This article is a part of the The Law, Economics, and Policy of the COVID-19 Pandemic symposium.

Earlier this week, merger talks between Uber and food delivery service Grubhub surfaced. House Antitrust Subcommittee Chairman David N. Cicilline quickly reacted to the news:

Americans are struggling to put food on the table, and locally owned businesses are doing everything possible to keep serving people in our communities, even under great duress. Uber is a notoriously predatory company that has long denied its drivers a living wage. Its attempt to acquire Grubhub—which has a history of exploiting local restaurants through deceptive tactics and extortionate fees—marks a new low in pandemic profiteering. We cannot allow these corporations to monopolize food delivery, especially amid a crisis that is rendering American families and local restaurants more dependent than ever on these very services. This deal underscores the urgency for a merger moratorium, which I and several of my colleagues have been urging our caucus to support.

Pandemic profiteering rolls nicely off the tongue, and we’re sure to see that phrase much more over the next year or so.

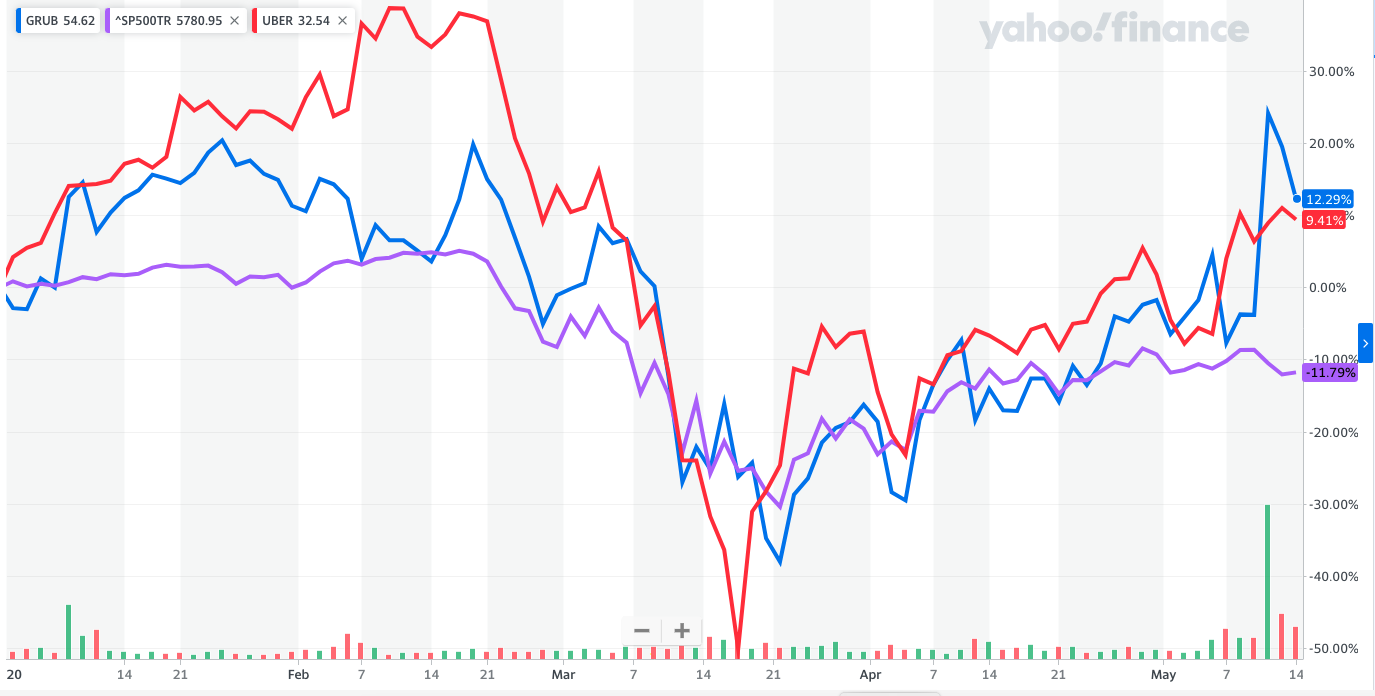

Grubhub shares jumped 29% Tuesday, the day the merger talks came to light, shown in the figure below. The Wall Street Journal reports companies are considering a deal that would value Grubhub stock at around 1.9 Uber shares, or $60-65 dollars a share, based on Thursday’s price.

