Thomas Wollmann has a new paper — “Stealth Consolidation: Evidence from an Amendment to the Hart-Scott-Rodino Act” — in American Economic Review: Insights this month. Greg Ip included this research in an article for the WSJ in which he claims that “competition has declined and corporate concentration risen through acquisitions often too small to draw the scrutiny of antitrust watchdogs.” In other words, “stealth consolidation”.

Wollmann’s study uses a difference-in-differences approach to examine the effect on merger activity of the 2001 amendment to the Hart-Scott-Rodino (HSR) Antitrust Improvements Act of 1976 (15 U.S.C. 18a). The amendment abruptly increased the pre-merger notification threshold from $15 million to $50 million in deal size. Strictly on those terms, the paper shows that raising the pre-merger notification threshold increased merger activity.

However, claims about “stealth consolidation” are controversial because they connote nefarious intentions and anticompetitive effects. As Wollmann admits in the paper, due to data limitations, he is unable to show that the new mergers are in fact anticompetitive or that the social costs of these mergers exceed the social benefits. Therefore, more research is needed to determine the optimal threshold for pre-merger notification rules, and claiming that harmful “stealth consolidation” is occurring is currently unwarranted.

Background: The “Unscrambling the Egg” Problem

In general, it is more difficult to unwind a consummated anticompetitive merger than it is to block a prospective anticompetitive merger. As Wollmann notes, for example, “El Paso Natural Gas Co. acquired its only potential rival in a market” and “the government’s challenge lasted 17 years and involved seven trips to the Supreme Court.”

Rolling back an anticompetitive merger is so difficult that it came to be known as “unscrambling the egg.” As William J. Baer, a former director of the Bureau of Competition at the FTC, described it, “there were strong incentives for speedily and surreptitiously consummating suspect mergers and then protracting the ensuing litigation” prior to the implementation of a pre-merger notification rule. These so-called “midnight mergers” were intended to avoid drawing antitrust scrutiny.

In response to this problem, Congress passed the Hart–Scott–Rodino Antitrust Improvements Act of 1976, which required companies to notify antitrust authorities of impending mergers if they exceeded certain size thresholds.

2001 Hart–Scott–Rodino Amendment

In 2001, Congress amended the HSR Act and effectively raised the threshold for premerger notification from $15 million in acquired firm assets to $50 million. This sudden and dramatic change created an opportunity to use a difference-in-differences technique to study the relationship between filing an HSR notification and merger activity.

