[TOTM: The following is part of a blog series by TOTM guests and authors on the law, economics, and policy of the ongoing COVID-19 pandemic. The entire series of posts is available here.

This post is authored by Geoffrey A. Manne, (President, ICLE; Distinguished Fellow, Northwestern University Center on Law, Business, and Economics); and Dirk Auer, (Senior Fellow of Law & Economics, ICLE)]

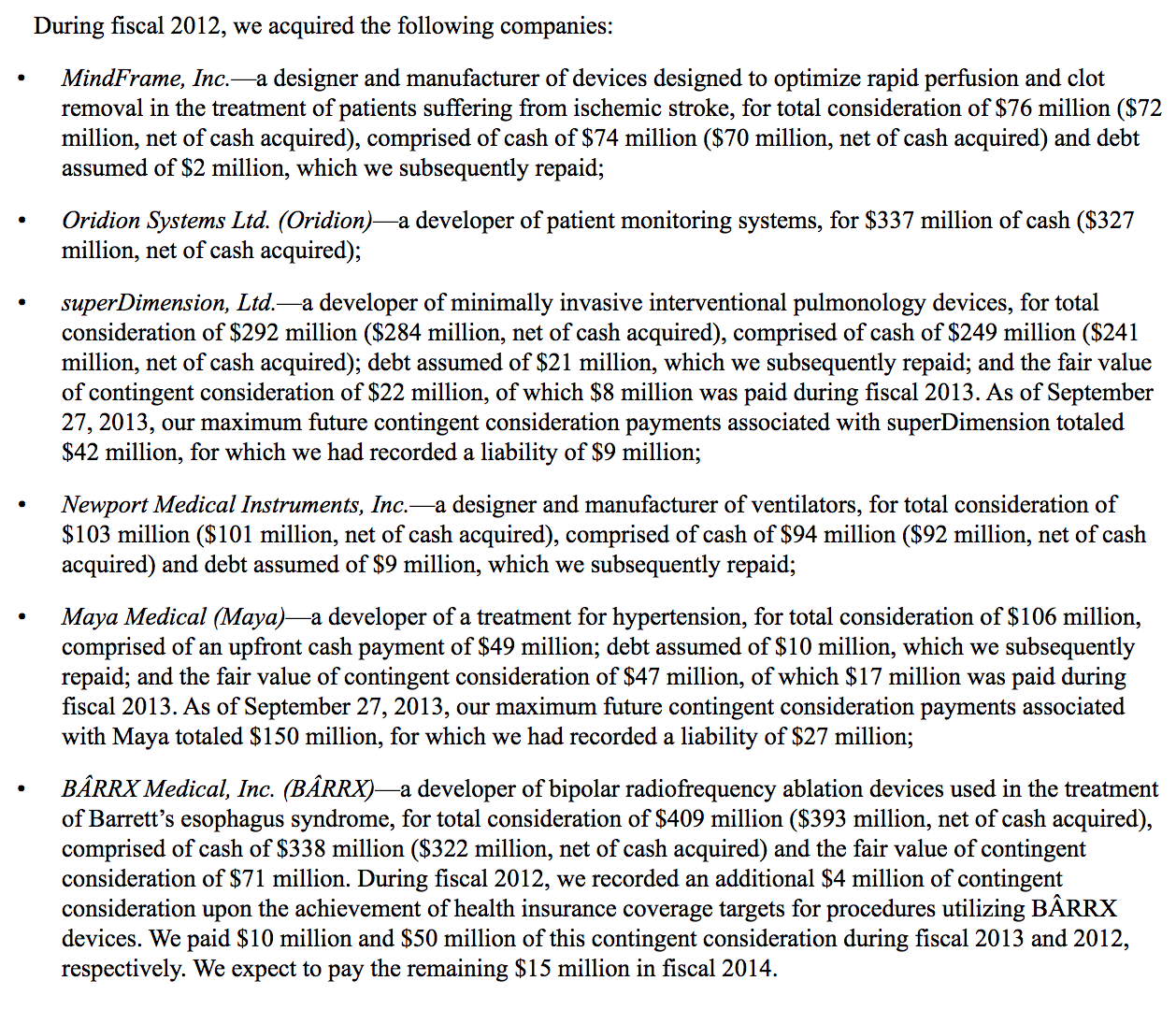

Back in 2012, Covidien, a large health care products company and medical device manufacturer, purchased Newport Medical Instruments, a small ventilator developer and manufacturer. (Covidien itself was subsequently purchased by Medtronic in 2015).