But is that “pandemic profiteering?”

After Amazon announced its intended acquisition of Whole Foods, the grocer’s stock price soared by 27%. Rep. Cicilline voiced some convoluted concerns about that merger, but said nothing about profiteering at the time. Different times, different messaging.

Rep. Cicilline and others have been calling for a merger moratorium during the pandemic and used the Uber/Grubhub announcement as Exhibit A in his indictment of merger activity.

A moratorium would make things much easier for regulators. No more fighting over relevant markets, no HHI calculations, no experts debating SSNIPs or GUPPIs, no worries over consumer welfare, no failing firm defenses. Just a clear, brightline “NO!”

Even before the pandemic, it was well known that the food delivery industry was due for a shakeout. NPR reports, even as the business is growing, none of the top food-delivery apps are turning a profit, with one analyst concluding consolidation was “inevitable.” Thus, even if a moratorium slowed or stopped the Uber/Grubhub merger, at some point a merger in the industry will happen and the U.S. antitrust authorities will have to evaluate it.

First, we have to ask, “What’s the relevant market?” The government has a history of defining relevant markets so narrowly that just about any merger can be challenged. For example, for the scuttled Whole Foods/Wild Oats merger, the FTC famously narrowed the market to “premium natural and organic supermarkets.” Surely, similar mental gymnastics will be used for any merger involving food delivery services.

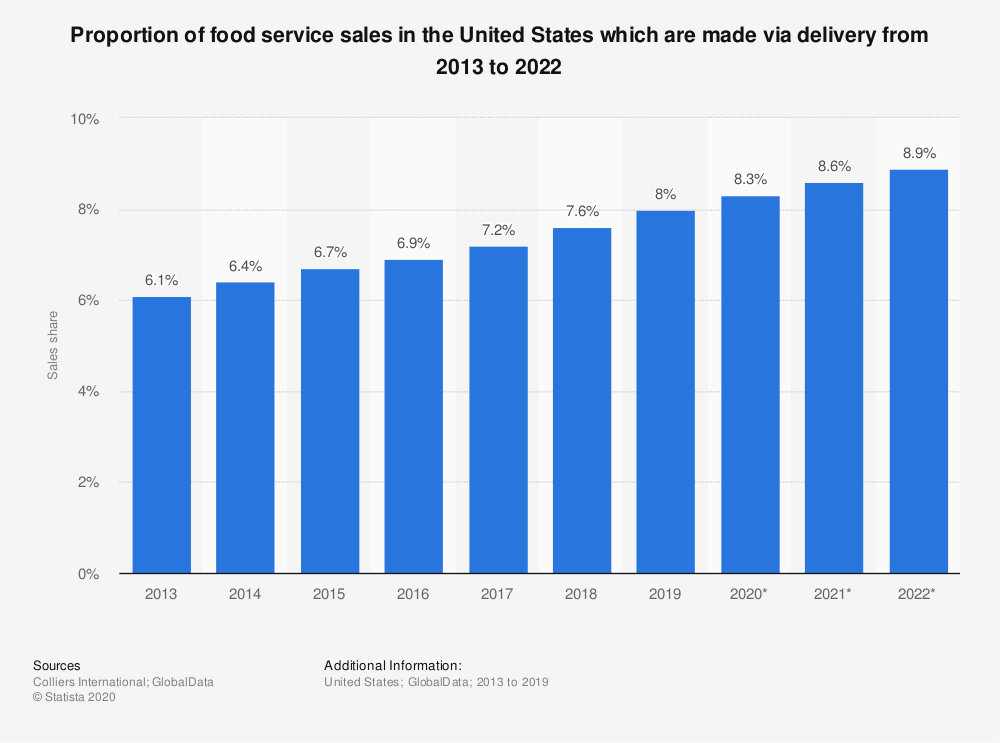

While food delivery has grown in popularity over the past few years, delivery represents less than 10% of U.S. food service sales. While Rep. Cicilline may be correct that families and local restaurants are “more dependent than ever” on food delivery, delivery is only a small fraction of a large market. Even a monopoly of food delivery service would not confer market power on the restaurant and food service industry.