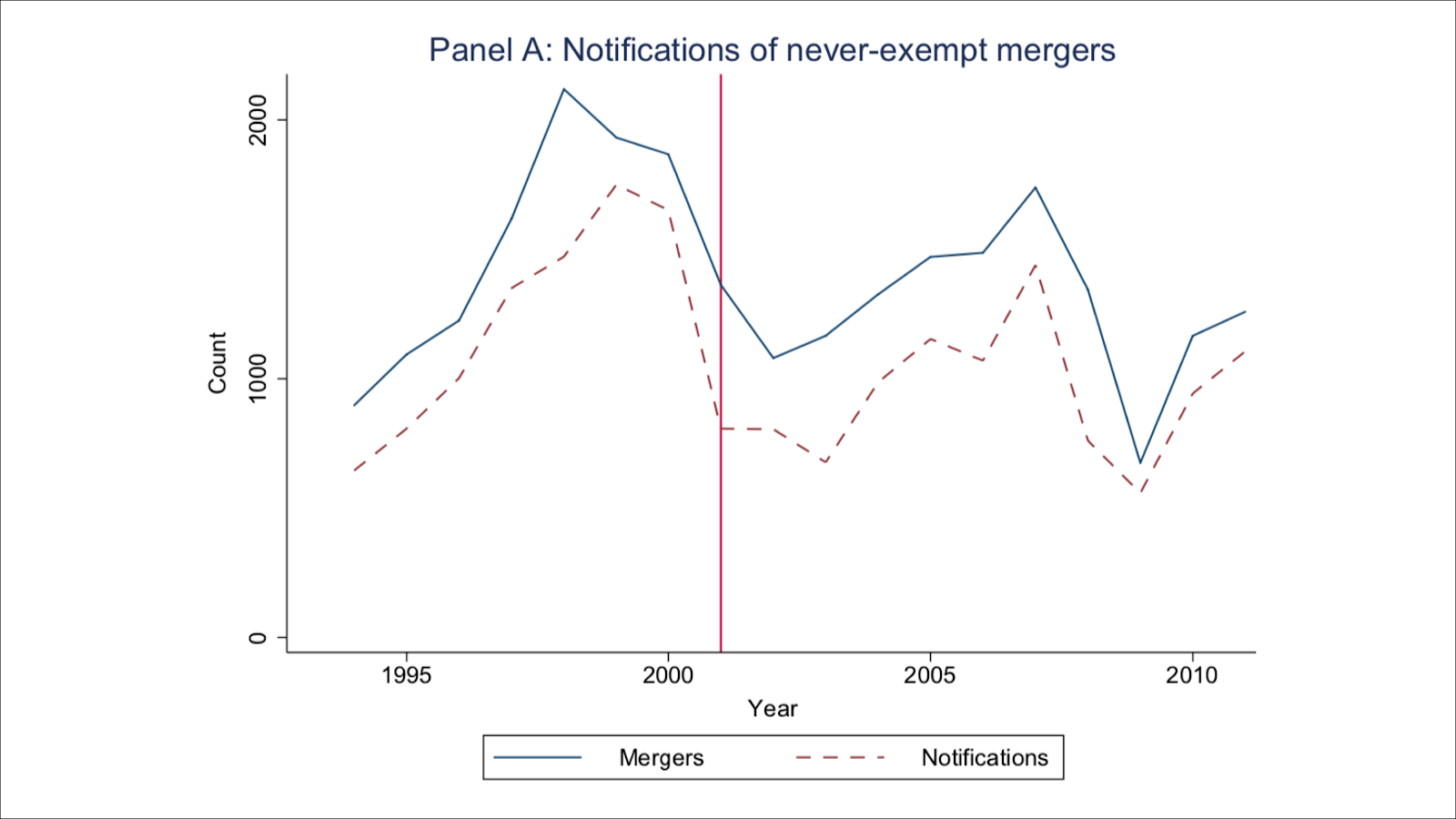

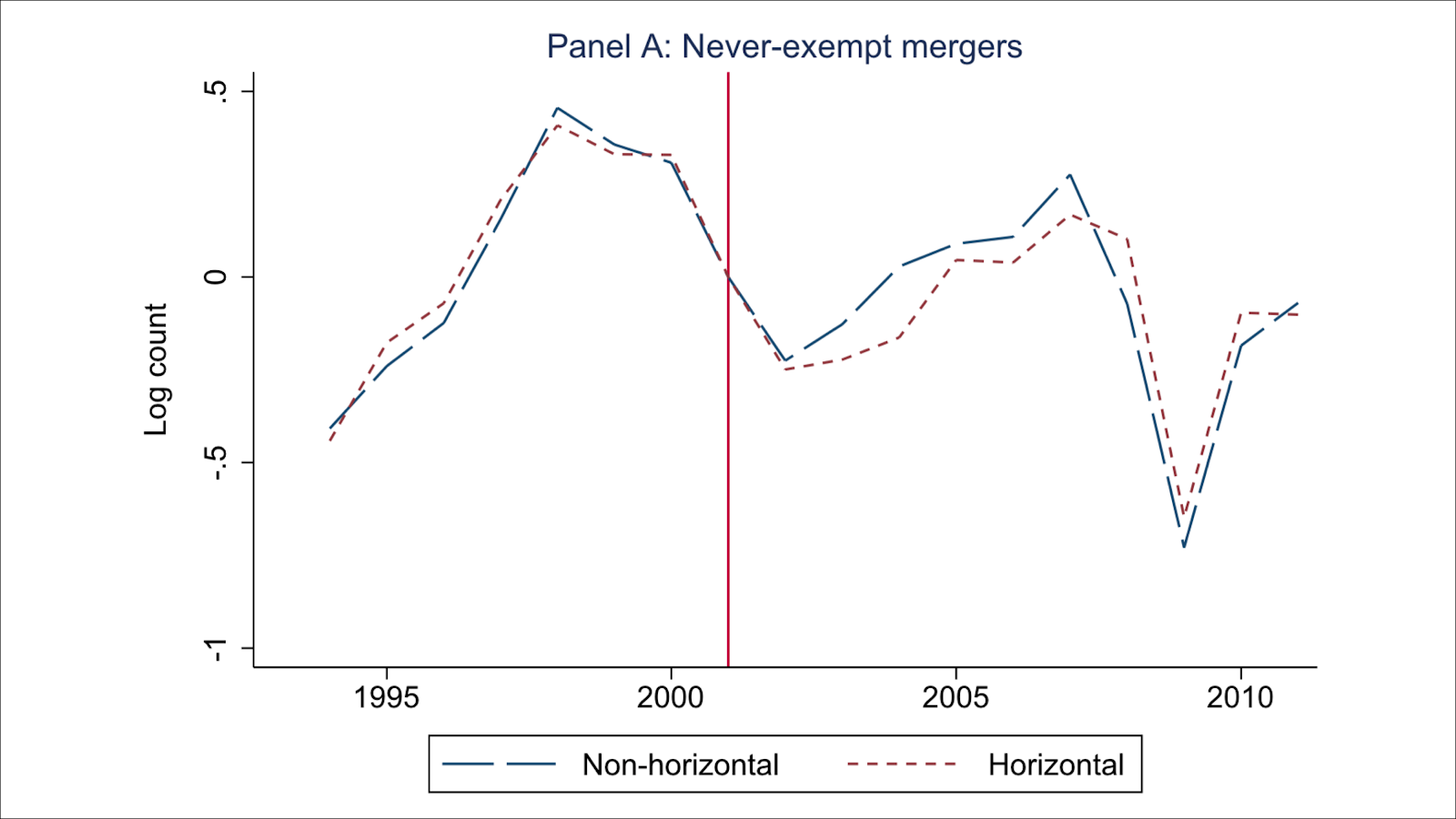

According to Wollmann, here’s what notifications look like for never-exempt mergers (>$50M):