Eight years later, in the midst of the coronavirus pandemic, the New York Times has just published an article revisiting the Covidien/Newport transaction, and questioning whether it might have contributed to the current shortage of ventilators.

The article speculates that Covidien’s purchase of Newport, and the subsequent discontinuation of Newport’s “Aura” ventilator — which was then being developed by Newport under a government contract — delayed US government efforts to procure mechanical ventilators until the second half of 2020 — too late to treat the first wave of COVID-19 patients:

And then things suddenly veered off course. A multibillion-dollar maker of medical devices bought the small California company that had been hired to design the new machines. The project ultimately produced zero ventilators.

That failure delayed the development of an affordable ventilator by at least half a decade, depriving hospitals, states and the federal government of the ability to stock up.

* * *

Today, with the coronavirus ravaging America’s health care system, the nation’s emergency-response stockpile is still waiting on its first shipment.

The article has generated considerable interest not so much for what it suggests about government procurement policies or for its relevance to the ventilator shortages associated with the current pandemic, but rather for its purported relevance to ongoing antitrust debates and the arguments put forward by “antitrust populists” and others that merger enforcement in the US is dramatically insufficient.

Only a single sentence in the article itself points to a possible antitrust story — and it does nothing more than report unsubstantiated speculation from unnamed “government officials” and rival companies:

Government officials and executives at rival ventilator companies said they suspected that Covidien had acquired Newport to prevent it from building a cheaper product that would undermine Covidien’s profits from its existing ventilator business.

Nevertheless, and right on cue, various antitrust scholars quickly framed the deal as a so-called “killer acquisition” (see also here and here):

Unsurprisingly, politicians were also quick to jump on the bandwagon. David Cicilline, the powerful chairman of the House Antitrust Subcommittee, opined that:

And FTC Commissioner Rebecca Kelly Slaughter quickly called for a retrospective review of the deal:

The public reporting on this acquisition raises important questions about the review of this deal. We should absolutely be looking back to figure out what happened.

These “hot takes” raise a crucial issue. The New York Times story opened the door to a welter of hasty conclusions offered to support the ongoing narrative that antitrust enforcement has failed us — in this case quite literally at the cost of human lives. But are any of these claims actually supportable?

Unfortunately, the competitive realities of the mechanical ventilator industry, as well as a more clear-eyed view of what was likely going on with the failed government contract at the heart of the story, simply do not support the “killer acquisition” story.

What is a “killer acquisition”…?

Let’s take a step back. Because monopoly profits are, by definition, higher than joint duopoly profits (all else equal), economists have long argued that incumbents may find it profitable to acquire smaller rivals in order to reduce competition and increase their profits. More specifically, incumbents may be tempted to acquire would-be entrants in order to prevent them from introducing innovations that might hurt the incumbent’s profits.

For this theory to have any purchase, however, a number of conditions must hold. Most importantly, as Colleen Cunningham, Florian Ederer, and Song Ma put it in an influential paper:

“killer acquisitions” can only occur when the entrepreneur’s project overlaps with the acquirer’s existing product…. [W]ithout any product market overlap, the acquirer never has a strictly positive incentive to acquire the entrepreneur… because, without overlap, acquiring the project does not give the acquirer any gains resulting from reduced competition, and the two bargaining entities have exactly the same value for the project.

Moreover, the authors add that:

Successfully developing a new product draws consumer demand and profits away equally from all existing products. An acquiring incumbent is hurt more by such cannibalization when he is a monopolist (i.e., the new product draws demand away only from his own existing product) than when he already faces many other existing competitors (i.e., cannibalization losses are spread over many firms). As a result, as the number of existing competitors increases, the replacement effect decreases and the acquirer’s development decisions become more similar to those of the entrepreneur.

Finally, the “killer acquisition” terminology is appropriate only when the incumbent chooses to discontinue its rival’s R&D project:

If incumbents face significant existing competition, acquired projects are not significantly more frequently discontinued than independent projects. Thus, more competition deters incumbents from acquiring and terminating the projects of potential future competitors, which leads to more competition in the future.

