This is the third in a series of TOTM blog posts discussing the Commission’s recently published Google Android decision (the first post can be found here, and the second here). It draws on research from a soon-to-be published ICLE white paper.

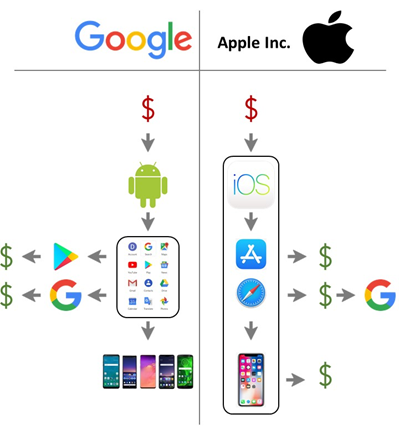

(Comparison of Google and Apple’s smartphone business models. Red $ symbols represent money invested; Green $ symbols represent sources of revenue; Black lines show the extent of Google and Apple’s control over their respective platforms)

For the third in my series of posts about the Google Android decision, I will delve into the theories of harm identified by the Commission.

The big picture is that the Commission’s analysis was particularly one-sided. The Commission failed to adequately account for the complex business challenges that Google faced – such as monetizing the Android platform and shielding it from fragmentation. To make matters worse, its decision rests on dubious factual conclusions and extrapolations. The result is a highly unbalanced assessment that could ultimately hamstring Google and prevent it from effectively competing with its smartphone rivals, Apple in particular.

1. Tying without foreclosure

The first theory of harm identified by the Commission concerned the tying of Google’s Search app with the Google Play app, and of Google’s Chrome app with both the Google Play and Google Search apps.

Oversimplifying, Google required its OEMs to choose between either pre-installing a bundle of Google applications, or forgoing some of the most important ones (notably Google Play). The Commission argued that this gave Google a competitive advantage that rivals could not emulate (even though Google’s terms did not preclude OEMs from simultaneously pre-installing rival web browsers and search apps).

To support this conclusion, the Commission notably asserted that no alternative distribution channel would enable rivals to offset the competitive advantage that Google obtained from tying. This finding is, at best, dubious.

For a start, the Commission claimed that user downloads were not a viable alternative distribution channel, even though roughly 250 million apps are downloaded on Google’s Play store every day.

The Commission sought to overcome this inconvenient statistic by arguing that Android users were unlikely to download apps that duplicated the functionalities of a pre-installed app – why download a new browser if there is already one on the user’s phone?

But this reasoning is far from watertight. For instance, the 17th most-downloaded Android app, the “Super-Bright Led Flashlight” (with more than 587million downloads), mostly replicates a feature that is pre-installed on all Android devices. Moreover, the five most downloaded Android apps (Facebook, Facebook Messenger, Whatsapp, Instagram and Skype) provide functionalities that are, to some extent at least, offered by apps that have, at some point or another, been preinstalled on many Android devices (notably Google Hangouts, Google Photos and Google+).

The Commission countered that communications apps were not appropriate counterexamples, because they benefit from network effects. But this overlooks the fact that the most successful communications and social media apps benefited from very limited network effects when they were launched, and that they succeeded despite the presence of competing pre-installed apps. Direct user downloads are thus a far more powerful vector of competition than the Commission cared to admit.

Similarly concerning is the Commission’s contention that paying OEMs or Mobile Network Operators (“MNOs”) to pre-install their search apps was not a viable alternative for Google’s rivals. Some of the reasons cited by the Commission to support this finding are particularly troubling.

For instance, the Commission claimed that high transaction costs prevented parties from concluding these pre installation deals.

But pre-installation agreements are common in the smartphone industry. In recent years, Microsoft struck a deal with Samsung to pre-install some of its office apps on the Galaxy Note 10. It also paid Verizon to pre-install the Bing search app on a number of Samsung phones, in 2010. Likewise, a number of Russian internet companies have been in talks with Huawei to pre-install their apps on its devices. And Yahoo reached an agreement with Mozilla to make it the default search engine for its web browser. Transaction costs do not appear to have been an obstacle in any of these cases.

The Commission also claimed that duplicating too many apps would cause storage space issues on devices.