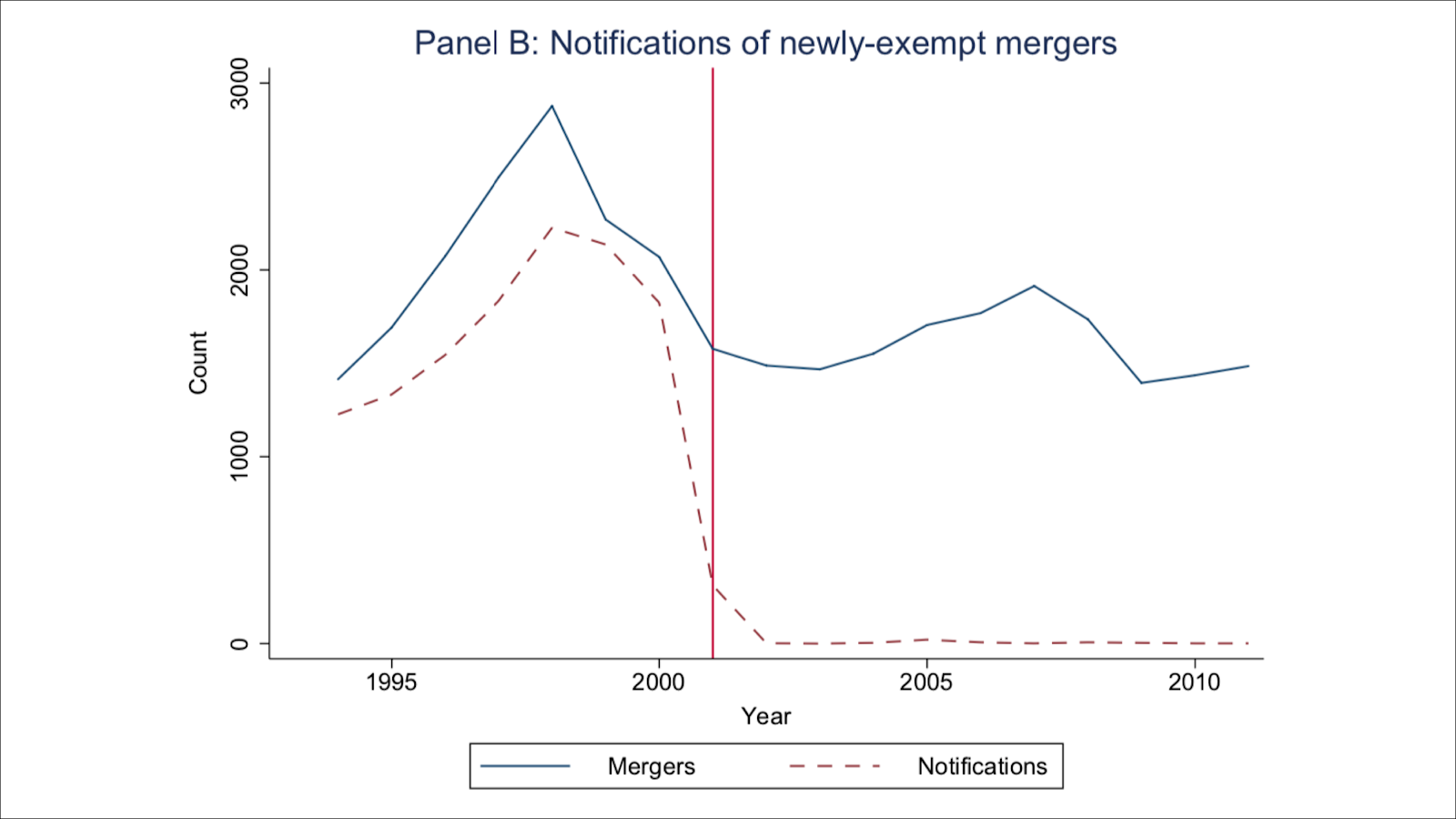

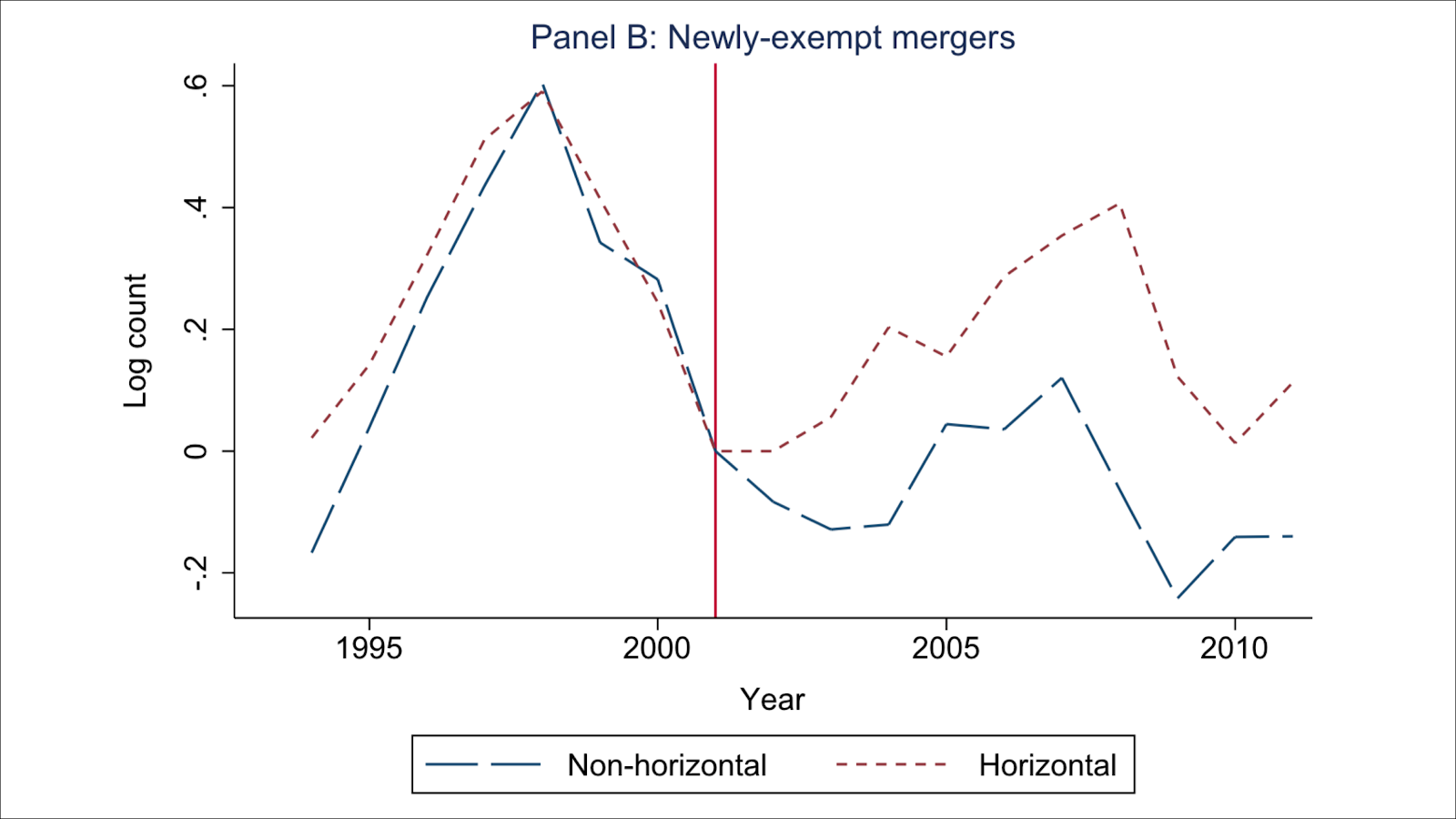

And here’s what notifications for newly-exempt ($15M