…And what isn’t a killer acquisition?

What is left out of this account of killer acquisitions is the age-old possibility that an acquirer purchases a rival precisely because it has superior know-how or a superior governance structure that enables it to realize greater return and more productivity than its target. In the case of a so-called killer acquisition, this means shutting down a negative ROI project and redeploying resources to other projects or other uses — including those that may not have any direct relation to the discontinued project.

Such “synergistic” mergers are also — like allegedly “killer” mergers — likely to involve acquirers and targets in the same industry and with technological overlap between their R&D projects; it is in precisely these situations that the acquirer is likely to have better knowledge than the target’s shareholders that the target is undervalued because of poor governance rather than exogenous, environmental factors.

In other words, whether an acquisition is harmful or not — as the epithet “killer” implies it is — depends on whether it is about reducing competition from a rival, on the one hand, or about increasing the acquirer’s competitiveness by putting resources to more productive use, on the other.

As argued below, it is highly unlikely that Covidien’s acquisition of Newport could be classified as a “killer acquisition.” There is thus nothing to suggest that the merger materially impaired competition in the mechanical ventilator market, or that it measurably affected the US’s efforts to fight COVID-19.

The market realities of the ventilator market and its implications for the “killer acquisition” story

1. The mechanical ventilator market is highly competitive

As explained above, “killer acquisitions” are less likely to occur in competitive markets. Yet the mechanical ventilator industry is extremely competitive.

A number of reports conclude that there is significant competition in the industry. One source cites at least seven large producers. Another report cites eleven large players. And, in the words of another report:

Medical ventilators market competition is intense.

The conclusion that the mechanical ventilator industry is highly competitive is further supported by the fact that the five largest producers combined reportedly hold only 50% of the market. In other words, available evidence suggests that none of these firms has anything close to a monopoly position.

This intense competition, along with the small market shares of the merging firms, likely explains why the FTC declined to open an in-depth investigation into Covidien’s acquisition of Newport.

Similarly, following preliminary investigations, neither the FTC nor the European Commission saw the need for an in-depth look at the ventilator market when they reviewed Medtronic’s subsequent acquisition of Covidien (which closed in 2015). Although Medtronic did not produce any mechanical ventilators before the acquisition, authorities (particularly the European Commission) could nevertheless have analyzed that market if Covidien’s presumptive market share was particularly high. The fact that they declined to do so tends to suggest that the ventilator market was relatively unconcentrated.

2. The value of the merger was too small

A second strong reason to believe that Covidien’s purchase of Newport wasn’t a killer acquisition is the acquisition’s value of $103 million.

Indeed, if it was clear that Newport was about to revolutionize the ventilator market, then Covidien would likely have been made to pay significantly more than $103 million to acquire it.

As noted above, the crux of the “killer acquisition” theory is that incumbents can induce welfare-reducing acquisitions by offering to acquire their rivals for significantly more than the present value of their rivals’ expected profits. Because an incumbent undertaking a “killer” takeover expects to earn monopoly profits as a result of the transaction, it can offer a substantial premium and still profit from its investment. It is this basic asymmetry that drives the theory.

Indeed, as a recent article by Kevin Bryan and Erik Hovenkamp notes, an acquisition value out of line with current revenues may be an indicator of the significance of a pending acquisition in which enforcers may not actually know the value of the target’s underlying technology:

[Where] a court may lack the expertise to [assess the commercial significance of acquired technology]…, the transaction value… may provide a reasonable proxy. Intuitively, if the startup is a relatively small company with relatively few sales to its name, then a very high acquisition price may reasonably suggest that the startup technology has significant promise.

The strategy only works, however, if the target firm’s shareholders agree that share value properly reflects only “normal” expected profits, and not that the target is poised to revolutionize its market with a uniquely low-cost or high-quality product. Relatively low acquisition prices relative to market size, therefore, tend to reflect low (or normal) expected profits, and a low perceived likelihood of radical innovations occurring.

We can apply this reasoning to Covidien’s acquisition of Newport:

- Precise and publicly available figures concerning the mechanical ventilator market are hard to come by. Nevertheless, one estimate finds that the global ventilator market was worth $2.715 billion in 2012. Another report suggests that the global market was worth $4.30 billion in 2018; still another that it was worth $4.58 billion in 2019.