And yet, a back-of-the-envelope calculation suggests that storage space is unlikely to be a major issue. For instance, the Bing Search app has a download size of 24MB, whereas typical entry-level smartphones generally have an internal memory of at least 64GB (that can often be extended to more than 1TB with the addition of an SD card). The Bing Search app thus takes up less than one-thousandth of these devices’ internal storage. Granted, the Yahoo search app is slightly larger than Microsoft’s, weighing almost 100MB. But this is still insignificant compared to a modern device’s storage space.

Finally, the Commission claimed that rivals were contractually prevented from concluding exclusive pre-installation deals because Google’s own apps would also be pre-installed on devices.

However, while it is true that Google’s apps would still be present on a device, rivals could still pay for their applications to be set as default. Even Yandex – a plaintiff – recognized that this would be a valuable solution. In its own words (taken from the Commission’s decision):

Pre-installation alongside Google would be of some benefit to an alternative general search provider such as Yandex […] given the importance of default status and pre-installation on home screen, a level playing field will not be established unless there is a meaningful competition for default status instead of Google.

In short, the Commission failed to convincingly establish that Google’s contractual terms prevented as-efficient rivals from effectively distributing their applications on Android smartphones. The evidence it adduced was simply too thin to support anything close to that conclusion.

2. The threat of fragmentation

The Commission’s second theory of harm concerned the so-called “antifragmentation” agreements concluded between Google and OEMs. In a nutshell, Google only agreed to license the Google Search and Google Play apps to OEMs that sold “Android Compatible” devices (i.e. devices sold with a version of Android did not stray too far from Google’s most recent version).

According to Google, this requirement was necessary to limit the number of Android forks that were present on the market (as well as older versions of the standard Android). This, in turn, reduced development costs and prevented the Android platform from unraveling.

The Commission disagreed, arguing that Google’s anti-fragmentation provisions thwarted competition from potential Android forks (i.e. modified versions of the Android OS).

This conclusion raises at least two critical questions: The first is whether these agreements were necessary to ensure the survival and competitiveness of the Android platform, and the second is why “open” platforms should be precluded from partly replicating a feature that is essential to rival “closed” platforms, such as Apple’s iOS.

Let us start with the necessity, or not, of Google’s contractual terms. If fragmentation did indeed pose an existential threat to the Android ecosystem, and anti-fragmentation agreements averted this threat, then it is hard to make a case that they thwarted competition. The Android platform would simply not have been as viable without them.

The Commission dismissed this possibility, relying largely on statements made by Google’s rivals (many of whom likely stood to benefit from the suppression of these agreements). For instance, the Commission cited comments that it received from Yandex – one of the plaintiffs in the case:

(1166) The fact that fragmentation can bring significant benefits is also confirmed by third-party respondents to requests for information:

[…](2) Yandex, which stated: “Whilst the development of Android forks certainly has an impact on the fragmentation of the Android ecosystem in terms of additional development being required to adapt applications for various versions of the OS, the benefits of fragmentation outweigh the downsides…”

Ironically, the Commission relied on Yandex’s statements while, at the same time, it dismissed arguments made by Android app developers, on account that they were conflicted. In its own words:

Google attached to its Response to the Statement of Objections 36 letters from OEMs and app developers supporting Google’s views about the dangers of fragmentation […] It appears likely that the authors of the 36 letters were influenced by Google when drafting or signing those letters.

More fundamentally, the Commission’s claim that fragmentation was not a significant threat is at odds with an almost unanimous agreement among industry insiders.

For example, while it is not dispositive, a rapid search for the terms “Google Android fragmentation”, using the DuckDuckGo search engine, leads to results that cut strongly against the Commission’s conclusions. Of the ten first results, only one could remotely be construed as claiming that fragmentation was not an issue. The others paint a very different picture (below are some of the most salient excerpts):

“There’s a fairly universal perception that Android fragmentation is a barrier to a consistent user experience, a security risk, and a challenge for app developers.” (here)

“Android fragmentation, a problem with the operating system from its inception, has only become more acute an issue over time, as more users clamor for the latest and greatest software to arrive on their phones.” (here)

“Android Fragmentation a Huge Problem: Study.” (here)

“Google’s Android fragmentation fix still isn’t working at all.” (here)

“Does Google care about Android fragmentation? Not now—but it should.” (here).