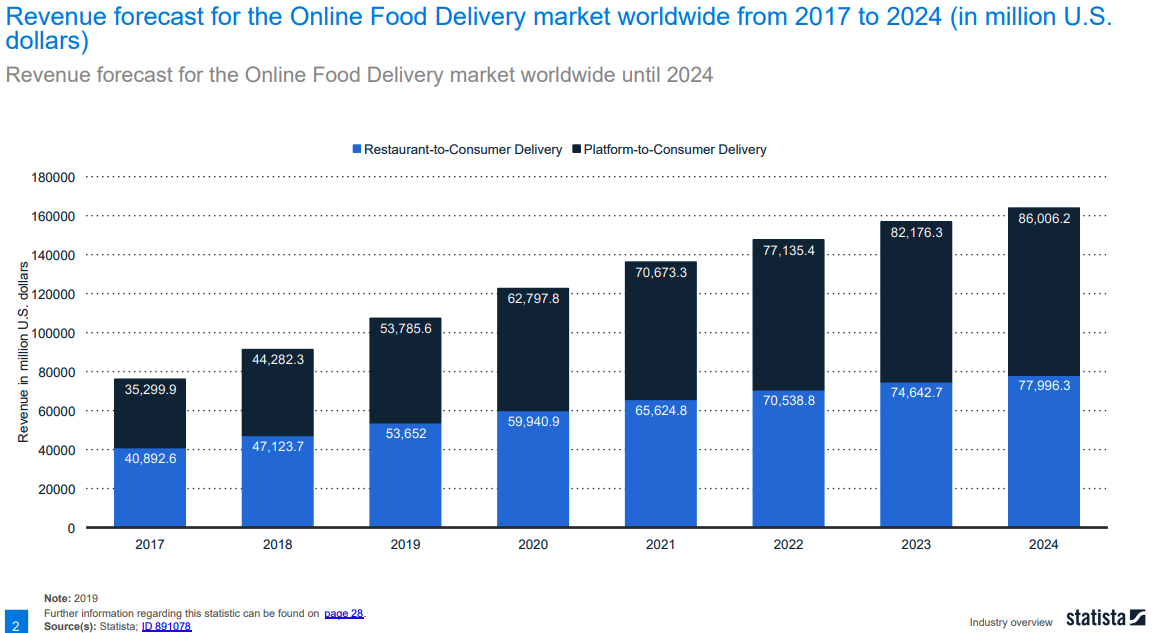

No reasonable person would claim an Uber/Grubhub merger would increase market power in the restaurant and food service industry. But, it might convey market power in the food delivery market. Much attention is paid to the “Big Four”–DoorDash, Grubhub, Uber Eats, and Postmates. But, these platform delivery services are part of the larger food service delivery market, of which platforms account for about half of the industry’s revenues. Pizza accounts for the largest share of restaurant-to-consumer delivery.

This raises the big question of what is the relevant market: Is it the entire food delivery sector, or just the platform-to-consumer sector?

Based on the information in the figure below, defining the market narrowly would place an Uber/Grubhub merger squarely in the “presumed to be likely to enhance market power” category.

- 2016 HHI: <3,175

- 2018 HHI: <1,474

- 2020 HHI: <2,249 pre-merger; <4,153 post-merger

Alternatively, defining the market to encompass all food delivery would cut the platforms’ shares roughly in half and the merger would be unlikely to harm competition, based on HHI. Choosing the relevant market is, well, relevant.