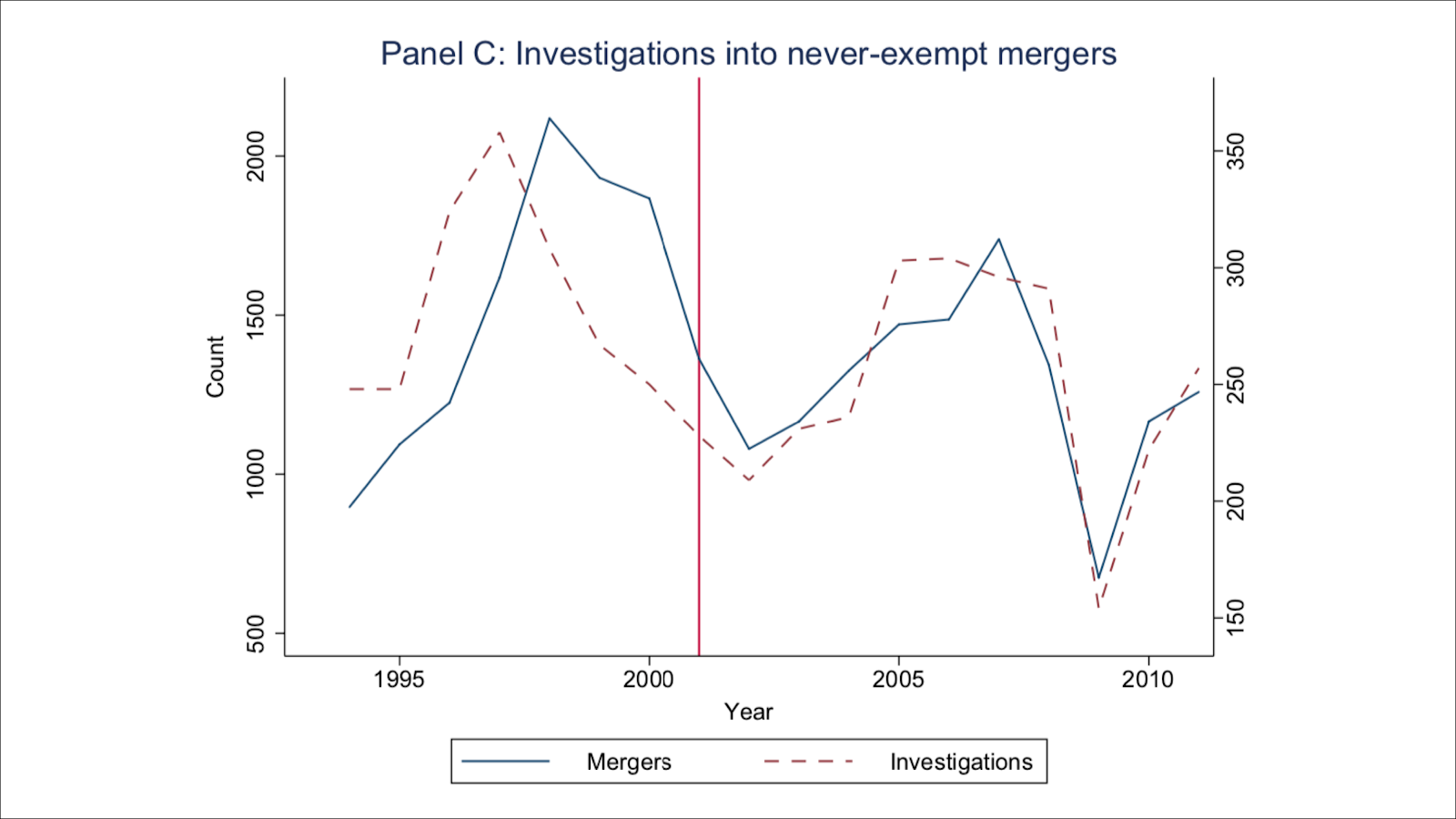

So what does that mean for merger investigations? Here is the number of investigations into never-exempt mergers:

We see a pretty consistent relationship between number of mergers and number of investigations. More mergers means more investigations.