“This is very frustrating to users and a major headache for Google… and a challenge for corporate IT,” Gold said, explaining that there are a large number of older, not fully compatible devices running various versions of Android.” (here)

Perhaps more importantly, one might question why Google should be treated differently than rivals that operate closed platforms, such as Apple, Microsoft and Blackberry (before the last two mostly exited the Mobile OS market). By definition, these platforms limit all potential forks (because they are based on proprietary software).

The Commission argued that Apple, Microsoft and Blackberry had opted to run “closed” platforms, which gave them the right to prevent rivals from copying their software.

While this answer has some superficial appeal, it is incomplete. Android may be an open source project, but this is not true of Google’s proprietary apps. Why should it be forced to offer them to rivals who would use them to undermine its platform? The Commission did not meaningfully consider this question.

And yet, industry insiders routinely compare the fragmentation of Apple’s iOS and Google’s Android OS, in order to gage the state of competition between both firms. For instance, one commentator noted:

[T]he gap between iOS and Android users running the latest major versions of their operating systems has never looked worse for Google.

Likewise, an article published in Forbes concluded that Google’s OEMs were slow at providing users with updates, and that this might drive users and developers away from the Android platform:

For many users the Android experience isn’t as up-to-date as Apple’s iOS. Users could buy the latest Android phone now and they may see one major OS update and nothing else. […] Apple users can be pretty sure that they’ll get at least two years of updates, although the company never states how long it intends to support devices.

However this problem, in general, makes it harder for developers and will almost certainly have some inherent security problems. Developers, for example, will need to keep pushing updates – particularly for security issues – to many different versions. This is likely a time-consuming and expensive process.

To recap, the Commission’s decision paints a world that is either black or white: either firms operate closed platforms, and they are then free to limit fragmentation as they see fit, or they create open platforms, in which case they are deemed to have accepted much higher levels of fragmentation.

This stands in stark contrast to industry coverage, which suggests that users and developers of both closed and open platforms care a great deal about fragmentation, and demand that measures be put in place to address it. If this is true, then the relative fragmentation of open and closed platforms has an important impact on their competitive performance, and the Commission was wrong to reject comparisons between Google and its closed ecosystem rivals.

3. Google’s revenue sharing agreements

The last part of the Commission’s case centered on revenue sharing agreements between Google and its OEMs/MNOs. Google paid these parties to exclusively place its search app on the homescreen of their devices. According to the Commission, these payments reduced OEMs and MNOs’ incentives to pre-install competing general search apps.

However, to reach this conclusion, the Commission had to make the critical (and highly dubious) assumption that rivals could not match Google’s payments.

To get to that point, it notably assumed that rival search engines would be unable to increase their share of mobile search results beyond their share of desktop search results. The underlying intuition appears to be that users who freely chose Google Search on desktop (Google Search & Chrome are not set as default on desktop PCs) could not be convinced to opt for a rival search engine on mobile.

But this ignores the possibility that rivals might offer an innovative app that swayed users away from their preferred desktop search engine.

More importantly, this reasoning cuts against the Commission’s own claim that pre-installation and default placement were critical. If most users, dismiss their device’s default search app and search engine in favor of their preferred ones, then pre-installation and default placement are largely immaterial, and Google’s revenue sharing agreements could not possibly have thwarted competition (because they did not prevent users from independently installing their preferred search app). On the other hand, if users are easily swayed by default placement, then there is no reason to believe that rivals could not exceed their desktop market share on mobile phones.

The Commission was also wrong when it claimed that rival search engines were at a disadvantage because of the structure of Google’s revenue sharing payments. OEMs and MNOs allegedly lost all of their payments from Google if they exclusively placed a rival’s search app on the home screen of a single line of handsets.

The key question is the following: could Google automatically tilt the scales to its advantage by structuring the revenue sharing payments in this way? The answer appears to be no.

For instance, it has been argued that exclusivity may intensify competition for distribution. Conversely, other scholars have claimed that exclusivity may deter entry in network industries. Unfortunately, the Commission did not examine whether Google’s revenue sharing agreements fell within this category.

It thus provided insufficient evidence to support its conclusion that the revenue sharing agreements reduced OEMs’ (and MNOs’) incentives to pre-install competing general search apps, rather than merely increasing competition “for the market”.

4. Conclusion

To summarize, the Commission overestimated the effect that Google’s behavior might have on its rivals. It almost entirely ignored the justifications that Google put forward and relied heavily on statements made by its rivals. The result is a one-sided decision that puts undue strain on the Android Business model, while providing few, if any, benefits in return.