- As noted above, Covidien reported to the SEC that it paid $103 million to purchase Newport (a firm that produced only ventilators and apparently had no plans to branch out).

- For context, at the time of the acquisition Covidien had annual sales of $11.8 billion overall, and $743 million in sales of its existing “Airways and Ventilation Products.”

If the ventilator market was indeed worth billions of dollars per year, then the comparatively small $108 million paid by Covidien — small even relative to Covidien’s own share of the market — suggests that, at the time of the acquisition, it was unlikely that Newport was poised to revolutionize the market for mechanical ventilators (for instance, by successfully bringing its Aura ventilator to market).

The New York Times article claimed that Newport’s ventilators would be sold (at least to the US government) for $3,000 — a substantial discount from the reportedly then-going rate of $10,000. If selling ventilators at this price seemed credible at the time, then Covidien — as well as Newport’s shareholders — knew that Newport was about to achieve tremendous cost savings, enabling it to offer ventilators not only to the the US government, but to purchasers around the world, at an irresistibly attractive — and profitable — price.

Ventilators at the time typically went for about $10,000 each, and getting the price down to $3,000 would be tough. But Newport’s executives bet they would be able to make up for any losses by selling the ventilators around the world.

“It would be very prestigious to be recognized as a supplier to the federal government,” said Richard Crawford, who was Newport’s head of research and development at the time. “We thought the international market would be strong, and there is where Newport would have a good profit on the product.”

If achievable, Newport thus stood to earn a substantial share of the profits in a multi-billion dollar industry.

Of course, it is necessary to apply a probability to these numbers: Newport’s ventilator was not yet on the market, and had not yet received FDA approval. Nevertheless, if the Times’ numbers seemed credible at the time, then Covidien would surely have had to offer significantly more than $108 million in order to induce Newport’s shareholders to part with their shares.

Given the low valuation, however, as well as the fact that Newport produced other ventilators — and continues to do so to this day, there is no escaping the fact that everyone involved seemed to view Newport’s Aura ventilator as nothing more than a moonshot with, at best, a low likelihood of success.

Curically, this same reasoning explains why it shouldn’t surprise anyone that the project was ultimately discontinued; recourse to a “killer acquisition” theory is hardly necessary.

3. Lessons from Covidien’s ventilator product decisions

The killer acquisition claims are further weakened by at least four other important pieces of information:

- Covidien initially continued to develop Newport’s Aura ventilator, and continued to develop and sell Newport’s other ventilators.

- There was little overlap between Covidien and Newport’s ventilators — or, at the very least, they were highly differentiated

- Covidien appears to have discontinued production of its own portable ventilator in 2014

- The Newport purchase was part of a billion dollar series of acquisitions seemingly aimed at expanding Covidien’s in-hospital (i.e., not-portable) device portfolio

Covidien continued to develop and sell Newport’s ventilators

For a start, while the Aura line was indeed discontinued by Covidien, the timeline is important. The acquisition of Newport by Covidien was announced in March 2012, approved by the FTC in April of the same year, and the deal was closed on May 1, 2012.

However, as the FDA’s 510(k) database makes clear, Newport submitted documents for FDA clearance of the Aura ventilator months after its acquisition by Covidien (June 29, 2012, to be precise). And the Aura received FDA 510(k) clearance on November 9, 2012 — many months after the merger.

It would have made little sense for Covidien to invest significant sums in order to obtain FDA clearance for a project that it planned to discontinue (the FDA routinely requires parties to actively cooperate with it, even after 510(k) applications are submitted).

Moreover, if Covidien really did plan to discreetly kill off the Aura ventilator, bungling the FDA clearance procedure would have been the perfect cover under which to do so. Yet that is not what it did.

Covidien continued to develop and sell Newport’s other ventilators

Second, and just as importantly, Covidien (and subsequently Medtronic) continued to sell Newport’s other ventilators. The Newport e360 and HT70 are still sold today. Covidien also continued to improve these products: it appears to have introduced an improved version of the Newport HT70 Plus ventilator in 2013.

If eliminating its competitor’s superior ventilators was the only goal of the merger, then why didn’t Covidien also eliminate these two products from its lineup, rather than continue to improve and sell them?

