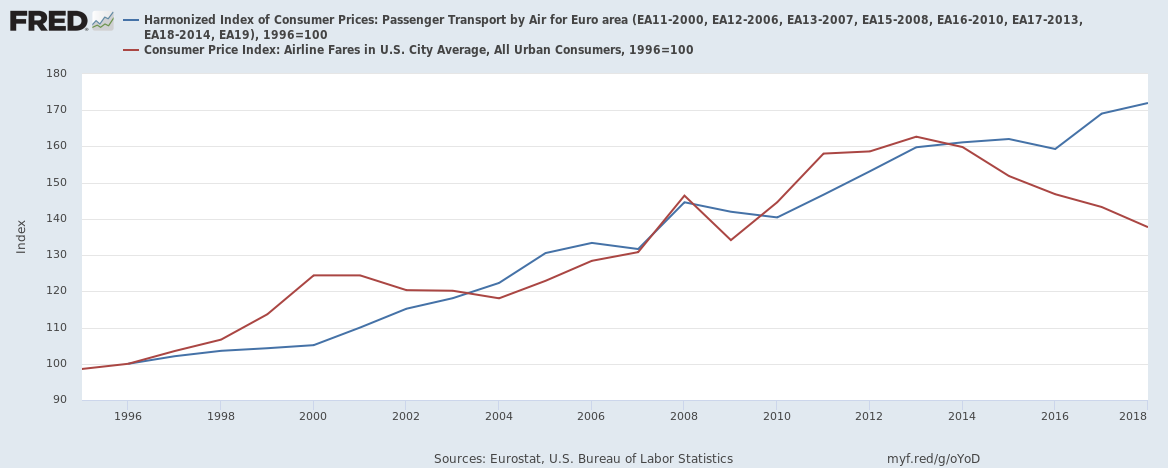

While the concentration and profits story fits the antitrust populist narrative, other observations run contrary to Philippon’s conclusion. For example, airline prices, as measured by price indexes, show that changes in U.S. and EU airline prices have fairly closely tracked each other until 2014, when U.S. prices began dropping. Sure, airlines have instituted baggage fees, but the CPI includes taxes, fuel surcharges, airport, security, and baggage fees. It’s not obvious that U.S. consumers are worse off in the so-called era of rising concentration.

Regressing U.S. air fare price index against Philippon’s concentration information in the figure above (and controlling for general inflation) finds that if U.S. concentration in 2015 was the same as in 1995, U.S. airfares would be about 2.8% lower. That a 1,250 point increase in HHI would be associated with a 2.8% increase in prices indicates that the increased concentration in U.S. airlines has led to no significant increase in consumer prices.

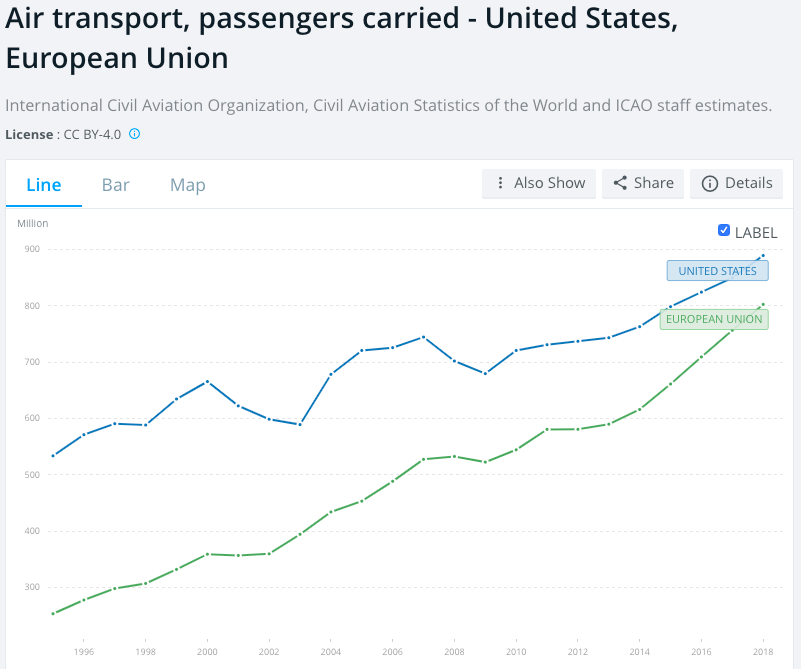

Also, if consumers are truly worse off, one would expect to see a drop off or slow down in the use of air travel. An eyeballing of passenger data does not fit the populist narrative. Instead, we see airlines are carrying more passengers and consumers are paying lower prices on average.

{kind=link}

While it’s true that low-cost airlines have shaken up air travel in the EU, the differences are not solely explained by differences in market concentration. For example, U.S. regulations prohibit foreign airlines from operating domestic flights while EU carriers compete against operators from other parts of Europe. While the WSJ’s figures tell an interesting story of concentration, prices, and profits, they do not provide a compelling case of anticompetitive conduct.