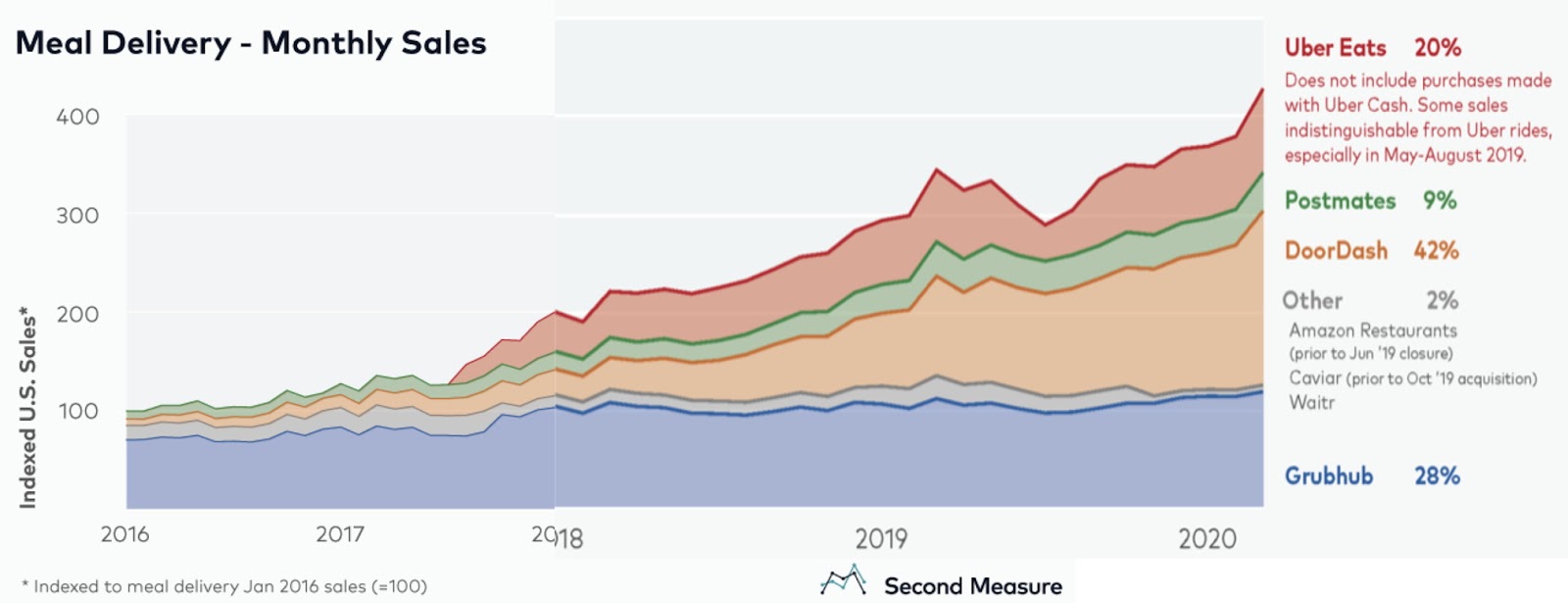

The Second Measure data suggests that concentration in the platform delivery sector decreased with the entry of Uber Eats, but subsequently increased with DoorDash’s rising share–which included the acquisition of Caviar from Square.

(NB: There seems to be a significant mismatch in the delivery revenue data. Statista reports platform delivery revenues increased by about 40% from 2018 to 2020, but Second Measure indicates revenues have more than doubled.)

Geoffrey Manne, in an earlier post points out “while national concentration does appear to be increasing in some sectors of the economy, it’s not actually so clear that the same is true for local concentration — which is often the relevant antitrust market.” That may be the case here.