At least part of the answer, as will be seen below, is that there was almost no overlap between Covidien and Newport’s product lines.

There was little overlap between Covidien’s and Newport’s ventilators

Third — and perhaps the biggest flaw in the killer acquisition story — is that there appears to have been very little overlap between Covidien and Newport’s ventilators.

This decreases the likelihood that the merger was a killer acquisition. When two products are highly differentiated (or not substitutes at all), sales of the first are less likely to cannibalize sales of the other. As Florian Ederer and his co-authors put it:

Importantly, without any product market overlap, the acquirer never has a strictly positive incentive to acquire the entrepreneur, neither to “Acquire to Kill” nor to “Acquire to Continue.” This is because without overlap, acquiring the project does not give the acquirer any gains resulting from reduced competition, and the two bargaining entities have exactly the same value for the project.

A quick search of the FDA’s 510(k) database reveals that Covidien has three approved lines of ventilators: the Puritan Bennett 980, 840, and 540 (apparently essentially the same as the PB560, the plans to which Medtronic recently made freely available in order to facilitate production during the current crisis). The same database shows that these ventilators differ markedly from Newport’s ventilators (particularly the Aura).

In particular, Covidien manufactured primarily traditional, invasive ICU ventilators (except for the PB540, which is potentially a substitute for the Newport HT70), while Newport made much-more-portable ventilators, suitable for home use (notably the Aura, HT50 and HT70 lines).

Under normal circumstances, critical care and portable ventilators are not substitutes. As the WHO website explains, portable ventilators are:

[D]esigned to provide support to patients who do not require complex critical care ventilators.

A quick glance at Medtronic’s website neatly illustrates the stark differences between these two types of devices:

This is not to say that these devices do not have similar functionalities, or that they cannot become substitutes in the midst of a coronavirus pandemic. However, in normal times (as was the case when Covidien acquired Newport), hospitals likely did not view these devices as substitutes.

The conclusion that Covidien and Newport’s ventilator were not substitutes finds further support in documents and statements released at the time of the merger. For instance, Covidien’s CEO explained that:

This acquisition is consistent with Covidien’s strategy to expand into adjacencies and invest in product categories where it can develop a global competitive advantage.

And that:

Newport’s products and technology complement our current portfolio of respiratory solutions and will broaden our ventilation platform for patients around the world, particularly in emerging markets.

In short, the fact that almost all of Covidien and Newport’s products were not substitutes further undermines the killer acquisition story. It also tends to vindicate the FTC’s decision to rapidly terminate its investigation of the merger.

Covidien appears to have discontinued production of its own portable ventilator in 2014

Perhaps most tellingly: It appears that Covidien discontinued production of its own competing, portable ventilator, the Puritan Bennett 560, in 2014.

The product is reported on the company’s 2011, 2012 and 2013 annual reports:

Airway and Ventilation Products — airway, ventilator, breathing systems and inhalation therapy products. Key products include: the Puritan Bennett™ 840 line of ventilators; the Puritan Bennett™ 520 and 560 portable ventilator….

(The PB540 was launched in 2009; the updated PB560 in 2010. The PB520 was the EU version of the device, launched in 2011).

But in 2014, the PB560 was no longer listed among the company’s ventilator products:

Airway & Ventilation, which primarily includes sales of airway, ventilator and inhalation therapy products and breathing systems.

Key airway & ventilation products include: the Puritan Bennett™ 840 and 980 ventilators, the Newport™ e360 and HT70 ventilators….

Nor — despite its March 31 and April 1 “open sourcing” of the specifications and software necessary to enable others to produce the PB560 — did Medtronic appear to have restarted production, and the company did not mention the device in its March 18 press release announcing its own, stepped-up ventilator production plans.

Surely if Covidien had intended to capture the portable ventilator market by killing off its competition it would have continued to actually sell its own, competing device. The fact that the only portable ventilators produced by Covidien by 2014 were those it acquired in the Newport deal strongly suggests that its objective in that deal was the acquisition and deployment of Newport’s viable and profitable technologies — not the abandonment of them. This, in turn, suggests that the Aura was not a viable and profitable technology.

(Admittedly we are unable to determine conclusively that either Covidien or Medtronic stopped producing the PB520/540/560 series of ventilators. But our research seems to indicate strongly that this is indeed the case).