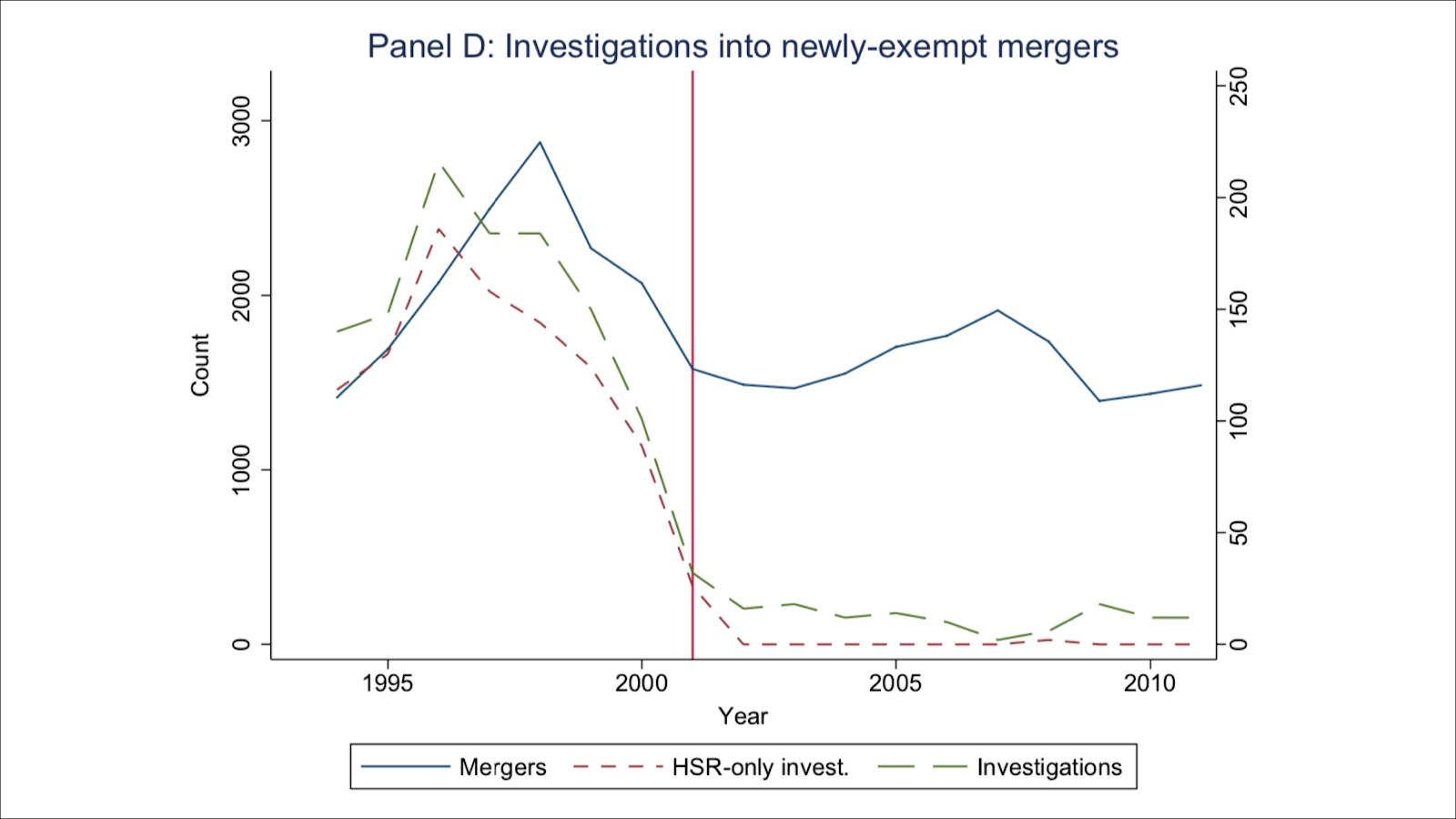

How about for newly-exempt mergers?

Here, investigations go to zero while merger activity remains relatively stable. In other words, it appears that some mergers that would have been investigated had they required an HSR notification were not investigated.

Wollmann then uses four-digit SIC code industries to sort mergers into horizontal and non-horizontal categories. Here are never-exempt mergers:

He finds that almost all of the increase in merger activity (relative to the counterfactual in which the notification threshold were unchanged) is driven by horizontal mergers. And here are newly-exempt mergers:

Policy Implications & Limitations

The charts show a stark change in investigations and merger activity. The difference-in-differences methodology is solid and the author addresses some potential confounding variables (such as presidential elections). However, the paper leaves the broader implications for public policy unanswered.

Furthermore, given the limits of the data in this analysis, it’s not possible for this approach to explain competitive effects in the relevant antitrust markets, for three reasons:

Four-digit SIC code industries are not antitrust markets

Wollmann chose to classify mergers “as horizontal or non-horizontal based on whether or not the target and acquirer operate in the same four-digit SIC code industry, which is common convention.” But as Werden & Froeb (2018) notes, four-digit SIC code industries are orders of magnitude too large in most cases to be useful for antitrust analysis:

The evidence from cartel cases focused on indictments from 1970–80. Because the Justice Department prosecuted many local cartels, for 52 of the 80 indictments examined, the Commerce Quotient was less than 0.01, i.e., the SIC 4-digit industry was at least 100 times the apparent scope of the affected market. Of the 80 indictments, 19 involved SIC 4-digit industries that had been thought to comport well with markets, so these were the most instructive. For 16 of the 19, the SIC 4-digit industry was at least 10 times the apparent scope of the affected market (i.e., the Commerce Quotient was less than 0.1).

Antitrust authorities do not rely on SIC 4-digit industry codes and instead establish a market definition based on the facts of each case. It is not possible to infer competitive effects from census data as Wollmann attempts to do.

The data cannot distinguish between anticompetitive mergers and procompetitive mergers

As Wollmann himself notes, the results tell us nothing about the relative costs and benefits of the new HSR policy:

Even so, these findings do not on their own advocate for one policy over another. To do so requires equating industry consolidation to a specific amount of economic harm and then comparing the resulting figure to the benefits derived from raising thresholds, which could be large. Even if the agencies ignore the reduced regulatory burden on firms, introducing exemptions can free up agency resources to pursue other cases (or reduce public spending). These and related issues require careful consideration but simply fall outside the scope of the present work.

For instance, firms could be reallocating merger activity to targets below the new threshold to avoid erroneous enforcement or they could be increasing merger activity for small targets due to reduced regulatory costs and uncertainty.

The study is likely underpowered for effects on blocked mergers

While the paper provides convincing evidence that investigations of newly-exempt mergers decreased dramatically following the change in the notification threshold, there is no equally convincing evidence of an effect on blocked mergers. As Wollmann points out, blocked mergers were exceedingly rare both before and after the Amendment (emphasis added):

Over 57,000 mergers comprise the sample, which spans eighteen years. The mean number of mergers each year is 3,180. The DOJ and FTC receive 31,464 notifications over this period, or 1,748 per year. Also, as stated above, blocked mergers are very infrequent: there are on average 13 per year pre-Amendment and 9 per-year post-Amendment.

Since blocked mergers are such a small percentage of total mergers both before and after the Amendment, we likely cannot tell from the data whether actual enforcement action changed significantly due to the change in notification threshold.

