This article is a part of the The Law, Economics, and Policy of the COVID-19 Pandemic symposium.

[TOTM: The following is part of a blog series by TOTM guests and authors on the law, economics, and policy of the ongoing COVID-19 pandemic. The entire series of posts is available here.

This post is authored by Eric Fruits, (Chief Economist, International Center for Law & Economics).]

The Wall Street Journal reports congressional leaders have agreed to impose limits on stock buybacks and dividend payments for companies receiving aid under the COVID-19 disaster relief package.

Rather than a flat-out ban, the draft legislation forbids any company taking federal emergency loans or loan guarantees from repurchasing its own stock or paying shareholder dividends. The ban lasts for the term of the loans, plus one year after the aid had ended.

In theory, under a strict set of conditions, there is no difference between dividends and buybacks. Both approaches distribute cash from the corporation to shareholders. In practice, there are big differences between dividends and share repurchases.

- Dividends are publicly visible actions and require authorization by the board of directors. Shareholders have expectations of regular, stable dividends. Buybacks generally lack such transparency. Firms have flexibility in choosing the timing and the amount of repurchases, subject to the details of their repurchase programs.

- Cash dividends have no effect on the number of shares outstanding. In contrast, share repurchases reduce the number of shares outstanding. By reducing the number of shares outstanding, buybacks increase earnings per share, all other things being equal.

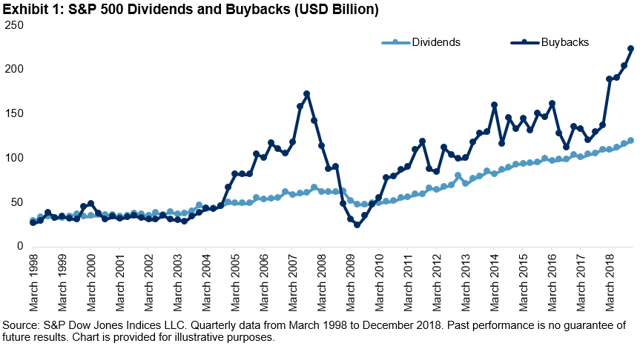

Over the past 15 years, buybacks have outpaced dividend payouts. The figure above, from Seeking Alpha, shows that while dividends have grown relatively smoothly over time, the aggregate value of buybacks are volatile and vary with the business cycle. In general, firms increase their repurchases relative to dividends when the economy booms and reduce them when the economy slows or shrinks.

This observation is consistent with a theory that buybacks are associated with periods of greater-than-expected financial performance. On the other hand, dividends are associated with expectations of long-term profitability. Dividends can decrease, but only when profits are expected to be “permanently” lower.

During the Great Recession, the figure above shows that dividends declined by about 10%, the amount of share repurchases plummeted by approximately 85%. The flexibility afforded by buybacks provided stability in dividends.

There is some logic to dividend and buyback limits imposed by the COVID-19 disaster relief package. If a firm has enough cash on hand to pay dividends or repurchase shares, then it doesn’t need cash assistance from the federal government. Similarly, if a firm is so desperate for cash that it needs a federal loan or loan guarantee, then it doesn’t have enough cash to provide a payout to shareholders. Surely managers understand this and sophisticated shareholders should too.

Because of this understanding, the dividend and buyback limits may be a non-binding constraint. It’s not a “good look” for a corporation to accept millions of dollars in federal aid, only to turn around and hand out those taxpayer dollars to the company’s shareholders. That’s a sure way to get an unflattering profile in the New York Times and an invitation to attend an uncomfortable hearing at the U.S. Capitol. Even if a distressed firm could repurchase its shares, it’s unlikely that it would.

The logic behind the plus-one-year ban on dividends and buybacks is less clear. The relief package is meant to get the U.S. economy back to normal as fast as possible. That means if a firm repays its financial assistance early, the company’s shareholders should be rewarded with a cash payout rather than waiting a year for some arbitrary clock to run out.

The ban on dividends and buybacks may lead to an unintended consequence of increased merger and acquisition activity. Vox reports an email to Goldman Sachs’ investment banking division says Goldman expects to see an increase in hostile takeovers and shareholder activism as the prices of public companies fall. Cash rich firms who are subject to the ban and cannot get that cash to their existing shareholders may be especially susceptible takeover targets.

Desperate times call for desperate measures and these are desperate times. Buyback backlash has been brewing for sometime and the COVID-19 relief package presents a perfect opportunity to ban buybacks. With the pressures businesses are under right now, it’s unlikely there’ll be many buybacks over the next few months. The concern should be over the unintended consequences facing firms once the economy recovers.