Putting the Newport deal in context

Finally, although not dispositive, it seems important to put the Newport purchase into context. In the same year as it purchased Newport, Covidien paid more than a billion dollars to acquire five other companies, as well — all of them primarily producing in-hospital medical devices.

That 2012 spending spree came on the heels of a series of previous medical device company acquisitions, apparently totally some four billion dollars. Although not exclusively so, the acquisitions undertaken by Covidien seem to have been primarily targeted at operating room and in-hospital monitoring and treatment — making the putative focus on cornering the portable (home and emergency) ventilator market an extremely unlikely one.

By the time Covidien was purchased by Medtronic the deal easily cleared antitrust review because of the lack of overlap between the company’s products, with Covidien’s focusing predominantly on in-hospital, “diagnostic, surgical, and critical care” and Medtronic’s on post-acute care.

Newport misjudged the costs associated with its Aura project; Covidien was left to pick up the pieces

So why was the Aura ventilator discontinued?

Although it is almost impossible to know what motivated Covidien’s executives, the Aura ventilator project clearly suffered from many problems.

The Aura project was intended to meet the requirements of the US government’s BARDA program (under the auspices of the U.S. Department of Health and Human Services’ Biomedical Advanced Research and Development Authority). In short, the program sought to create a stockpile of next generation ventilators for emergency situations — including, notably, pandemics. The ventilator would thus have to be designed for events where

mass casualties may be expected, and when shortages of experienced health care providers with respiratory support training, and shortages of ventilators and accessory components may be expected.

The Aura ventilator would thus sit somewhere between Newport’s two other ventilators: the e360 which could be used in pediatric care (for newborns smaller than 5kg) but was not intended for home care use (or the extreme scenarios envisioned by the US government); and the more portable HT70 which could be used in home care environments, but not for newborns.

Unfortunately, the Aura failed to achieve this goal. The FDA’s 510(k) clearance decision clearly states that the Aura was not intended for newborns:

The AURA family of ventilators is applicable for infant, pediatric and adult patients greater than or equal to 5 kg (11 lbs.).

A press release issued by Medtronic confirms that

the company was unable to secure FDA approval for use in neonatal populations — a contract requirement.

And the US Government RFP confirms that this was indeed an important requirement:

The device must be able to provide the same standard of performance as current FDA pre-market cleared portable ventilators and shall have the following additional characteristics or features:

• Flexibility to accommodate a wide patient population range from neonate to adult.

Newport also seems to have been unable to deliver the ventilator at the low price it had initially forecasted — a common problem for small companies and/or companies that undertake large R&D programs. It also struggled to complete the project within the agreed-upon deadlines. As the Medtronic press release explains:

Covidien learned that Newport’s work on the ventilator design for the Government had significant gaps between what it had promised the Government and what it could deliver — both in terms of being able to achieve the cost of production specified in the contract and product features and performance. Covidien management questioned whether Newport’s ability to complete the project as agreed to in the contract was realistic.

As Jason Crawford, an engineer and tech industry commentator, put it:

Projects fail all the time. “Supplier risk” should be a standard checkbox on anyone’s contingency planning efforts. This is even more so when you deliberately push the price down to 30% of the market rate. Newport did not even necessarily expect to be profitable on the contract.

The above is mostly Covidien’s “side” of the story, of course. But other pieces of evidence lend some credibility to these claims:

- Newport agreed to deliver its Aura ventilator at a per unit cost of less than $3000. But, even today, this seems extremely ambitious. For instance, the WHO has estimated that portable ventilators cost between $3,300 and $13,500. If Newport could profitably sell the Aura at such a low price, then there was little reason to discontinue it (readers will recall the development of the ventilator was mostly complete when Covidien put a halt to the project).

- Covidien/Newport is not the only firm to have struggled to offer suitable ventilators at such a low price. Philips (which took Newport’s place after the government contract fell through) also failed to achieve this low price. Rather than the $2,000 price sought in the initial RFP, Philips ultimately agreed to produce the ventilators for $3,280. But it has not yet been able to produce a single ventilator under the government contract at that price.

- Covidien has repeatedly been forced to recall some of its other ventilators ( here, here and here) — including the Newport HT70. And rival manufacturers have also faced these types of issues (for example, here and here).