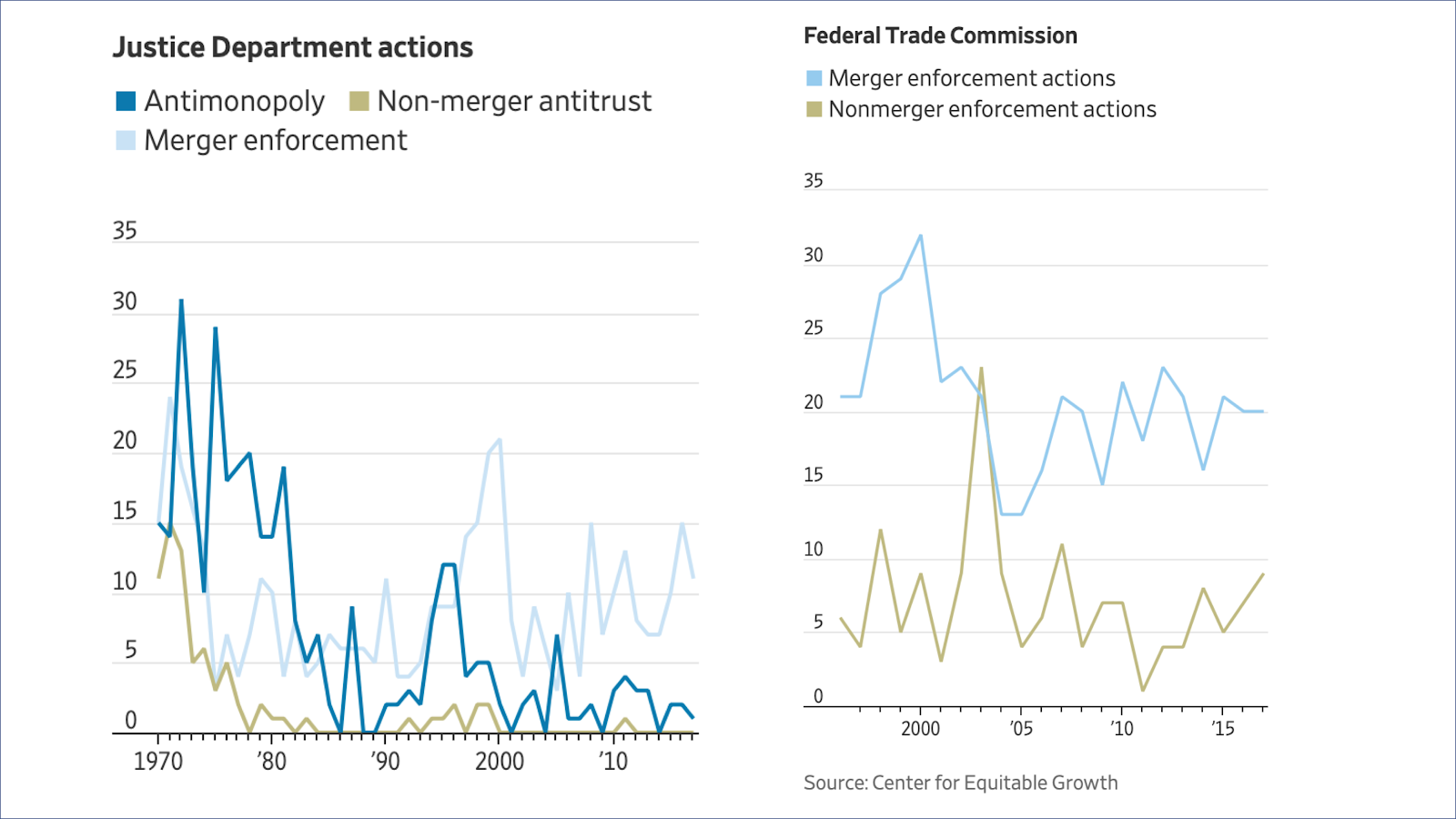

Greg Ip’s write-up for the WSJ includes some relevant charts for this issue. Ironically for a piece about the problems of lax merger review, the accompanying graphs show merger enforcement actions slightly increasing at both the FTC and the DOJ since 2001:

Source: WSJ

Overall, Wollmann’s paper does an effective job showing how changes in premerger notification rules can affect merger activity. However, due to data limitations, we cannot conclude anything about competitive effects or enforcement intensity from this study.