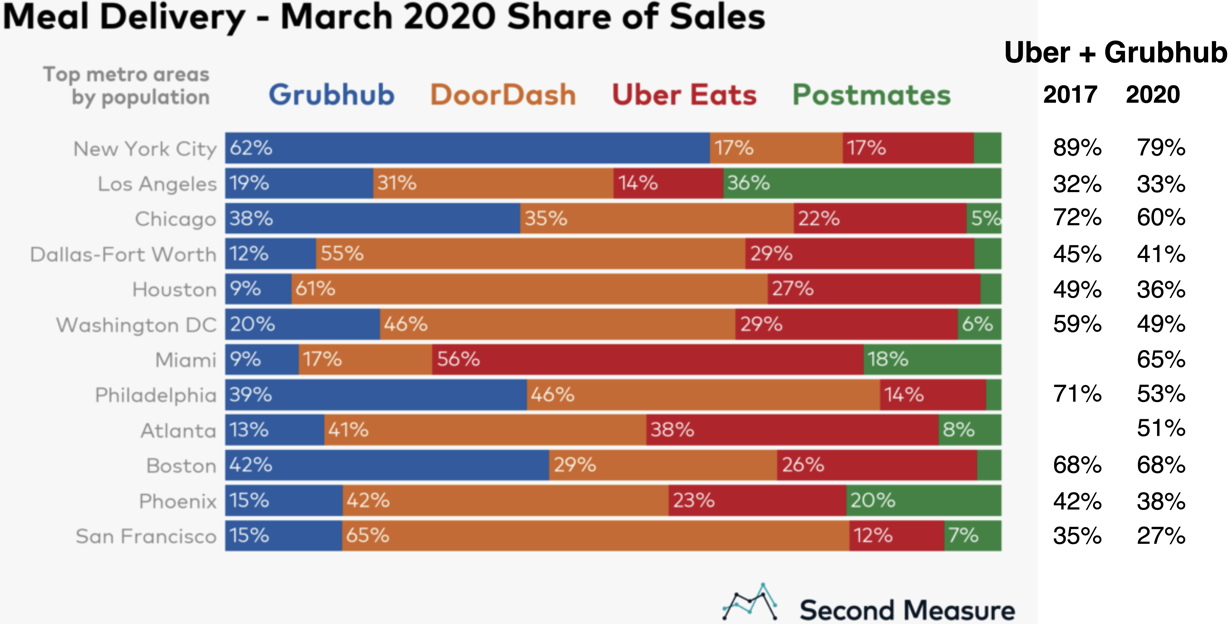

The figure below is a sample of platform delivery shares by city. I added data from an earlier study of 2017 shares. In all but two metro areas, Uber and Grubhub’s combined market share declined from 2017 to 2020. In Boston, the combined shares did not change and in Los Angeles, the combined shares increased by 1%.

(NB: There are some serious problems with this data, notably that it leaves out the restaurant-to-consumer sector and assumes the entire platform-to-consumer sector is comprised of only the “Big Four.”)

Platform-to-consumer delivery is a complex two-sided market in which the platforms link, and compete for, both restaurants and consumers. Platforms compete for restaurants, drivers, and consumers. Restaurants have a choice of using multiple platforms or entering into exclusive arrangements. Many drivers work for multiple platforms, and many consumers use multiple platforms.

Fundamentally, the rise of platform-to-consumer is an evolution in vertical integration. Restaurants can choose to offer no delivery, use their own in-house delivery drivers, or use a third party delivery service. Every platform faces competition from in-house delivery, placing a limit on their ability to raise prices to restaurants and consumers.

The choice of delivery is not an either-or decision. For example, many pizza restaurants who have their own delivery drivers also use platform delivery service. Their own drivers may serve a limited geographic area, but the platforms allow the restaurant to expand its geographic reach, thereby increasing its sales. Even so, the platforms face competition from in-house delivery.

Mergers or other forms of shake out in the food delivery industry are inevitable. Mergers will raise important questions about relevant product and geographic markets as well as competition in two-sided markets. While there is a real risk of harm to restaurants, drivers, and consumers, there is also a real possibility of welfare enhancing efficiencies. These questions will never be addressed with an across-the-board merger moratorium.