Accordingly, Covidien may well have preferred to cut its losses on the already problem-prone Aura project, before similar issues rendered it even more costly.

In short, while it is impossible to prove that these development issues caused Covidien to pull the plug on the Aura project, it is certainly plausible that they did. This further supports the hypothesis that Covidien’s acquisition of Newport was not a killer acquisition.

Ending the Aura project might have been an efficient outcome

As suggested above, moreover, it is entirely possible that Covidien was better able to realize the poor prospects of Newport’s Aura project and also better organized to enable it to make the requisite decision to abandon the project.

A small company like Newport faces greater difficulties abandoning entrepreneurial projects because doing so can impair a privately held firm’s ability to raise funds for subsequent projects.

Moreover, the relatively large share of revue and reputation that Newport — worth $103 million in 2012, versus Covidien’s $11.8 billion — would have realized from fulfilling a substantial US government project could well have induced it to overestimate the project’s viability and to undertake excessive risk in the (vain) hope of bringing the project to fruition.

While there is a tendency among antitrust scholars, enforcers, and practitioners to look for (and find…) antitrust-related rationales for mergers and other corporate conduct, it remains the case that most corporate control transactions (such as mergers) are driven by the acquiring firm’s expectation that it can manage more efficiently. As Henry G. Manne put it in his seminal article, Mergers and the Market for Corporate Control (1965):

Since, in a world of uncertainty, profitable transactions will be entered into more often by those whose information is relatively more reliable, it should not surprise us that mergers within the same industry have been a principal form of changing corporate control. Reliable information is often available to suppliers and customers as well. Thus many vertical mergers may be of the control takeover variety rather than of the “foreclosure of competitors” or scale-economies type.

Of course, the same information that renders an acquiring firm in the same line of business knowledgeable enough to operate a target more efficiently could also enable it to effect a “killer acquisition” strategy. But the important point is that a takeover by a firm with a competing product line, after which the purchased company’s product line is abandoned, is at least as consistent with a “market for corporate control” story as with a “killer acquisition” story.

Indeed, as Florian Ederer himself noted with respect to the Covidien/Newport merger,

“Killer acquisitions” can have a nefarious image, but killing off a rival’s product was probably not the main purpose of the transaction, Ederer said. He raised the possibility that Covidien decided to kill Newport’s innovation upon realising that the development of the devices would be expensive and unlikely to result in profits.

Concluding remarks

In conclusion, Covidien’s acquisition of Newport offers a cautionary tale about reckless journalism, “blackboard economics,” and government failure.

Reckless journalism because the New York Times clearly failed to do the appropriate due diligence for its story. Its journalists notably missed (or deliberately failed to mention) a number of critical pieces of information — such as the hugely important fact that most of Covidien’s and Newport’s products did not overlap, or the fact that there were numerous competitors in the highly competitive mechanical ventilator industry.

And yet, that did not stop the authors from publishing their extremely alarming story, effectively suggesting that a small medical device merger materially contributed to the loss of many American lives.

The story also falls prey to what Ronald Coase called “blackboard economics”:

What is studied is a system which lives in the minds of economists but not on earth.

Numerous commentators rushed to fit the story to their preconceived narratives, failing to undertake even a rudimentary examination of the underlying market conditions before they voiced their recriminations.

The only thing that Covidien and Newport’s merger ostensibly had in common with the killer acquisition theory was the fact that a large firm purchased a small rival, and that the one of the small firm’s products was discontinued. But this does not even begin to meet the stringent conditions that must be fulfilled for the theory to hold water. Unfortunately, critics appear to have completely ignored all contradicting evidence.

Finally, what the New York Times piece does offer is a chilling tale of government failure.

The inception of the US government’s BARDA program dates back to 2008 — twelve years before the COVID-19 pandemic hit the US.

The collapse of the Aura project is no excuse for the fact that, more than six years after the Newport contract fell through, the US government still has not obtained the necessary ventilators. Questions should also be raised about the government’s decision to effectively put all of its eggs in the same basket — twice. If anything, it is thus government failure that was the real culprit.

And yet the New York Times piece and the critics shouting “killer acquisition!” effectively give the US government’s abject failure here a free pass — all in the service of pursuing their preferred “killer story.”